In a recent post (“A New Approach To Portfolio Construction“), we showed a couple examples of Portfolio Armor‘s new portfolio construction tool in action. You may recall our approach there in broad strokes:

- Find securities with the highest expected returns net of their hedging costs (high “net expected returns”) at your particular risk tolerance.

- Hedge them.

That’s our approach when users start with a “clean slate” — that is, they don’t start with their own favorite securities. But in the comments on my last post, I asked commenters on the Slope of Hope trading blog for their favorite long ideas to use for a future post. A few mentioned ideas, but only one ("Bigolded") also gave me a “threshold” to use (i.e., the biggest decline he was willing to risk), so in this post, we’ll show a couple of portfolios based on Bigolded's inputs.

Creating Hedged Portfolios For Bigolded

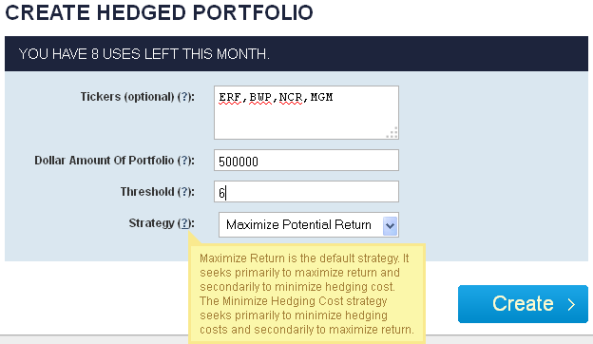

Bigolded mentioned four securities: Enerplus Corporation ERF, Boardwalk Pipeline Partners BWP, NCR Corp. NCR, and MGM Resorts International MGM, and said he didn’t want to risk more than a 6% decline in the value of his portfolio. He didn’t mention the size of his portfolio, so I’ve just picked $500,000 as a round number below. So, here’s how we go about creating a hedged portfolio for him.

-

We enter his tickers in the first field below (“Tickers”), “500000″ in the second field (“Dollar Amount Of Portfolio”), and, for our first example, we stick with the default strategy (“Maximize Potential Return”).

-

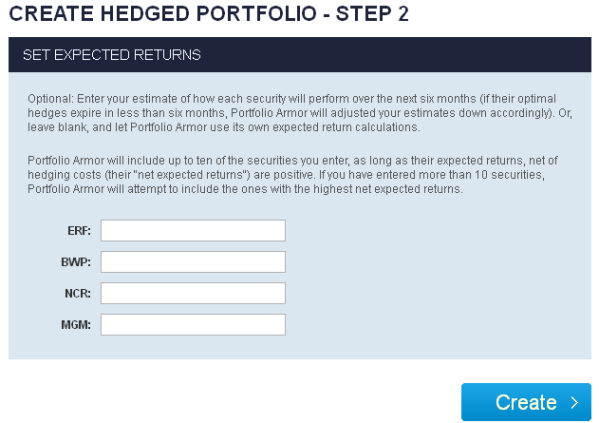

In the next step, you can pick our own six month expected returns for these stocks, or you can leave these fields blank, as I have done here, and let Portfolio Armor use its own expected return calculations, which are based on its analysis of the securities’ historical returns and current options market sentiment about them.

-

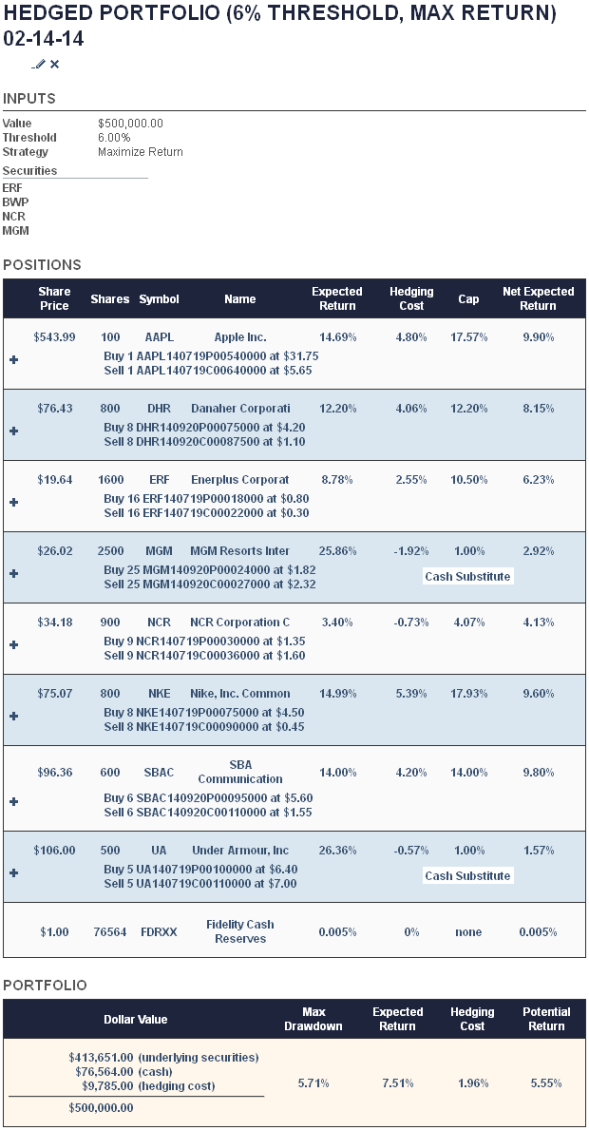

And, after clicking the “Create” button above, we’re done. Here’s our hedged portfolio:

Each Security Is Hedged

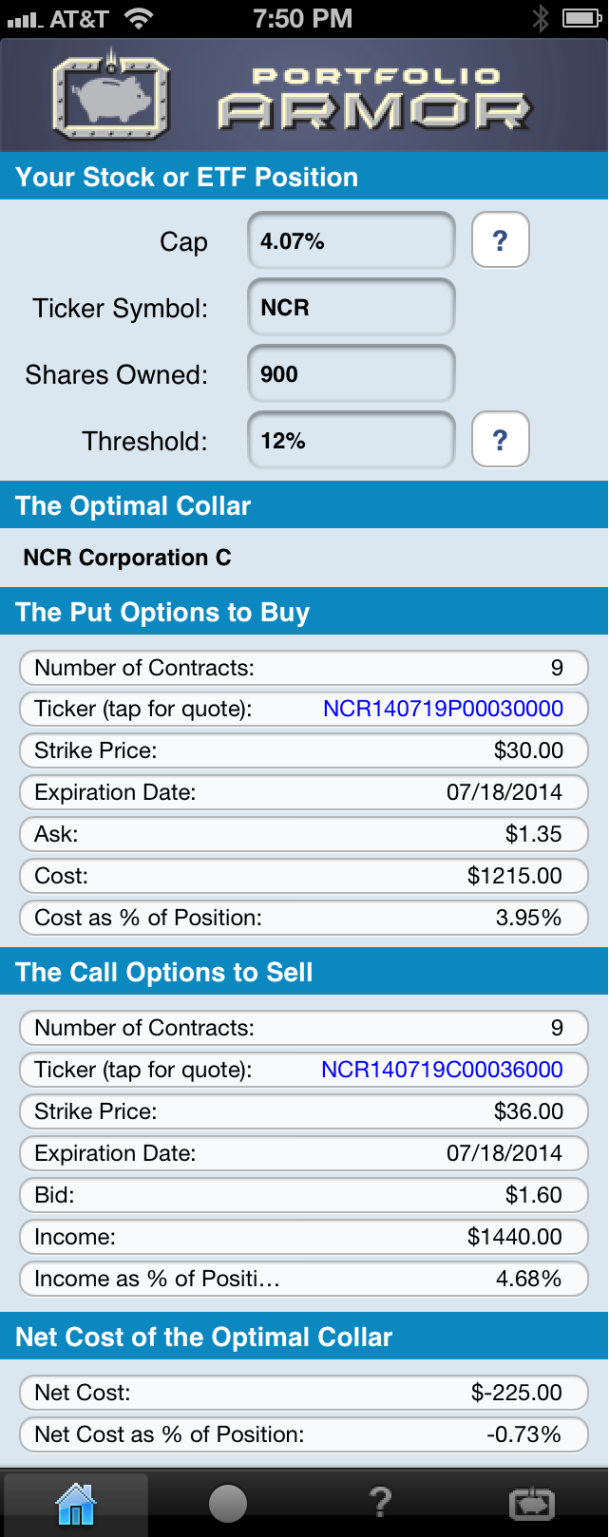

Note that in the portfolio above, each of the underlying securities is hedged. Hedging each security according to the investor’s risk tolerance obviates the need for broad diversification, and lets him concentrate his assets in a handful of securities with high expected returns net of their hedging costs. Here’s a closer look at the hedge for one of these positions, NCR:

This collar for NCR was capped at 4.07%, because that’s the six month expected return Portfolio Armor calculated for the stock. The threshold Portfolio Armor used here was 12% though, not the 6% BIgolded mentioned. The reason for that is that NCR was too expensive to hedge using a 6% threshold, so Portfolio Armor used a threshold twice as large, but reduced the position size by half so that the maximum drawdown of BIgolded’s portfolio was less than 6% (5.71% actually, as you can see at the bottom of the previous screen capture). Note also that the hedging cost for NCR here was negative, meaning BIgolded would be getting paid to hedge it.

Three Out Of Four Securities Included

The only one of Bigolded's tickers that wasn’t included here was BWP, because, its net expected return was negative. MGM was included hedged as what we call a cash substitute — that’s a security collared with a tight cap (1% or the current yield on a leading money market fund, whichever is higher) in an attempt to capture a better-than-cash return while keeping the investor’s downside limited according to his specifications. MGM was hedged this way because it was too expensive to hedge otherwise using a 6% threshold. The algorithm rounded out his portfolio by adding a few additional securities that had high net expected returns: Apple, Inc. AAPL, Danaher Corporation DHR, Nike, Inc. NKE, SBA Communications SBAC, and Under Armour UA. Under Armour and MGM were hedged as what we call "cash substitutes": that's a security collared with a tight cap (1% or the current yield on a leading money market fund, whichever is higher) in an attempt to capture a better-than-cash return while keeping the investor's downside limited according to his specifications.

Hedging Cost And Potential Return

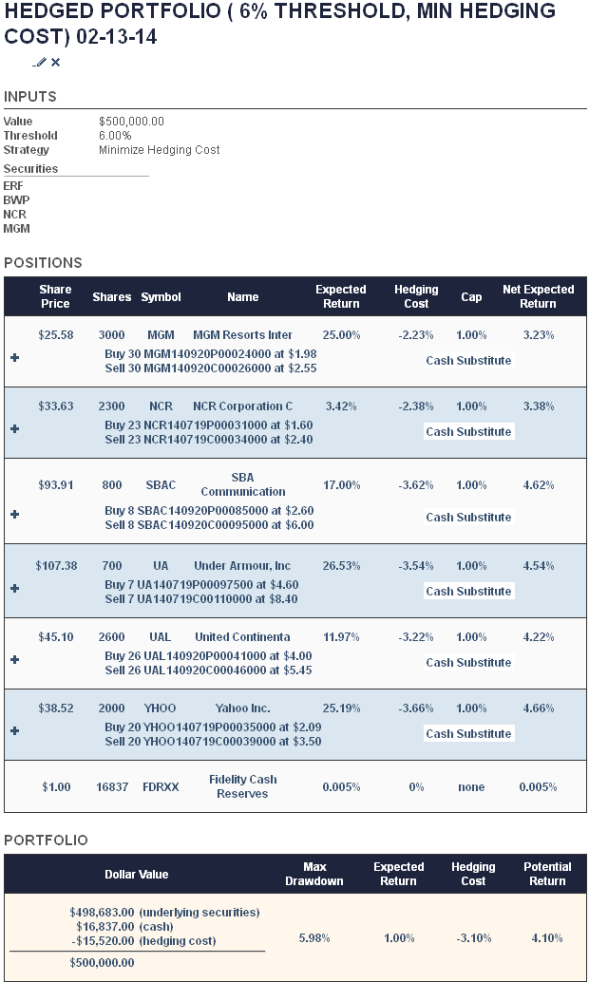

The hedging cost of this portfolio was 1.96%, and its potential return over the next six months was 5.55%. In general, the higher the risk you’re willing to take (the larger your threshold), the higher your potential return. For an example of a hedged portfolio using a 20% threshold, see this post. If BIgolded felt the hedging cost of 1.96% was too high, he could run this again, using our second strategy, “Minimize Hedging Cost”. If he did, he would have gotten this portfolio:

As you can see at the bottom of the screen capture above, the potential return of this portfolio over six months was a little bit lower, at 4.10%, but the hedging cost was negative in this case, -3.10%, meaning the investor would have gotten paid to hedge. Two new securities appear in this portfolio: Yahoo, Inc. YHOO, and United Continental UAL.

The worst case scenario for this portfolio would be if each of the underlying securities went to zero over the next six months. If that happened, the investor would be down 5.98%. The best case scenario for this portfolio would be for each of these underlying securities to appreciate by more than 1% next week. If that happened, they’d get called away, and the investor would be up at least 4.1% (he might be able to make a bit more by selling the put legs of his collars).

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.