January isn’t usually a month where you see retail sales go through the roof, but these days investors are learning to expect the unexpected.

A 5.3% climb in retail sales last month blew analysts’ 1% average estimate out of the water and offered evidence that maybe the latest stimulus checks went quickly in and out of peoples’ hands to inject new life into the economy. Stock index futures didn’t react much to the news early Wednesday, but the 10-year Treasury yield—which posted a near one-year high yesterday above 1.3%—added to its gains.

Rising yields can be a sign of expectations for better economic growth, and some analysts expect double-digit earnings gains much of this year. Those gains, however, are going to get a tailwind from some pretty easy year-over-year comparisons thanks to last year’s pandemic-related earnings collapse.

Speaking of earnings, later today we have Tilray Inc TLRY, Hyatt Hotels Corporation H and Baidu Inc BIDU, among others. Then get ready for appearances tomorrow from Walmart Inc WMT and Marriott International Inc MAR. Obviously, WMT stands out in this bunch, and focus could be on how online sales are faring vs. in-store.

In its previous quarter, WMT’s online sales were ablaze, shooting 79% higher on a year-over year basis and accounting for a greater share of the retailer’s $134.7 billion in revenue. At the same time, in-store traffic saw some declines last year, and average tickets rose, suggesting consumers were shopping less often but stocking up when they did. One question going into tomorrow whether WMT will issue guidance this time out. It didn’t last time, but more reporting companies have been sharing outlooks throughout this earnings season.

Getting back to data, this morning’s other big number—the January Producer Price Index—offered a cautionary note. It rose 1.3%, way above analysts’ estimates for a 0.5% gain and above December’s 0.3% growth. This is just one data point, but it might trigger some fears of the economy possibly getting overheated.

Rally Fatigue?

When last week ended it felt like the market was having a little trouble sustaining the rally. That feeling spilled over into the new week on Tuesday. An early surge higher sputtered out despite renewed fundamental optimism. Today’s bullish retail sales news didn’t seem to get the engine chugging, either. All this might reinforce ideas that the major indices seem a bit fatigued.

Stocks like Tesla Inc TSLA and Apple Inc AAPL, which helped lead in January, have surrendered some gains and aren’t pulling the cart like they did. This could be one reason for the pause in the major indices, which often do best when “mega-caps” put on the after-burners. Another reason might be more investor money headed into bonds and alternative investments, attracted by climbing yields and fast price action there. Bitcoin recently clawed above $50,000 for the first time. Higher yields, in and of themselves, can threaten future earnings expectations by raising corporate borrowing costs, which often weighs on stocks.

MarketWatch reported Tuesday that it appears more investors are willing to take the risk of moving into longer-term corporate bonds despite the chance of rates going higher. There’s also a trend toward investment in higher-risk corporate bonds that pay more premium yields, although any investment here has to be carefully thought out because of the larger chance of default.

It’s been tough to be a stock market bear lately, to say the least. Whatever you may think of the market’s historic levels and valuations, many investors keep looking around and concluding that the risk-reward in the U.S. equity market may be the best game in town. That won’t necessarily always be the case, and rising yields and a volatility futures complex that’s in contango—with summer volatility expectations higher than current—are two possible warning signs.

“Perfect Storm” For Energy Sector

Tuesday saw Energy’s gains beat all other sectors thanks in part to frosty weather in Texas that shut refineries, knocked out power, and quickly ratcheted up the prices of crude and natural gas. To the surprise of few, companies that tend to do well when crude goes up—like Exxon Mobil Corporation XOM and ConocoPhillips COP—enjoyed nice boosts that spilled into pre-market trading today. Even before Texas went on ice, crude had been rolling up big gains since early November.

Some of the pre-storm crude gains might have reflected investor bets that a reopening economy and economic stimulus would raise demand for crude and other commodities like copper, which is also up huge over the last three months.

Financials also got a jumpstart on Tuesday, drawing energy from yield curve steepening (see chart below) that tends to help banks’ net margins. We’re still two months away from Q1 bank earnings, but don’t discount the chance that these rising yields—if they last—might start having a positive impact on bank earnings this quarter.

The dragging sector on Tuesday was Real Estate, which may be feeling the impact of rising bond yields. Those climbing yields could mean higher borrowing costs and a possible brake on the sizzling market for homes. The U.S. 10-year Treasury yield rose to 1.3% on Tuesday, the highest level in almost a year and about 80 basis points above last summer’s lows. More relevant to the housing market, the 30-year bond yield hit 2.08%. Stay tuned for January housing starts and building permits data tomorrow morning. Analysts expect relatively flat sequential growth.

In other data, but the Empire State Manufacturing Survey increased to 12.1 in February, from 3.5 in January and above the average Wall Street estimate. Fed minutes from the recent Federal Open Market Committee (FOMC) meeting are due later this afternoon.

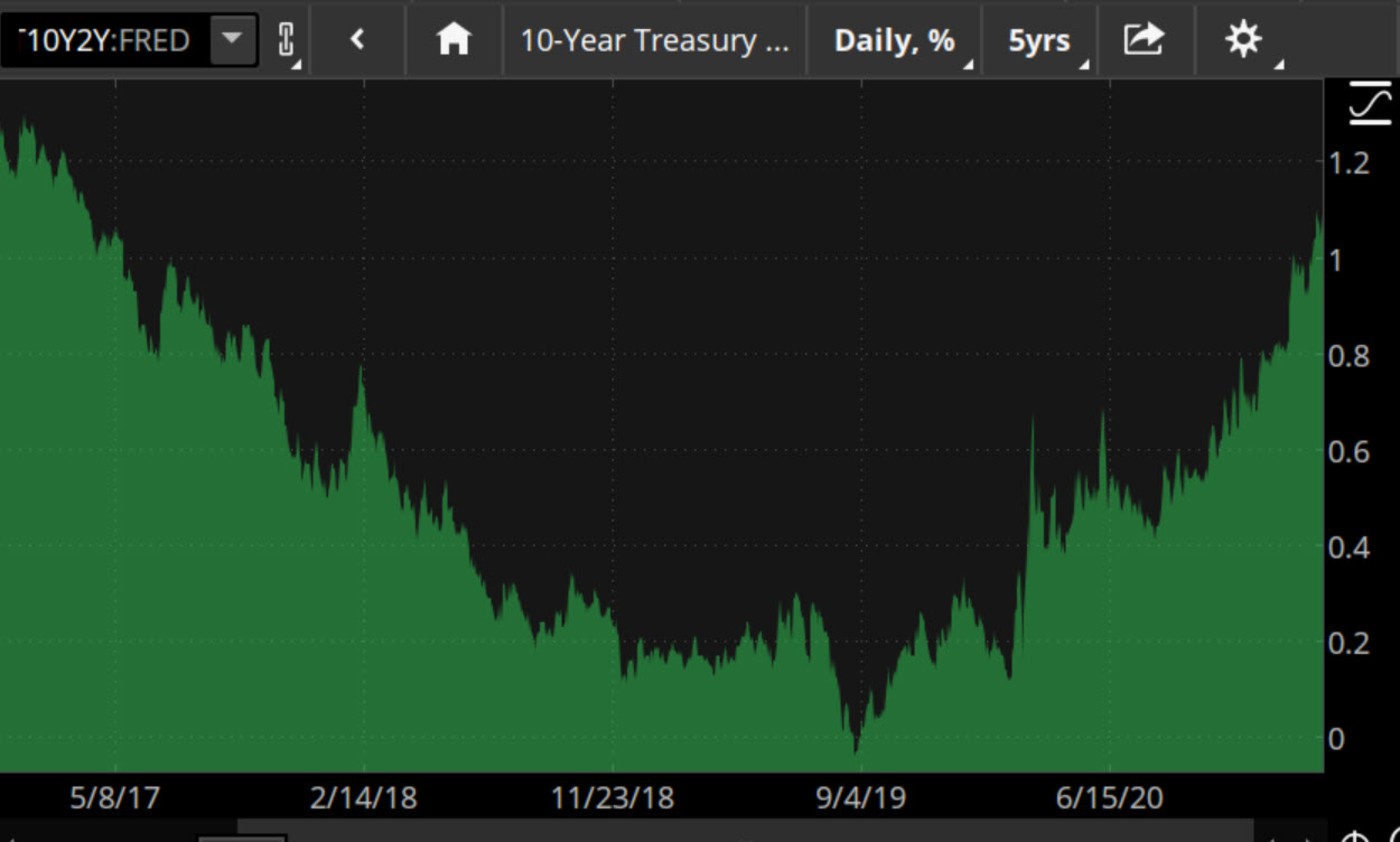

CHART OF THE DAY: PEAKS AND VALLEYS. The spread between 10-year and two-year Treasury yields (subtract the 2-year yield from the 10-year yield) has had its ups and downs over the last four years or so, to say the least. It’s now back at the highest level since mid-2017 as optimism grows about a reopening economy, pushing up longer-term yields. Data Source: Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

The Smell of Fear: If you’re actively trading the market, you probably already know how the Cboe Volatility Index (VIX) can be like a lighthouse spotlighting jagged rocks the market might be sailing toward even when the water seems calm. It happened again Tuesday, and if you had your eyes open in pre-market hours yesterday and noticed, you might want to give yourself a pat on the back. All the major stock indices indicated a higher open to start the shortened week, starting way back on Monday evening when futures trading began. At the same time, however, a red flashing light came from VIX, which was rapidly heading higher.

As we’ve noted here before, when stocks and VIX both climb at once, it often indicates that one or the other could soon change direction, and that’s what happened yesterday. After a higher open for stocks, VIX—which had fallen briefly below the historic average of 20 late last week—climbed above 22, and major indices briefly lost their footing and fell into negative territory. It was another “beware of the VIX” lesson to those who haven’t learned it yet. By the way, the VIX futures complex remains sharply in contango, with contracts for the summer trading up near 29. So that may be another thing to beware of even if you’re bullish overall. By the way, volatility edged a bit lower early Wednesday.

Is the Labor Market Too Hot, Too Cold or Just Right for More QE? You don’t even have to scour the news to hear conflicting opinions on the state of the market. Just power up your mobile device and plug into any financial news feed and you’ll hear more than a handful of “bad news bears” (or smart ones) claiming that the market may be a bit over its skis in terms of valuation. As an investor, of course this concerns you, as you have no idea whether these analysts are calling for a short-term correction or a longer-term plunge. But then, the devil is often in the details that you can’t easily see. Take Fed Chair Jerome Powell’s statement last Wednesday that the “real” unemployment rate isn’t 6.3% but “closer to 10%,” and that our economy is “still very far from a strong labor market whose benefits are broadly shared.”

It’s important to play connect-the-dots. An overheating economy is dangerous when labor markets are tight, because increases in the cost of living may demand higher wages which in turn feeds back to consumers (most of whom work) causing them to demand higher wages to keep up with inflation. But in an environment with a little more slack in the labor market—in other words, a pool of unemployed “reserves” to hire—the economy might be able to withstand a little more heating-up.

FOMO Extends Reign: You can talk about possible dark clouds like higher yields and rising volatility hanging over the stock market, or get into a knot about events like last month’s short-covering surge. However, every time major indices move lower, they seem to find quick buying interest as many investors continue to join the FOMO (Fear of Missing Out) crowd. If the S&P 500 Index (SPX) starts to stumble, places to look for support might be near the 20-day moving average of 3850, and below that at the 50-day MA of 3775.

The SPX and all the other major indices remain far, far above their 200-day moving averages. Typically, the 200-day is seen as a major level to watch, but those MAs have been left in the dust by the mighty surge that began in early November. The old saying is “Don’t fight the Fed,” and that might apply to this rally. To coin a more up-to-date phrase, maybe it’s “Don’t fight the stimulus” or, “It’s the vaccine, stupid!”

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by rupixen.com on Unsplash

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.