The last quarter was a rough arena in some ways for semiconductors as US-China trade tensions, recession fears, and mixed interest rate expectations covered the field with a thick fog of market noise, volatility, and plenty of headline risk.

Amid this backdrop, two of the chip industry’s biggest players—Intel Corporation INTC and Advanced Micro Devices, Inc. AMD—slogged it out with new products aimed at either capturing or defending market share in the central processing unit (CPU) space.

Semis Up in Market, But Earnings Under Pressure

In the runup to this earnings cycle, a record number of Tech sector firms issued negative earnings guidance, according to FactSet. Analysts expect a year-over-year earnings decline of 10.2% for the sector as a whole. And among the sub-industries in Technology, semiconductors are expected to deliver the largest drop—negative 30%, according to FactSet.

Against these expectations, however, the PHLX Semiconductor Index SOX appears to be charging ahead. Since July 1, the SOX had advanced around 5%, recently surpassing its three-month closing high of 1625 (though it’s since backed off from that level). By comparison, the S&P 500 index (SPX) rose 0.9% over the same period.

Since reporting Q2 earnings, AMD shares have risen around 2%, while INTC advanced 0.5%. Looking ahead, INTC is scheduled to report Q3 earnings results this Thursday, Oct. 24. AMD will be reporting next week on Oct. 29.

In terms of market performance, the two are seemingly neck-and-neck, with AMD holding a slight advantage. Both chipmakers are locked in an elbows-out battle over dominance across multiple CPU spaces covering desktop, gaming, mobile, and enterprise applications. And it appears that the jostling will continue to play out well into the next year, as competition between their latest and coming product releases gets underway.

Potential Headwinds for Semiconductors

In light of the conditions above—namely tariffs and other economic uncertainties—consider paying attention to corporate infrastructure spending and how that might affect demand for the products chip companies offer. When the future seems undefined, companies often won’t spend on infrastructure.

And once trade uncertainty is lifted, it’ll take time for any infrastructure plans to come to fruition. When companies can’t plan, businesses can get hurt. That said, chip companies have been left on the roadside for dead several times this year alone, yet they keep performing.

On the bright side, there’s a certain level of demand for CPUs that’s probably going to be there regardless of what’s happening with the economy. People rely on tech-driven gadgets, not just laptops and desktops but also phones and popular video games—all of those things are powered by chips. And if chipmakers are performing well in the market, as AMD and INTC appear to be, that often indicates investor confidence in the broader economy.

Overall, semiconductor stocks are near their highs, and one thing to keep in mind is that data centers make up a sizeable chunk of their market. The enterprise segment may be a critical component to the industry’s performance in the coming quarters, as corporate spending drives enterprise revenue.

When AMD last reported in July, it beat earnings and revenue expectations, yet revenue was down 13% from the same reporting period a year prior. That last piece of news might have helped cause shares to tumble 10% the following day. But the stock bounced back four sessions later after hitting a low of $27.65, as that month also saw the continued roll-out of AMD’s 7-nanometer (7nm) Ryzen 3000 desktop series processors (a fundamental factor that might have supported the stock’s performance).

If that sounds like a foreign language, a smaller nanometer count typically means more computing power packed into a much smaller space. AMD’s latest generation 7nm Ryzen processors may give the company a slight advantage, as its closest competitive product series, INTC’s 9th gen CPUs, currently offers a 14nm manufacturing process.

AMD’s nanometer advantage accelerated its capacity to swoop in and capture a sizable portion of market share across the desktop and gaming (graphics processing unit, or GPU) space. INTC’s small core supply shortage might have also contributed to AMD’s momentum.

Following up on its strong foray into the small core CPU space, AMD launched its EPYC “Rome” processor in early August aimed at the enterprise (server and data center) market, further advancing the company’s products into a field long dominated by INTC.

In addition to its technological advantages, AMD has also been attempting to outprice its rivals, with more core/thread power at a much lower price than many of its rivals. For instance, AMD’s 2990WX processor (for gaming devices) features 32 cores and 64 threads are priced at $1,699.00 as compared with INTC’s i9-9980XE processor with 18/36 cores/threads priced at $1,989.99. If you’re not familiar with cores and threads, think of it this way: having more cores in a processor is like having more workers in the workplace.

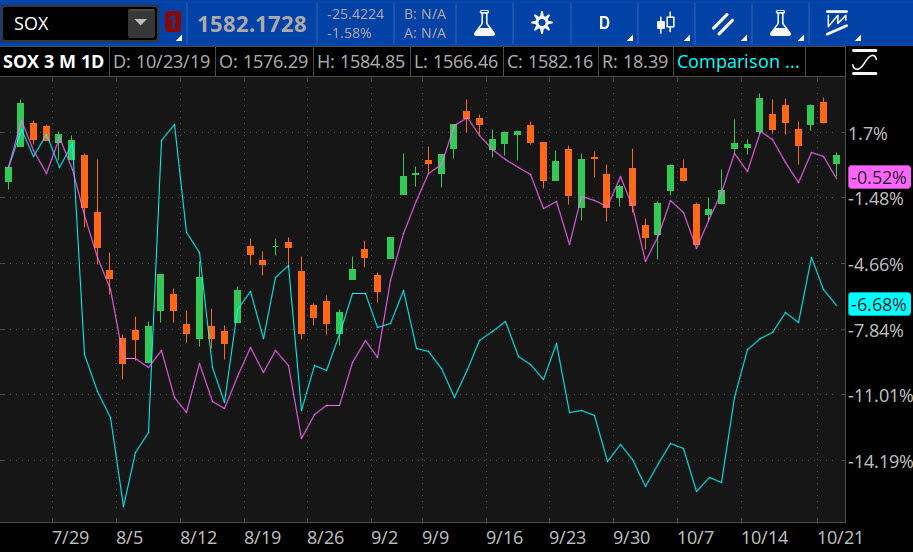

FIGURE 1: PLAYING CATCH-UP. After sagging in September, shares of Advanced Micro devices (AMD - blue line) have had a roaring start to October, while Intel shares (INTC - purple line) have been treading water the last couple of months following a summer surge. However, both names have lagged the Philadelphia Semiconductor Index (SOX - candlestick) over the last few months. Data Source: Nasdaq. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

AMD Earnings and Options Activity

Heading into Q3 earnings season, the company guided for revenue of approximately $1.8 billion That would be an increase of approximately 9% year-over-year and 18% sequentially.

When AMD releases results, it's expected to report adjusted EPS of $0.18, up from $0.13 in the prior-year quarter, on revenue of $1.81 billion, according to third-party consensus analyst estimates. That revenue would represent a 9.4% rise from a year ago.

The options market has priced in approximately a 7% stock price move in either direction around the upcoming earnings release. Implied volatility was at the 29th percentile as of Wednesday morning.

Looking at the Nov. 1 weekly option expiration, call options have been active at the 34, 34.5 and 35 strikes Put volume has been lighter overall, but activity has been highest at the 30 and 32 strikes.

Note: Call options represent the right, but not the obligation, to buy the underlying security at a predetermined price over a set period of time. Put options represent the right, but not the obligation to sell the underlying security at a predetermined price over a set period of time.

Intel’s Ambition on Display

Despite INTC’s 3% year-over-year revenue decline in Q2, the chipmaker beat revenue and earnings expectations. The company had a few rough spots, including a small core supply shortage and trade-related uncertainties, but overall, INTC’s Q3 outlook and guidance, according to financial research firm Refinitiv, were above expectations.

George Davis, INTC’s CFO, told analysts in a conference call that the company expects to generate $1.24 per share and a revenue of $18 billion in Q3 (in contrast to Refinitiv estimates of $1.16 per share and revenue of $17.72 billion). Despite Davis’ above-consensus guidance, note that his EPS figure represents a year-over-year decline of 11.4%, while revenue expectations represent a year-over-year slide of around 6%.

Yet aside from competitive pressure from AMD—namely INTC’s loss of market share and potential erosion of margin due to AMD’s competitive pricing and capacity to provide supply over INTC’s shortage—the chipmaker is in the midst of implementing an ambitious game plan aimed at maintaining its long-standing dominance in the market.

“We’re pursuing the largest opportunity in our company’s history, a nearly $300 billion TAM (total available market) comprised not just of CPUs for PCs and servers, but of XTUs and adjacent technologies for an incredibly wide range of workloads and devices,” INTC CEO Robert Swan said in a conference call. “XTU,” or “extreme tuning utility,” is an application that allows users to crank more power out of a platform.

The second part of INTC’s plan is aimed toward “accelerating the rate of innovation,” in its current product development. This last part actually speaks to what arguably is INTC’s unique competitive advantage in the CPU space—the company is well capitalized, and its revenues are 10 times those of its now fiercest competitor, AMD.

INTC’s first 10nm chips for mobile platforms, code-named Ice Lake, are expected to hit shelves during the holiday season. Its latest 10-nm system-on-chip designed for 5G base station, Snow Ridge, is in production and scheduled to launch early in 2020. With Snow Ridge, INTC aims to capture a 40% share of the 5G market segment by 2022, according to Swan.

But perhaps its most anticipated product series is the upcoming 7nm chips, which, according to Swan, is on track for launch in 2021. “Our 7-nanometer process...will be comparable to competitors’ 5-nanometer nodes,” Swan added.

Intel Earnings and Options Activity

When INTC releases results, it is expected to report adjusted EPS of $1.24, down from $1.40 in the prior-year quarter, on revenue of $18.05 billion, according to third-party consensus analyst estimates. That revenue would represent a 5.7% decline from a year ago.

Options traders have priced in approximately a 4.4% stock price move in either direction around the upcoming earnings release, according to the Market Maker Move indicator on the thinkorswim platform. Implied volatility was at the 48th percentile as of Wednesday morning.

Looking at the Oct. 25 weekly option expiration, call options have been most active at the 54 and 55 strikes. Put volume has been lighter overall, but most active at the 49.5 and 51 strikes.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

Image Sourced from Pixabay

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.