An Economic World War III

President Biden deserves credit for having so far avoided World War III. He has resisted calls to impose a no-fly zone over Ukraine, which would lead to war with Russia, and he has clearly signaled he has no intention of fighting Russia.

But Biden has, in effect, helped launch an economic World War III, imposing unprecedented sanctions on a large and economically important country. Russia isn't an Iran or Libya. It's a continent-spanning country with a population of 145 million, and it is (or was) one of the world's top five exporters of oil, natural gas, nickel, wheat, coal, and other commodities. Let's breakdown why these sanctions are dangerous for us, and close with our investment approach to them.

What's The Endgame?

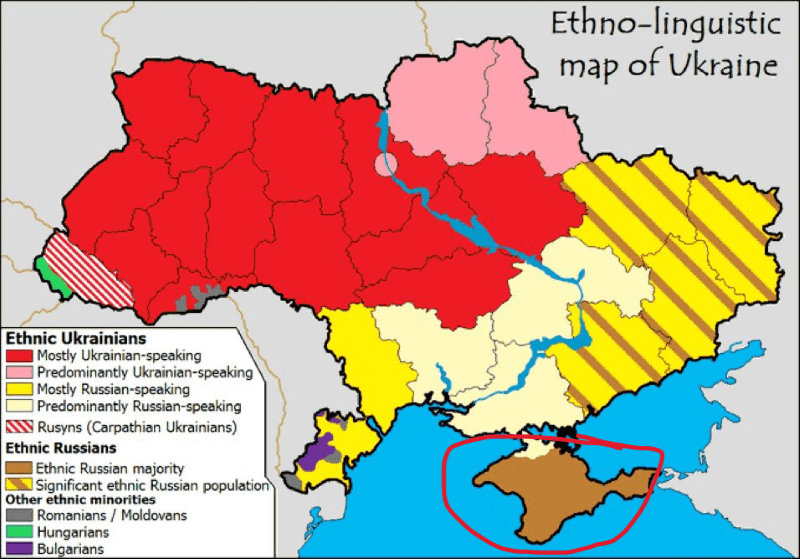

One of the biggest problems with the sanctions is that there's been no endgame articulated for them, and without an endgame, they may never end. The United States has had sanctions on Cuba since 1962. Obviously, the most recent, and most severe sanctions the West imposed on Russia were in response to Russia's invasion of Ukraine, but will the new sanctions be lifted if Russia withdraws its invasion force, or signs a peace treaty with the government of the Ukraine? Or will we demand Russia abandon Crimea (circled below), which is majority Russian ethnically, historically Russian, and includes Sevastopol, the home port of Russia's Black Sea Fleet?

If our condition for lifting the sanctions is Russia abandoning Crimea, then we're likely never going to be lifting them.

What's The Impact?

Our sanctions on Russia are certainly hurting the Russian economy, and making some Russian billionaires slightly poorer, but they are unlikely to pressure Russian President Vladimir Putin into acceding to our demands. Russia is self-sufficient when it comes to food, energy, and weapons, and Putin's powerbase is Russia's siloviki (former KGB types), not its "oligarchs" (a term that, if we're being honest, more accurately describes American centi-billionaires such as Jeff Bezos). As an American, my primary concern is what the sanctions' impact will be on us, but a secondary concern is what the impact will be on those poorer than us.

The immediate impact on America has been most obvious at the pump. Gasoline prices are now at a record high. It's worth noting here that there is a small subset of Americans that is happy about this. I spoke to one representative of this class last week, a New York venture capitalist whose firm has invested in Twitter and numerous other Silicon Valley firms you're familiar with. When I noted that President Biden had inherited $2 per gallon gas, he replied that $2 gas was "a bad thing" because of its impact on the climate. Easy for him to say; for low-income Americans who have to drive to their jobs and can't afford Teslas, record gas prices are a severe hardship.

Americans May Be Poorer; Others May Starve

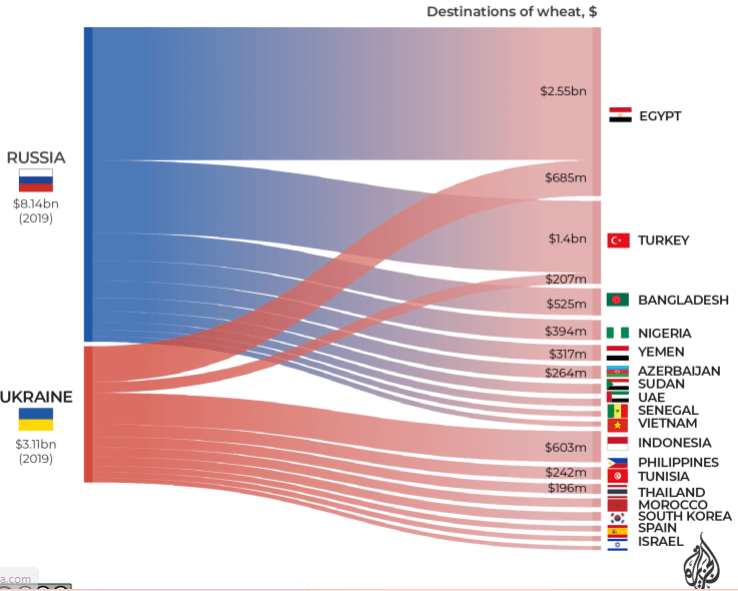

As bad as the impact of continued sanctions may be on America, it will be worse on poorer countries that aren't agricultural power houses. Russia is the world's largest exporter of wheat; Russia and Ukraine combined export 25% of the world's wheat.

Graphic via Al Jazeera.

If our current economic WWIII continues, it could lead to famine in some poorer countries.

Diminishing American Power, Weaker Dollar

Ultimately, our sanctions may lead to diminishing American power, and a weaker dollar, as non-Western countries diversify away from the dollar to avoid having their reserves frozen by us in a future conflict.

This helps explain why the Saudis and others declined Biden's calls recently. What if a future American administration (or possibly the current one) decides the Saudis are worth of the same level of sanctions as Russia, due to the conduct of their war in Yemen?

Investment Considerations

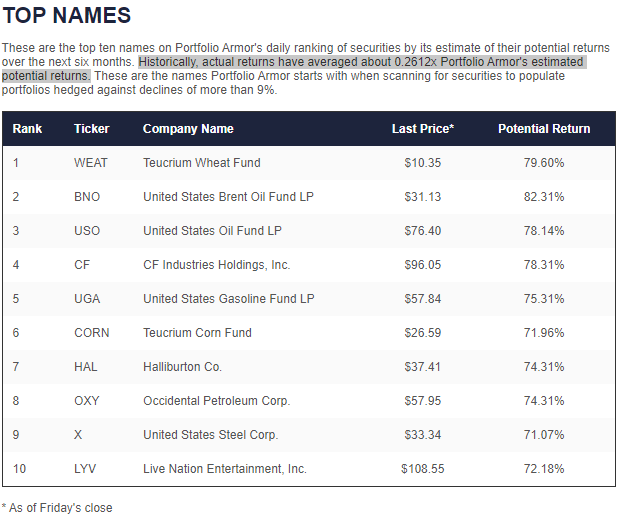

As regular readers know, our system doesn't consider the macro picture when selecting its top names. Instead, it gauges stock and options market sentiment to estimate which securities are likely to perform the best over the next six months. Nevertheless, that bottoms-up approach is painting a clear macro picture when you look at our most recent top ten.

Screen capture via Portfolio Armor on 3/11/2022.

Our number one name on Friday was the Teucrium Wheat Fund WEAT, and two other agricultural names made the list: the Teucrium Corn Fund CORN and nitrogen fertilizer producer CF Industries Holdings, Inc. CF. Fully half of our top ten were oil and gas names including Haliburton Co. HAL, Occidental Petroleum Corp. OXY, and the United States Gasoline Fund LP UGA. Overall, our nine of our top ten names are bets on food and energy getting more expensive over the next six months.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.