(Tuesday Market Open) Consumer price growth slowed to a crawl in November, fueling arguments that inflation is starting to ease. Stock futures rallied early Tuesday after the news.

The November Consumer Price Index rose 0.1% versus analysts’ consensus expectations of 0.3%. Core CPI, which strips out volatile food and energy prices, rose 0.2% in November, again below the 0.3% consensus. Prices were up 7.1% from a year earlier.

The headline and core CPI had been 0.4% and 0.3% in October, respectively. Improvement in these month-over-month figures is crucial, and now we’ve had two months in a row of cooling monthly data.

It’s not surprising to see the Nasdaq Composite®($COMP) leading gains after the CPI data, as many growth stocks are more sensitive to higher interest rates. Today’s CPI likely solidifies ideas that the Federal Reserve will hike rates by just 50 basis points tomorrow, down from 75 basis points at its previous four meetings.

In another CPI-related morning development, the 10-year U.S. Treasury yield (TNX) plunged 12 basis points immediately after the report to 3.48%. The 2-year Treasury yield, the most sensitive to the Fed’s interest rate policy, fell even more, and was down 16 basis points at 4.23%.

Inflation data is also rolling in today from outside the U.S. Germany’s November CPI fell to 10% from 10.4% in October and came in near analysts’ expectations. The European Central Bank (ECB) meets this week and analysts expect a 50-basis-point rate increase.

Morning Rush

- The 10-year Treasury yield (TNX) fell 12 basis points to 3.48%.

- The U.S. Dollar Index ($DXY) fell below 104 for the first time since late June.

- Cboe Volatility Index (VIX) futures dropped sharply to just above 22.

- WTI Crude Oil (/CL) is up 0.5% at $73.50 per barrel.

Fed Prepares to Meet

As the Federal Open Market Committee (FOMC) meeting begins this morning, the CME FedWatch Tool projects 79% chances of a 50-basis-point rate hike tomorrow.

- The median Fed terminal, or peak, rate was 4.6% back in September when it last made a projection. That’ll be updated Wednesday, and may be one of the first numbers market participants check. Wall Street now looks for a terminal rate somewhere in the 5% to 5.25% range.

- Other updates we’ll get with the rate decision at 2 p.m. ET tomorrow are the Fed’s economic and rate projections. The rate projections will be scrutinized for clues about the path of hikes next year, while the economic projections will provide insight into how the Fed expects inflation, unemployment, and Gross Domestic Product (GDP) to progress in 2023.

- In tomorrow’s dot-plot, FOMC members are each asked to plot where they think rates will be at the end of each year. This will be the first updated dot-plot since September. The key thing to watch on the dot plot will be whether the Fed expects rates to begin falling late next year. There’s expectation for a bit of a drop in late 2023, and the path of the dot plot next year could be the next volatility-inducing data point.

In the September dot plot, most FOMC members expected 2022 to end with the benchmark rate between 4% and 4.5%. A 50-basis-point hike tomorrow would get us within that range.

Potential Market Movers

Late yesterday, shares of enterprise software company Oracle (ORCL) jumped 3% in post-market trading following a solid earnings report. Revenue and earnings per share (EPS) beat Wall Street’s estimates, and revenue actually came in $200 million ahead of Oracle’s own expectations, something you don’t hear too much lately.

The company’s closely scrutinized cloud business showed none of the troubles that dimmed recent earnings for some of its competitors. The infrastructure cloud business grew 59% in the quarter and cloud-based applications rose 45%.

While ORCL is just one company, it does have an impressive global footprint. Seeing its cloud business look so healthy could raise spirits about corporate technology spending in general, contrary to the negativity some analysts penciled in after disappointing quarterly cloud performance from Amazon (AMZN) and Microsoft (MSFT).

So why isn’t ORCL up more? Perhaps because of some mixed guidance for the current quarter.

Reviewing the Market Minutes

Following last week’s swoon, Monday started with a bang—for stocks, anyway. The bond market dipped to begin the week, hurt in part by soft demand seen in a government auction for 10-year Treasury notes. The 10-year Treasury yield (TNX) rose five basis points to 3.61%, though it’s unclear if that rise in yields (which move in the opposite direction of the underlying note) had more to do with weak demand at the auction or investor concerns heading into today’s CPI data.

Over on Wall Street it was a different story. The mood seemed upbeat, possibly on ideas the market might’ve become oversold after falling in six of the previous seven sessions. A comeback in WTI Crude (/CL) after it hit new 2022 lows last week gave energy stocks a nice boost. Merger and acquisition news from Amgen (AMGN)—which announced plans to acquire Horizon Pharmaceuticals (HZNP)—may have helped improve sentiment. So did news that Microsoft (MSFT) would acquire a 4% stake in the London Stock Exchange as part of a strategic partnership for data analytics and cloud technology.

Here’s how the major indexes performed Monday:

- The Dow Jones Industrial Average® ($DJI) climbed 528 points, or 1.58%, to 34,005.

- The $COMP rose 1.26% to 11,143.

- The Russell 2000®(RUT) added 1.22% to 1,818.

- The S&P 500® index (SPX) rose 56 points, or 1.43%, to 3,990.

Talking Technicals: Last week we noted the SPX continued to find technical support in a range between 3,920 and 3,940. It closed right in the middle of that Friday at 3,934; it then tested that level on an early downturn Monday. When buyers stepped back in, the index quickly pivoted and began putting on weight, ultimately closing at its highest level (3,990) in exactly a week.

Now the level to watch is last week’s 3,998 intraday high and above that the 200-day moving average (MA) of 4,035. Down below, some technicians see 3,955 as a point to watch on any pullbacks. The SPX has traded in a very tight range between roughly 3,900 and 4,080 for a month now, so it’ll be interesting to see if this fresh volatility indicated by the VIX changes that.

Speaking of 200-day MAs, the $DXY closed below its own 200-day MA Monday for the third consecutive session. That particular trendline had been important support for the $DXY for more than a year, but now the net appears to have a hole.

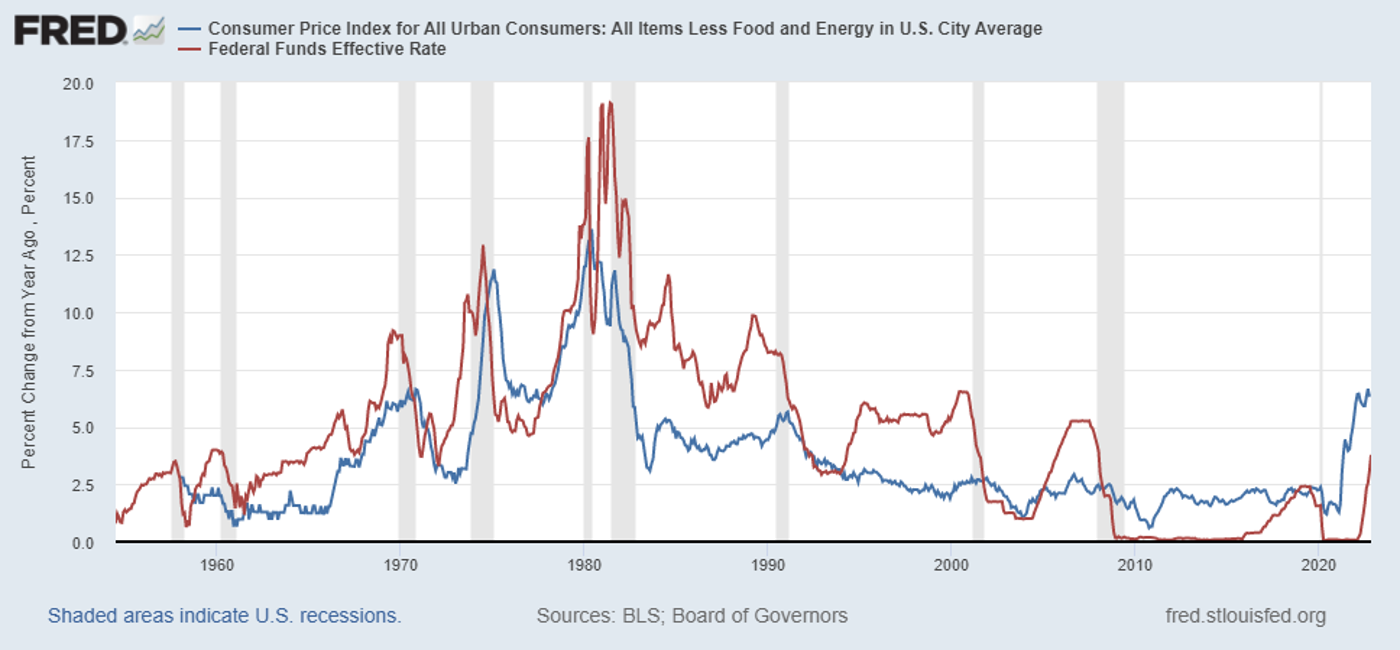

CHART OF THE DAY: WIN! Those of us who were around back in the 1970s remember the government’s “Whip Infation Now (WIN) program, but the chart above comparing the Consumer Price Index (blue line) to the Fed funds rate (red line) shows that many times the Fed thought it had inflation “whipped,” pulled back rates, and then found out inflation wasn’t down for the count. Fed officials may be wary now of repeating those mistakes in 2023 as they watch inflation start to slow. Data Source: St. Louis Fed. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

Don’t Mothball the Drilling Rigs Just Yet: The U.S. government’s announcement of a fusion breakthrough made headlines yesterday and could pay long-term dividends. However, traditional and alternative sources of energy aren’t going away anytime soon, according to experts. To paraphrase what one scientist told CNN, hearing this week’s fusion news and asking about its ultimate practical payoff would be like hearing about an embryo and asking when it’s going to graduate from Harvard. The government’s experiment did create a net energy gain using fusion, but a whole lot more energy would be needed to run a power plant—the ultimate goal of many fusion pioneers.

Who’s Investing in Fusion? Most companies working on fusion are at the venture level and not yet available to the general investor. Private investors poured a record $3.4 billion into fusion last year, Bloomberg recently reported, citing research firm Pitchbook. Some of the investments come from the venture arms of public companies, including Chevron (CVX) and Alphabet (GOOGL). Bloomberg Intelligence Strategist Mike Dennis pegged the eventual nuclear fusion market at $40 trillion. Even if its initial contribution to the world’s total energy output is tiny, Dennis said fusion will remake energy markets the way Tesla (TSLA) remade the automobile industry. However, he didn’t say by when.

Budget Meals: It may seem like a head fake when we talk about middle- to higher-income shoppers looking for bargains at the grocery store during inflationary times. Bank of America Institute (BofA) made the point that wealthier customers simply have more flexibility to retrench, while lower-income shoppers generally hit the margins earlier and harder. However, this year, many wealthier customers have clearly changed their habits, according to BofA. It reported October spending at “value tier” grocery stores by shoppers with annual incomes above $100,000 was up 22% relative to January 2019 levels. One possible explanation? Higher-income consumers—not to be confused with the super-wealthy—have “experienced negative real wage growth for most of this year,” and that persistent inflation “is taking a toll.” The Atlanta Fed reported that wage growth for the nation’s top-income quartile was 4.5%, well below the CPI figure that grew 7.7% during October. How sticky will these retail choices be when the economy recovers? That’s an opportunity many retailers and their shareholders may want to keep an eye on.

Notable Calendar Items

Dec. 14: FOMC rate decision, quarterly projections and dot-plot, November Export and Import Prices, and expected earnings from Lennar (LEN)

Dec. 15: November Retail Sales, December Empire State Manufacturing, and November Industrial Production and Capacity Utilization

Dec. 16: Expected earnings from Accenture (ACN)

Dec. 19: No earnings or data of note

Dec. 20: November Housing Starts and Building Permits and expected earnings from General Mills (GIS) and Nike (NKE)

Dec. 21: November Existing Home Sales and expected earnings from Rite Aid (RAD) and Micron (MU)

Dec. 22: Government’s final Q3 GDP estimate and expected earnings from CarMax (KMX)

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.