The Past Week, In A Nutshell

What Happened: “The bulk of [recent] gains came in the leisure and hospitality sectors, which makes sense because you saw a lot of areas reopening restaurants in May,” said Shawn Cruz, manager of trader strategy at TD Ameritrade. “It just shows how absolutely shut down everything was in March and April. You don’t need much in terms of reopening to get a lot of people going back to work in some regard.”

Remember This: “It’s the beginning of a new business cycle,” said Barry Knapp, managing partner at Ironsides Macroeconomics. “You shouldn’t get all beared up, and you’re not supposed to focus on valuations. This is the early stage of the business cycle.”

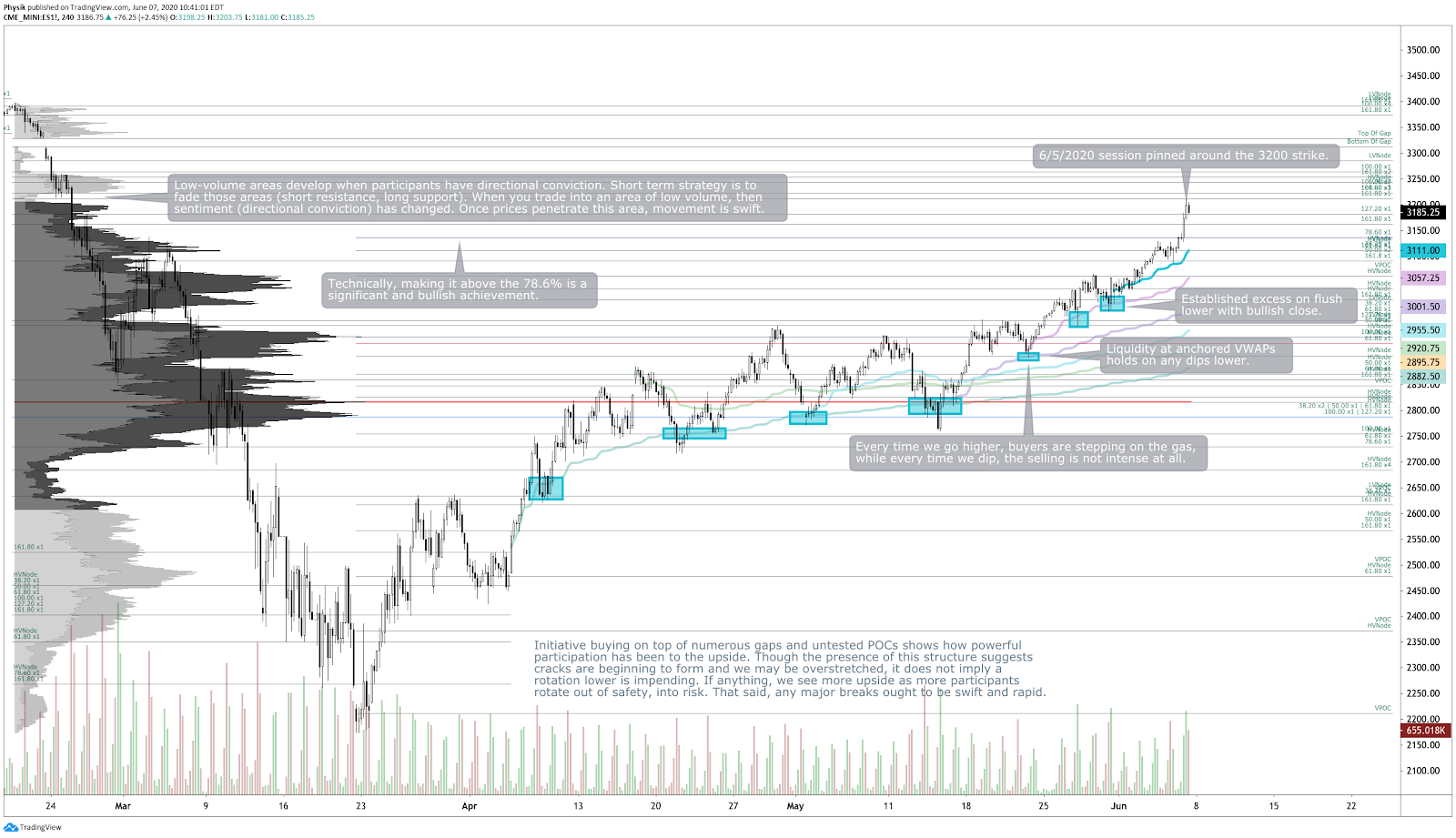

Pictured: Profile chart of the E-mini S&P 500 Futures

Technical

Risk-on sentiment in all major indices. Despite the Nasdaq-100 surpassing its all-time high, the moves have become more muted, signaling a rotation from the bigger technology- and innovation-driven companies to energy, transportation, financials, small caps and so on.

Monday came after an end-of-week flush and a close at the highs. Monday’s overnight action was supported with buyers lifting into the open.

Tuesday’s open seemed exhausted, with some heavy offers developing at and above $3075. Later, the S&P 500 traded down to $3050, an area of resting liquidity, before closing higher.

Wednesday’s session squeezed higher into $3111, came down to some resting bids at $3,090, and then buyers closed the range, again.

Friday opened on a massive gap, exacerbated by the May jobs report. The session ended up balancing at and around the $3,200 strike.

Putting everything together, the picture points to further upside, but it’s obvious that cracks are beginning to form as indicated by the mechanical, short-term momentum-driven activity going on. As long as value shifts higher and liquidations fail to generate any follow-through, then the bullish narrative remains.

Scroll to the bottom of this document to view non-profile charts.

Key Events:

NFIB Small Business Optimism; JOLTS Survey; Wholesale Trade; CPI; PPI; Initial Claims; Import Prices; University of Michigan Sentiment Survey; FOMC Meeting.

Fundamental

- Absent a second wave and geopolitical turmoil, momentum will push markets higher.

- Despite government measures, COVID-19 is wreaking havoc on Latin America.

- Canada added 290,000 jobs as restrictions on business were loosened.

- The U.S. economy added jobs in May with the jobless rate falling to 13.3%.

- The Senate loosened the rules small businesses must follow when applying for PPP.

- The personal care, restaurant, entertainment, and leisure industries are recovering.

- Non-white communities realize an un-equal recovery, worsened by low savings.

- YouTube’s growth paints a bullish picture for Alphabet Inc GOOGL.

- Corporate bond yield spreads reflect expectations of a business cycle upturn.

- Easing of capital outflows from ASEAN markets reduced liquidity pressures.

- China’s manufacturing returned to trend, but the consumer sector is still lagging.

- Repression, or forced lending to the government at low rates, may be bullish.

- By the end of 2020, earnings will be higher than they were in 2019.

- Valuation methods pin fair value for the S&P 500 Index between $2,200 and $2,800.

- Low rates rationalize the outperformance of growth companies.

- Fed’s balance sheet expansion may slow down inflation.

- Expensive stocks have not reached levels seen during the tech bubble.

- Eurozone corona-bonds would help euro-denominated assets outperform.

- OPEC+ agrees to one-month extension of output cuts.

- Ford Motor Company F is evaluating the need for office space.

- Remote work to spark a housing boom in the suburbs and smaller cities.

- Amazon.com AMZN plans sale for June 22 to jumpstart sales.

- ‘Nuclear Option’: U.S. could cut Beijing from the dollar payment system.

- Sentiment: 34.6% Bullish, 26.6% Neutral, 38.9% Bearish as of 6/6/2020.

Product Analysis

S&P 500 (ES)

Nasdaq 100 (NQ)

Russell 2000 (RTY)

Dow Jones (YM)

Gold (GC)

Crude Oil (CL)

Natural Gas (NG)

Treasury Bonds (ZB)

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.