The Federal Reserve this afternoon gave the market what it expected by standing pat on interest rates. That left investors and traders to delve into the language of the central bank’s accompanying press release and comments from Chairman Jerome Powell.

In its unanimous decision to leave its key policy rate unchanged, the Fed didn’t change too much in its statement accompanying the announcement. It did however downgrade its assessment of household spending, saying it has been rising at a “moderate” pace, compared with a “strong” pace the last time around. And central bankers said their current monetary policy is appropriate to support sustained economic expansion, a strong labor market, and inflation “returning to” its 2% objective.

Small Language Tweaks

The Fed decided to change that last bit from “near” to make it clear that it isn’t comfortable with inflation running persistently below that objective and to underscore that 2% isn’t a ceiling, Powell said during the press conference following the decision. And although the household spending wording was tweaked, Powell said the fundamentals supporting it remain solid.

Even though the Fed’s preferred inflation gauge, core personal consumption expenditure (PCE) prices, has been stubbornly below the 2% target, the economy seems to have been seeing positive impacts from three interest rate cuts last year, especially in the housing market and jobs market.

Powell did say during the press conference that there are “uncertainties” about the outlook, including from the coronavirus outbreak. It seems likely that the Fed won’t start factoring in the potential economic damage from the outbreak until companies start commenting on it in depth. Although some companies have mentioned it this earnings season, it’s been too early for us to get a really good feel for how it could affect corporate results in the future.

What Might Be Next?

Prior to the announcement, the futures market had built in about an 85% chance of the central bank standing pat on the Fed funds rate. Futures didn’t show any chance of a rate cut, but did indicate a small chance for a 25-basis point rise. It’s hard to see where that was coming from with the coronavirus and sluggish economic growth.

Looking further into the year, odds of any kind of Fed rate action seem to be retreating. It’s an election year, which could be one reason many analysts and investors expect the Fed to sit back. While election year rate moves aren’t unheard of, they’re a bit more rare because the Fed doesn’t want to give the impression of favoring one side or the other. It also cut rates three times in the second half of 2019, so some analysts argue the Fed wants to wait and see how that works through the system before doing anything else.

One key thing to consider if you’re trying to read the Fed’s intentions comes Friday morning when investors get a look at December PCE prices. (See more below.)

Repo Redux

Another question heading into the meeting today was around the Fed’s balance sheet. The Fed has been intervening since last fall through repurchase agreements, or “repos”, and that program was initially set to run through Feb. 13, but at the meeting the Fed said it intends to continue operations “through April,” and to continue buying Treasury bills “through the second quarter of 2020.”

The Fed’s interventions might have helped set off the stock buying spree seen since October, and many went into the meeting expecting to hear more about the future of the Fed’s repo facility. In the press conference, Powell said the Fed plans to move toward an “equilibrium level” for operations, but didn’t say with certainty what that level might be, as they’re still monitoring the rate market.

While it’s definitely possible that some of the rally since October reflects this Fed buying, there’s a lot of other fundamental news the market was reacting to, including the phase one trade agreement and hopes for better earnings as 2020 moves along. The Fed’s pledge to keep rates low also helped. There’s usually no one reason why the market moves, and trying to pinpoint specific ones is probably a losing game.

Watching Yields

The Fed is probably closely tracking yields, too. The premium of the 10-year Treasury yield to the two-year yield has fallen pretty sharply so far this year after going inverted for a while back in mid-2019. There’s a lot of debate around the possible impact of a flat or inverted curve (one where longer-term rates are even with or below shorter-term rates). Some economists see that as a recession indicator, but it’s unclear if cause and effect are really there. The gap seems to be stabilizing at around 18 basis points, with 10-year yields at around 1.62% earlier today. That’s down from recent peaks of near 1.95%, but the coronavirus is an extra weight that might be lifted if progress is made against the illness.

With interest rates still negative in Europe and Japan, the Fed found itself swimming upstream when it tried to tighten here in 2017 and 2018. Even with three cuts since July, U.S. rates are still considerably higher than rates among other developed nations, so that tends to bring foreign buyers here for yield. The resulting demand for bonds helps push U.S. yields lower.

The Fed put up a good fight but then appeared to lay down the sword. A nearly 20% drop in the S&P 500 (SPX) in Q4 2018 shows what the markets thought of the Fed’s hawkish policy back then, and the roaring rally since October shows how investors tend to react to lower rates, Fed stimulus, and the promise of continued dovish policy.

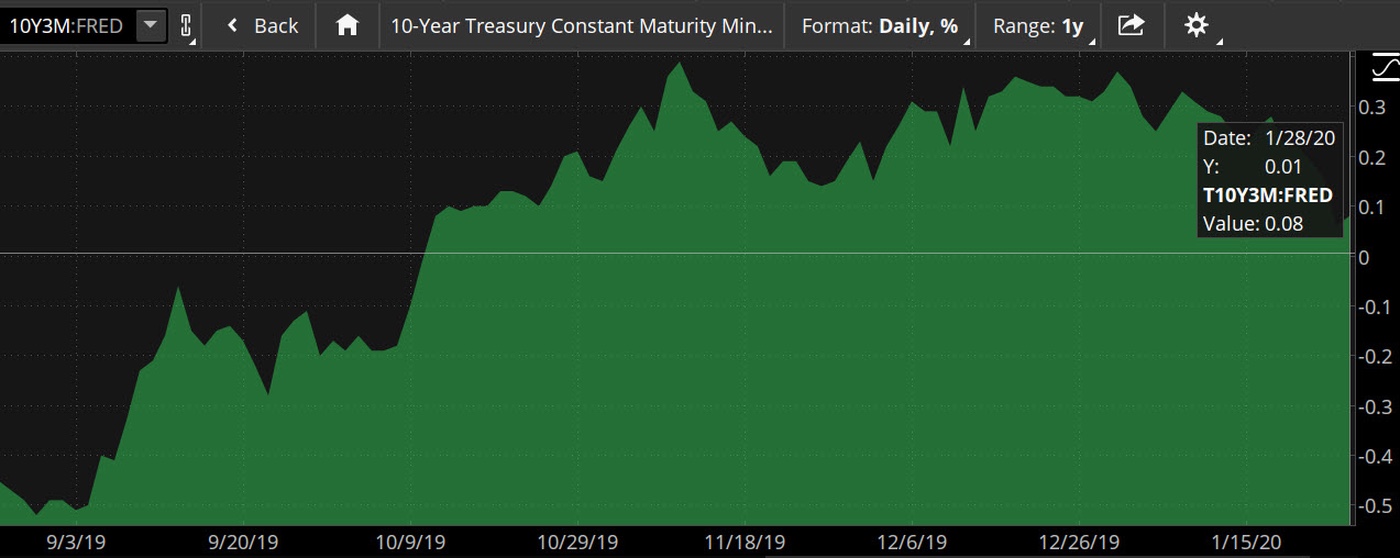

CHART OF THE AFTERNOON: INVERSION DIVERSION. Much ink has been spilled in the financial press over the past year regarding yield curve inversions and whether they portend recessions. One thing is clear: financial institutions, especially those which rely heavily on net interest margin, can feel the pressure. The yield spread between 3-month and 10-year Treasuries spent a chunk of last year in the negative, but a string of interest rate cuts by the Fed pushed the 3mo/10yr spread back to the plus side, by about 40 basis points at one point. Over the past month, however, investors seeking safety in the 10-yr, while the Fed has been seen as on hold from further rate cuts, have helped cause the 3-mo/10-yr to begin flirting with the zero line again. And it briefly inverted earlier this week amid coronavirus worries. Data source: Federal Reserve’s FRED database. Chart source: The thinkorswim® platform from TD Ameritrade. FRED® is a registered trademark of the Federal Reserve Bank of St. Louis. The Federal Reserve Bank of St. Louis does not sponsor or endorse and is not affiliated with TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

PCE On Tap: If you’ve been following the Fed a while, you’ve probably heard that they keep a close eye on personal consumption expenditure data (PCE) as an inflation meter. Also, you might know that it’s been lagging for a long time and through November stayed below the Fed’s 2% inflation target. Analysts expect the Friday PCE data to show 0.2% price growth in December, even with November’s read. Core PCE, which strips out more volatile elements like food and energy, also is seen up 0.2%, Briefing.com said. That would be up from 0.1% in November.

Price Check on Aisle Fed: While the Fed and investors await PCE prices on Friday, a question is why this number has been stuck in place. As of November, PCE prices had risen just 1.5% year-over-year, and core prices had risen 1.6% from a year earlier. It could be interesting to see Friday if the numbers have moved closer to 2%. Still, it would probably take a bunch of months of growth of more than 2% before the Fed started to really worry about inflation.

In the past, Fed officials have said they could see letting inflation run a little above 2% for a while as they try to fulfill their role of supporting maximum employment. Raising rates too soon in response to inflation might cut off the kind of jobs growth that’s kept unemployment at 50-year lows for months.

Inflation and Wages: One thing Powell has said about the employment situation is that he likes how job and wage growth have started to filter through to some of the more disadvantaged people in the country. Though year-over-year wage growth was only decent at 2.9% last month, the gains are still near recent one-decade highs and were 3% or better for a year-and-a-half heading into December. One thing the Fed might want to get answers to is why, with unemployment at just 3.5%, wage growth hasn’t been even stronger.

While it’s nice to see inflation in check if you’re a consumer, it also suggests that paychecks are somehow being held down by some force or other, and it would be good to see people have more in their wallets.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy.

Image by NikolayFrolochkin from Pixabay

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.