The Past Week, In A Nutshell

What Happened: Last week ended negative alongside mixed messaging on stimulus.

Remember This: “Markets have come a long way since the March lows, but we believe there may be more room for stocks to run,” said Jeff Buchbinder, Equity Strategist for LPL Financial.

“Given the impressive economic recovery to date and improving underlying technical and fundamental conditions, we think small cap stocks in particular may have attractive growth potential. Despite election and COVID-19-related risks, we see further gains ahead.”

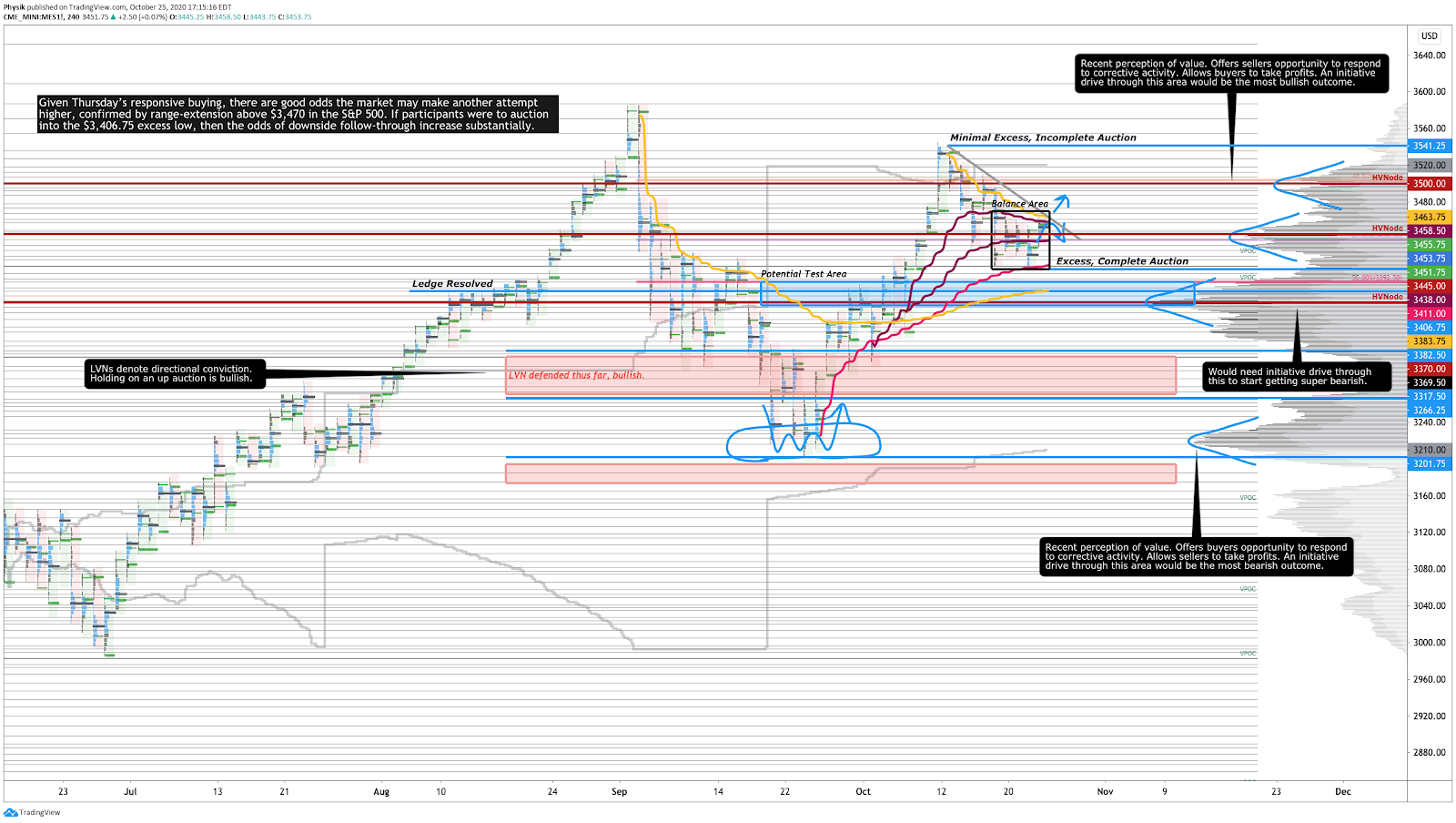

Pictured: Profile chart of the Micro E-mini S&P 500 Futures

Technical

Broad-market equity indices ended the week lower with the S&P 500 retracing nearly 40% of the rally that began after the September sell-off.

During Last Week’s Action: Alongside waning fiscal stimulus hopes, U.S. index products failed to show continued confidence to explore higher.

Instead, as the week progressed, House Speaker Nancy Pelosi walked back her deadline for a fiscal stimulus deal. After an initial drop on Monday, equity indices remained range-bound until Thursday’s session saw responsive buyers establish an excess low at the conjunction of multiple visual references. The buying continued into Friday’s close, at the high-end of the weekly range.

Overall, the market’s failure to range-extend, in either direction, is a sign of minimal conviction. Currently, the market is in the thick of an earnings season, elections are nearing, and stimulus talks are off-and-on. Given that the week ended in balance, a clear change in perception will be followed by a successful range extension in either direction. Adding, given Thursday’s responsive buying, there are good odds the market may make another attempt higher, confirmed by follow-through above $3,470 in the S&P 500. If participants were to auction into the $3,406.75 excess low, then the odds of further downside increase substantially.

Fundamental

In its global weekly commentary, BlackRock Inc BLK suggested the most recent resurgence of COVID-19 is not a replay of the spring.

"We believe daily new infections are likely a fraction of the peaks then, and rising case counts are having a diminishing negative impact on mobility. The economic restart has been quicker than expected, but the part that remains will be hardest. We do not expect a similarly large hit to economic activity as seen in the spring.”

Adding, however, the report noted the economy is facing challenges as the pace of growth begins to slow. Risks to the near-term recovery include fading fiscal stimulus, a prolonged or worsened pandemic, geopolitical tensions, and election complications.

Key Events

- Monday: Chicago Fed National Activity Index, New Home Sales.

- Tuesday: Durable Good Orders, House Price Index, CB Consumer Confidence.

- Wednesday: MBA Mortgage Applications, Goods Trade Balance, EIA Cushing Crude Oil Stocks Change, EIA Distillate Stocks Change.

- Thursday: GDP Growth Rate, Jobless Claims, Core PCE Prices QoQ, GDP Price Index, Pending Home Sales, PCE Prices QoQ.

- Friday: Core PCE Price Index YoY, PCE Price Index YoY, Core PCE Price Index MoM, PCE Price Index MoM, Personal Income MoM, Personal Spending MoM, Michigan Consumer Sentiment Final, Michigan Inflation Expectations Final.

Recent News

- House Speaker Nancy Pelosi on Sunday said the latest plan for aid is under review.

- U.K.’s NHS is preparing to introduce a coronavirus vaccine soon after Christmas.

- Commercial real estate, specifically office and lodging, faces the greatest uncertainty.

- The economy recovering slowly through October, but some sectors are still struggling.

- Policy drive toward the transformation of health insurance poses risk to profitability.

- General Motors Co GM investing $2 billion to build EVs in Tennessee.

- Intel Corporation’s INTC sale of memory business a credit positive.

- Alphabet Inc GOOGL breakup may be needed to end antitrust violations.

- China’s recovery lifted industrial commodities as its economy improved materially.

- Lockheed Martin LMT raised its full-year outlook after a third-quarter beat.

- American Express Co AXP issued a dismal outlook on travel, entertainment.

- Unacceptably high unemployment, low rates of resource utilization to rein in yields.

- Union Pacific Corp UNP reported a bigger-than-expected drop in profit.

- American Airlines AAL, Southwest Airlines LUV call for aid.

- Tesla Inc TSLA released “Full Self Driving” software upgrade to drivers.

- AstraZeneca AZN, Johnson & Johnson JNJ resuming trials.

- How blank-check acquirers could reshape emerging companies’ roles in markets.

- Fintech startups broke apart financial services and now the sector is rebundling.

- Texas Instruments Inc’s TXN revenue outperforms, outlook improves.

- China banking law changes will improve bank capital and formalize bank resolution.

- Business activity rose to a 20-month high as pace of new growth and orders eased.

- Courts rule against Uber Technologies UBER, Lyft Inc LYFT.

- Canada’s annual inflation rate rose in September, as retailer sales growth softened.

- FDA has approved Gilead Sciences Inc GILD antiviral drug remdesivir.

- Central bank digital currencies would compound current digital disruption for banks.

- The 2020 election could permanently change the way the United States does voting.

- Pandemic, remote work causes migration to small towns near public lands, resorts.

- Almost 60% of mutual fund assets will be ESG by 2025, according to a PwC forecast.

- Google Inc’s GOOGL dominance is reflected in search startup funding.

- President Vladimir Putin saw no need for global oil producers to change supply.

- More companies are offering earnings guidance, signaling adaptation to uncertainty.

- The third quarter could be the ‘biggest quarter of growth’ in United States history.

- Verizon Communications Inc VZ beat estimates for its third-quarter profit.

- Purdue Pharma LP agreed to plead guilty to criminal charges over prescription opioid.

- European Union to cut Canada, Georgia and Tunisia from “white list” travel countries.

Key Metrics

- Sentiment: 35.7% Bullish, 31.2% Neutral, 33.0% Bearish as of 10/21/2020.

- Gamma Exposure: (Trending Lower) 2,051,710,147 as of 10/23/2020.

- Dark Pool Index: (Trending Neutral) 40.9% as of 10/23/2020.

Cover Photo by Element5 Digital from Pexels.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.