The Viridian Cannabis Deal Tracker is an information service that monitors capital raise and M&A activity in the legal cannabis industry. Each week the Tracker analyzes/aggregates all closed deals and allocates each transaction to one of twelve key industry sectors in which the deal occurred (from Cultivation to Brands), the region in which the deal occurred (country or U.S. state), the status of the company announcing the transaction (public vs. private) and the type of deal structure (equity vs. debt).

The Viridian Cannabis Deal Tracker provides the deal data/terms/valuations/structures and market intelligence that cannabis companies, investors, and acquirers utilize to make informed decisions regarding capital and M&A strategy. Since its inception in 2015, the Viridian Cannabis Deal Tracker has tracked and analyzed more than 2,500 capital raises and 1,000 M&A transactions totaling over $45 billion in aggregate value. Find it exclusively on Benzinga Cannabis every week!

INVESTMENT AND M&A ACTIVITY IN THE CANNABIS INDUSTRY

11/9/2020 - 11/13/2020

CAPITAL RAISES

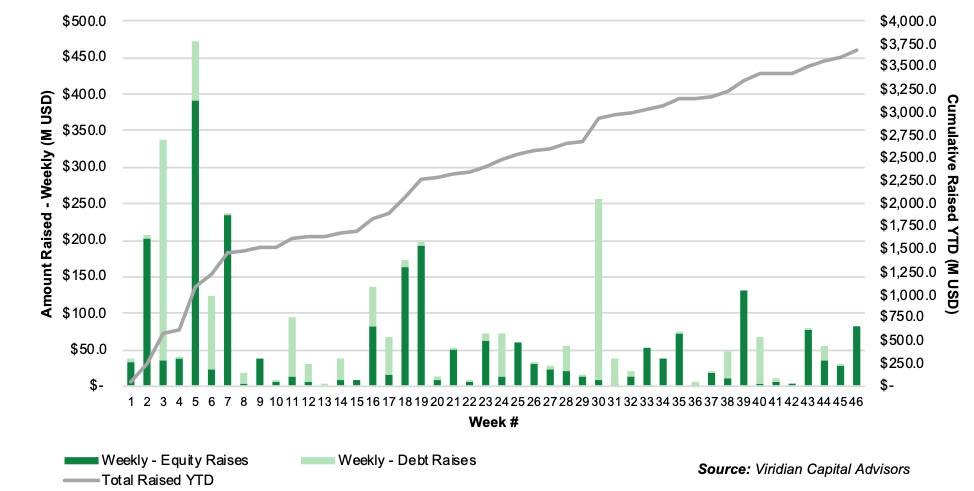

- Transactional Activity: Week 46 ended November 13, 2020, saw a $54.8 million higher dollar volume and 2 more transactions vs. the prior week of this year and a 260% higher dollar volume with two more transactions vs the prior-year period. We tracked 5 capital raise transactions totaling $82.8 million, vs 3 transactions totaling $23.0 million during the same week in 2019. The average tranche size was $16.6 million this week, vs. $7.7 million in the prior-year period.

- Largest Cap Raise: On November 12, 2020, Organigram Holdings OGI OGI, the 8th largest Canadian LP by market cap, completed its previously announced C$69.1 million (US52.6M), underwritten public offering of 37.375 million units at C$1.85 (US$1.41) per unit. Each unit consisted of one common share and one half of a common share purchase warrant with a term of 3 years and an exercise price of C$2.5 (US$1.90) per share (a premium of approximately 35%). We value this warrant at approximately C$0.32 (C$0.16 per unit) giving a net stock price of C$1.69. The stock closed at C$1.49 per share on the transaction date, reflecting significant pressure from the financing and finishing the week down 33% from the prior week and approximately 54% YTD. Investors have been disappointed by the company’s inability to turn around its revenues which were down 27% in the third quarter compared to the previous year and 22% sequentially from the 2nd quarter. This decline comes despite the company’s strategy shift to pursue the value segment of the Canadian cannabis market, a segment that has not been kind to OGI or most other players. This strategy seems perplexing since it completely reverses the company’s original premium product positioning and it seems to us rather unlikely that the company can compete on costs versus its larger competitors. After cutting staffing by 25%, slashing Capex, and drawing down the remaining $30 million on its term loan, many thought that the company was well-positioned liquidity wise, ergo the violent market reaction to this week’s capital raise. OGI now trades at 2.4x 2021 consensus revenue estimates, directly in line with the 2.5X median we observe for the 17 Canadian Cultivation & Retail companies we track with market caps over $25 million. Perhaps more telling however is the company’s .94X market to book ratio compared to the group median of 1.8x. This discount is after the company’s C$37.3 million (US$26.5M) asset impairment charge taken in the third quarter.

- Public vs. Private Cap Raises: All 5 of this week’s capital raises were closed by public companies. So far in 2020, public companies have accounted for 82% of all capital raises, vs. 65% for the same period in 2019. In 2020, public companies have accounted for 79% of total dollars raised, vs. 69% for the same period in 2019.

- Public Company Listings: Of the 5 public company capital raises, all are listed in Canada (2 on the CSE and 3 on the TSX), and all 5 also trade on secondary exchanges (4 on the OTC and 1 on the NASDAQ).

- Equity vs. Debt Cap Raises: Equity-based capital raises accounted for all of this week’s closed capital raises.

- 2nd Largest Capital Raise: On November 9, Cloud MD Software & Services DOC DOCRF, a technology company which provides SaaS-based health technology solutions to medical clinics in Canada, closed its previously announced bought deal offering of 15.525 million shares at C$2.40 per share (US$1.84) for gross proceeds of C$37.26 million (US$28.64M). The price was 77% higher than that of the company’s last equity raise in September. DOC has been active in the M&A market as well, completing 2 acquisitions of other software companies and 1 acquisition of a medical clinic year-to-date for a total consideration of approximately $7.4 million.

- Cap Raises by Sector: The 5 capital raises this week were spread across 3 different industry sectors with two each in Cultivation & Retail, one in Infused Products and Extracts, and one in Software/Media.

MERGERS & ACQUISITIONS

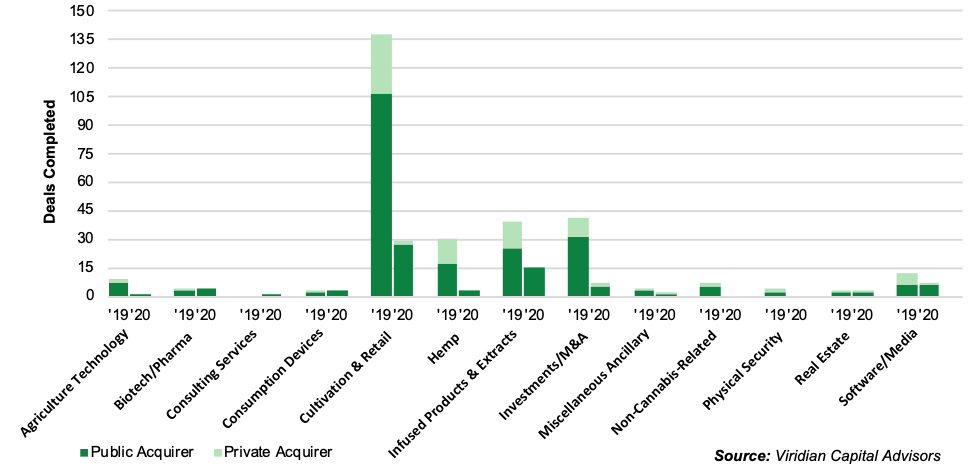

- Transactional Activity: Week 46 saw 2 M&A transactions, up from none in the prior-year period. Although the number of M&A transactions completed year-to-date is down 74% vs the comparable period of 2019, recently announced deals, newly adult legalized states, and the ticking of the SPAC timeclock all argue for near-term acceleration of M&A activity.

- Largest M&A Transaction: On November 12, Trulieve Cannabis TRULTCNNF a dominant competitor in the Florida market and one of the most profitable American cannabis companies, closed the acquisition of cultivator and producer PurePenn LLC and Pioneer Leasing & Consulting LLC (collectively, “PurePenn”) and dispensary operator Solevo Wellness (“Solevo”). Total consideration for the transactions was approximately C$66 million (US$50.2 million) composed of $29 million in cash and 1.78 million subordinate voting shares of the company. The acquisitions make Trullieve an integrated competitor in the rapidly growing and highly profitable Pennsylvania market with a 35,000 square foot cultivation and processing center that is expected to be expanded to 90,000 square feet in Q1 2021 as well as three Pittsburgh area dispensaries. Pennsylvania is one of the most attractive limited license medical states in the country after Florida, which Trulieve dominates, and the state is thought to be a likely adult legalization candidate in the next year. Pennsylvania adds the fifth state to Trulieve’s portfolio which also includes California, Connecticut, and Massachusetts along with Florida. Trulieve has been one of the best performing U.S. cannabis stocks, up approximately 143% year to date. After this strong run-up, the company now trades at approximately 4.5x consensus 2021 revenue estimates and 10.1x 2021 EBITDA estimates, compared to 2.4x and 10.4x medians for the 20 U.S. cultivation & retail sectors companies we track with market caps over $50 million. Today, Trulieve announced record results for the quarter ended 9/30/20, with revenues of $136 million (up 13% sequentially and above consensus), Adjusted EBITDA of $68 million (also above consensus and representing an industry-leading margin of 50%), and a cash balance of $193 million, portending continued aggressive expansion.

- Public vs. Private: Both of this week’s two acquisitions were made by public companies. Year-to-date, 91% of M&A transactions closed in 2020 have been made by public companies (up from 71% in 2019). Public companies, particularly with the recovery in stock prices and fundraising ability, have been the dominant acquirers in the cannabis industry. Private companies remain the dominant targets for acquirers.

- M&A by Sector: One of the buyers in this week’s transactions came from the Cultivation & Retail sector and the other came from the Software/Media. Targets came from the Cultivation & Retail and the Hemp Sectors.

WEEKLY SUMMARY

EQUITY RAISES

DEBT RAISES

MERGERS & ACQUISITIONS

YEAR-TO-DATE SUMMARY

CAPITAL RAISES

Capital Raises by Week

Capital Raises by Sector

MERGERS & ACQUISITIONS

M&A Activity by Week

M&A Activity by Sector

Photo by Javier Hasse.

The preceding article is from one of our external contributors. It does not represent the opinion of Benzinga and has not been edited.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Click on the image for more info.

Cannabis rescheduling seems to be right around the corner

Want to understand what this means for the future of the industry?

Hear directly for top executives, investors and policymakers at the Benzinga Cannabis Capital Conference, coming to Chicago this Oct. 8-9.

Get your tickets now before prices surge by following this link.