(Friday Market Open) A sentiment change is taking place on Wall Street as investors continue coming to grips with the negative economic data and lower Federal Reserve forecasts that rocked this week’s markets.

The market is generally shaking off optimistic expectations from some participants who’d thought that the economy could have a “soft landing” as the Fed eased up on tightening. That particular group of investors is likely getting an unwelcome reality check as stock futures continue this morning’s slide after yesterday’s sharp losses.

Things are likely to move lower in the near term as a downtrend remains in place after the S&P 500® index (SPX) bounced off the 4,100 level earlier this week. It could be interesting to see where a major support level might come into play. One such level was 3,900, but we’re already below that in futures trading this morning.

That said, a severe pullback seems unlikely, and after all the fireworks so far this week, we might have a slow Friday afternoon and a slow close as the holiday season looms. A lot of the action seems more or less played out.

There’s a bit of data coming soon after the market opens today. Investors get a look at preliminary December IHS Markit Manufacturing and Services Purchasing Manager’s Index (PMI). Both were in contraction territory last month.

Several Fed speakers are also scheduled today as the “quiet period” around this week’s Federal Open Market Committee (FOMC) meeting ends. It would be fairly surprising to hear any of them contradict the hawkish tone that came out of the FOMC gathering, but they’ll still be worth a listen.

Next week brings a heavy dose of housing data and an expected earnings report from Nike (NKE).

Morning Rush

- The 10-year Treasury yield (TNX) inched up 3 basis points to 3.48%.

- The U.S. Dollar Index ($DXY) stayed flat at 104.56.

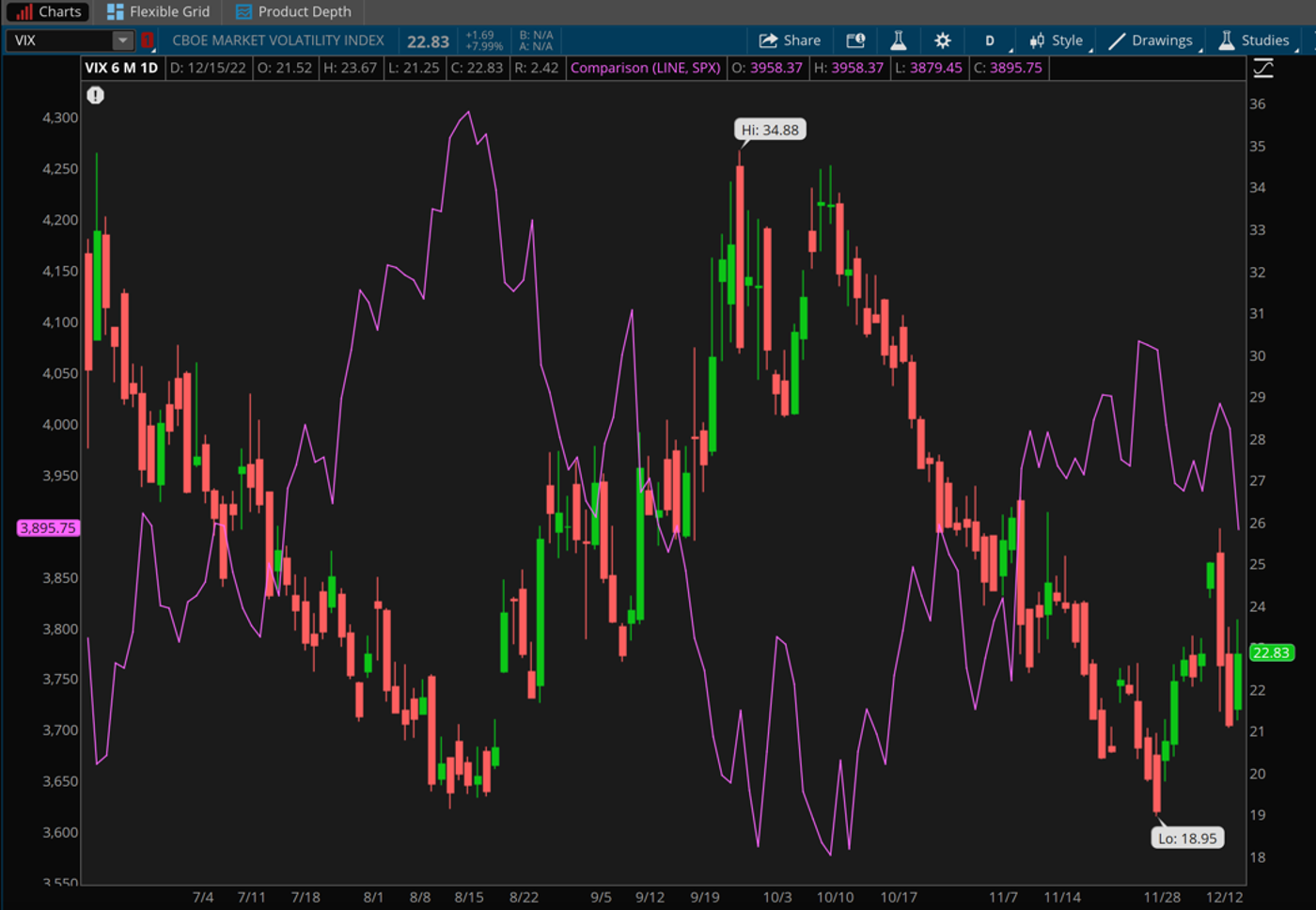

- Cboe Volatility Index® (VIX) futures are climbing, reaching 23.29.

- WTI Crude Oil (/CL) is giving up recent gains, down more than 2% at $74.41 per barrel.

You might’ve expected Treasury yields to get a lift thanks to the Fed’s hawkish tone on Wednesday. That wasn’t the case Thursday for the 10-year Treasury yield (TNX), which actually fell five basis points to 3.45%, near its recent lows. The 2-year Treasury yield, which is most sensitive to rate changes, however, barely budged Thursday.

The inverted yield curve got even more inverted Thursday and recently stood at 80 basis points for the 2/10. That’s near 2022 peak levels and may point toward growing market fears of recession. However, both the $DXY and /CL held up pretty well yesterday despite recession worries. Both would likely fall quite a bit from current levels if the economy really starts to crater.

Thursday’s losses in the stock market reflected investor worries that the Federal Reserve could tighten the economy into recession. Rate hikes in Europe by the Bank of England (BoE) and European Central Bank (ECB) just added to the gloominess on Wall Street. Worries about climbing COVID-19 cases as China re-opens could put a third candle on the cake.

Just In

Darden Restaurants (DRI) is one of the few bright spots this morning. Shares rose more than 1% in premarket trading after the company beat analysts’ estimates on both revenue and earnings per share (EPS) and raised its 2023 outlook. A 7.6% quarterly gain in same-store sales at Olive Garden was among the quarterly highlights. Apparently, people are still dining out despite inflation, but this one remains worth watching for trends on consumer spending.

Turning to geopolitics, there’s fresh news on the Ukraine front. Reports say Russia has launched a new barrage of missiles on many cities. Any escalation of the situation there could raise uneasiness around global markets.

Thinking Cap

If you’re one of many investors worried about a possible recession and its impact on your portfolio, there are some ways you can consider preparing.

- Investing strategies like dollar-cost averaging and diversifying can help you weather some of the storm, though there’s no foolproof way to avoid some damage.

- With the end of the year fast approaching, don’t forget to consider tax-loss harvesting, a process designed to take advantage of the IRS tax-loss harvesting rule that allows realized losses to offset the realized gains in your taxable portfolio. This process may potentially lower your tax liability—on the condition that all the trades are closed out in the same calendar year.

- In the meantime, defensive areas of the market might get more investor attention in coming weeks, including sectors like staples, utilities, and health care. None of these are recession-proof, but the old argument is that people still eat, turn on the heat in winter, and get sick even in hard times.

- A couple other sectors attracting some investor interest are energy and financials, neither of which typically comes to mind as recession-proof. Typically, growth and tech names take the worst blows in a full-on economic downturn.

- Many investors appear to be embracing longer-term fixed income, as we can see by the falling 10-year Treasury yield over the last month.

Reviewing the Market Minutes

“Risk-off” trading went into full swing Thursday, with growth sectors like information technology and communications services at the bottom of the sector performance scorecard. Financials also had a rough day, falling about 2%, and it’s often said you can’t have a rally without the banks.

It’s also hard to have a rally without stocks like Apple (AAPL). That particular behemoth was a big loser Thursday, falling nearly 5%. At its current price near $136 per share, AAPL isn’t far above its June low near $130, and it can often be a market barometer.

AAPL’s weakness, along with poor performances from fellow mega-caps like Microsoft (MSFT) and Alphabet (GOOGL), don’t tell a positive story for the overall market. The semiconductor subsector of info tech, which had been on a nice roll, sagged more than 4% on Thursday. This particular subsector is often seen as a global barometer of business demand.

Here’s how the major indexes performed Thursday, as every S&P sector declined:

- The Dow Jones Industrial Average® ($DJI) slide 764 points, or 2.25%, to 33,202.

- The Nasdaq® ($COMP) plunged 3.23% to 10,810.

- The Russell 2000® (RUT) dropped 2.25% to 1,774.

- The SPX fell 99 points, or 2.49%, to 3,895.

Talking Technicals: The SPX made a valiant late attempt Thursday to hold onto 3,900 but ultimately failed. A finish above that might’ve been viewed as technically positive, because it’s roughly the bottom of the recent range it’s traded in between 3,900 and 4,100. It’s also a psychological level, being a nice round number. The failure to close above 3,900 might lead to further technical selling today.

CHART OF THE DAY: SUPPORT CONVERGING. The 10-Year Treasury yield (TNX—candlesticks) now sits near a downtrend line on the chart (red line) and near its 100-day MA (blue line). We’ll see where it goes now that the FOMC has spoken. Data source: Cboe. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

The New Fed Conundrum? In early 2005, then-Fed Chairman Alan Greenspan used the word “conundrum” to describe his frustration as the 10-year Treasury yield (TNX) refused to rise despite a series of Fed rate hikes. Financial markets—and the overall economy—are arguably much more structurally sound now than back in 2005. But the Fed still has a conundrum as it tries to walk a tightrope between the two sides of its dual mandate—price stability and maximum employment. In Powell’s post-meeting press conference Wednesday, he made it clear that the Fed would like to temper some of the exuberance (another Greenspan term) that pushed asset prices to record levels in recent years without doing excess damage to the job market.

Today’s conundrum seems to be whether the Fed can time its policy adjustments to engineer a soft landing. Yesterday’s softer-than-expected retail sales number, combined with a steep fall in the U.S. savings rate (2.3%, the lowest level since 2005, according to Reuters), could indicate a pullback in consumer spending. We’ll keep an eye on the University of Michigan’s Consumer Sentiment Index December 23, and the Conference Board’s Consumer Confidence Survey December 27 for more insight into whether the Fed is close to sticking a “soft landing” or if the seatbelt sign will need to stay on through 2023.

Whither Earnings? Another conundrum, which won’t likely be answered until we get past the holidays, is how low the market needs to go to reflect possible softer earnings projections caused by this hawkish Fed. The combination of rising rates, higher inflation, and weaker economic growth the Fed forecast Wednesday doesn’t augur well for earnings in 2023. Even with Thursday’s sell-off, you could argue the market isn’t close to reflecting the downward earnings path.

We’ve talked about it here during each of the last few market rallies: Stocks remain at high valuations if you start to work an economic recession into your forecast. And whether there’s an actual recession, an “earnings recession” now seems quite likely, according to many analysts. For instance, in a note to investors after the Federal Open Market Committee (FOMC) meeting Wednesday, research firm CFRA said it now sees a “challenging first half” of 2023, with Q1 S&P earnings growth of just 0.5% followed by Q2 earnings falling 1.4%. Both of those are down from CFRA’s September 30 estimates. Further drops in earnings projections (you can fill in the possible numbers) might give today’s SPX forward price-earnings (P/E) ratio a valuation as high as 20 if earnings fall 5% to 10%, which isn’t uncommon in a recession. That theoretical scenario takes the P/E back to where it was very early this year, and we know what happened after that.

What’s VIX Saying? Surprisingly, volatility stayed in check early Thursday even as the stock market got knocked around and the SPX fell to one-month lows. The VIX did climb, but only to around 23 by midday, well below the 25 threshold that might signal trouble. VIX has generally been well behaved over the last month, though it did briefly leap above 25 earlier this week. One thing the VIX is possibly telling us is that today’s selling in stocks might be overdone. History tells us that a sell-off in stocks not accompanied by climbing volatility sometimes has a short shelf life. That said, the Fed’s economic projections and promise of more rate hikes likely raise the chance for “bouts of volatility” between now and the next Fed rate announcement on February 1, said Charles Schwab Chief Investment Strategist Liz Ann Sonders, in her commentary about Wednesday’s Fed meeting.

Notable Calendar Items

Dec. 19: No earnings or data of note

Dec. 20: November Housing Starts and Building Permits and expected earnings from General Mills (GIS) and Nike (NKE)

Dec. 21: November Existing Home Sales and expected earnings from Rite Aid (RAD) and Micron (MU)

Dec. 22: Government’s final Q3 GDP estimate and expected earnings from CarMax (KMX)

Dec. 23: November Durable Orders, November Personal Income and Spending, November PCE Prices, November New Home Sales, and Final December University of Michigan Consumer Sentiment

Dec. 26: Markets closed for official Christmas Day holiday. Enjoy if you celebrate!

Dec. 27: December Consumer Confidence

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.