Did you see the video footage over the weekend of those trucks leaving the Pfizer Inc. PFE manufacturing plant in Michigan—the ones filled with the first shipments of the coronavirus vaccine it developed with BioNTech SE BNTX? It seems many investors did, which could be helping lift markets to start the week.

Ahead of the open Monday, stocks were regaining some of the ground lost last week. Also—in a reversal from the action late last week—the Cboe Volatility Index (VIX) has eased a bit, and crude oil futures (/CL) look to be renewing their advance toward $50. In other words, the “risk-off” sentiment that seemed to rule the end of last week may be unwinding a bit.

With the vaccine rollout underway, investors were also looking at another issue that’s been on their mind recently—potential stimulus from Congress. Reuters reported that a bipartisan plan could be introduced as early as today, news which seemed to be cheering investors. Still, it remains to be seen whether Congress can dot the Is and cross the Ts to get a deal done.

Also helping sentiment is the more congenial tone between the United Kingdom and the European Union as the deadline approaches for the U.K’s pullout from the common market.

A Quick Review Of Last Week’s Action

Last week, vaccine optimism clashed with worries about rising COVID-19 infections and a worsening employment picture. It didn’t help that Brexit once again was in the headlines amid worry that the United Kingdom’s divorce from the European Union might come before a trade agreement could be reached.

One of the main things that ended up helping drag stocks lower for the week was waning investor hope for a congressional stimulus package as the debate on more federal coronavirus aid dragged on in Washington.

Wall Street seems to have sided with the Federal Reserve in thinking that more help from Capitol Hill is needed for Main Street as the pandemic continues and widespread availability of the vaccine is still a ways away.

While the Fed’s bond-buying program that covers Treasuries, corporate bonds, and mortgage-backed securities has been a big help for Wall Street, helping make these recent record highs possible, it’s also arguable that congressional stimulus such as extra unemployment help and checks deposited in bank accounts have done more for the average Joe and Jill.

Without another round of stimulus, investors and traders are apparently worried that, despite the stock market’s success this year, the pandemic’s effects on consumer spending could end up greatly delaying the economic recovery.

Fed Up To Bat This Week

Speaking of the Fed, this week investors are scheduled to get to hear more from the central bank. It’s two-day policy-setting meeting is scheduled to conclude on Wednesday afternoon.

Investors are expecting the central bank to stand pat on interest rates (100% certainty, according to the CME FedWatch tool, which uses futures prices to calculate rate-move probabilities). We’ll see if the Fed makes any comment on the need for further congressional stimulus—assuming one hasn’t been agreed on by then.

Investors also might want to know more about what the Fed thinks about the Treasury’s decision to let several emergency lending programs expire on the last day of the year and whether monetary policy makers think they have other tools than what they’ve already used to help the economy, and by extension the markets.

In addition to the Fed meeting, this week’s economic calendar also includes readings on November industrial production, retail sales, housing starts and building permits.

The weekly unemployment claims report will also likely be closely watched. The report, once a relatively sleepy affair, has come to have more significant impact on trading during the pandemic because it offers a more up-to-date reading on the labor market than the government’s monthly employment situation report.

Another thing that investors may want to keep an eye on is quadruple witching day this week. Friday is one of four days a year (once a quarter) when contracts for stock index futures, stock index options, stock options, and single-stock futures all expire.

Traditionally, markets tend to see elevated volatility around these days, so it’s possible we could see some extra price movement as the week goes on.

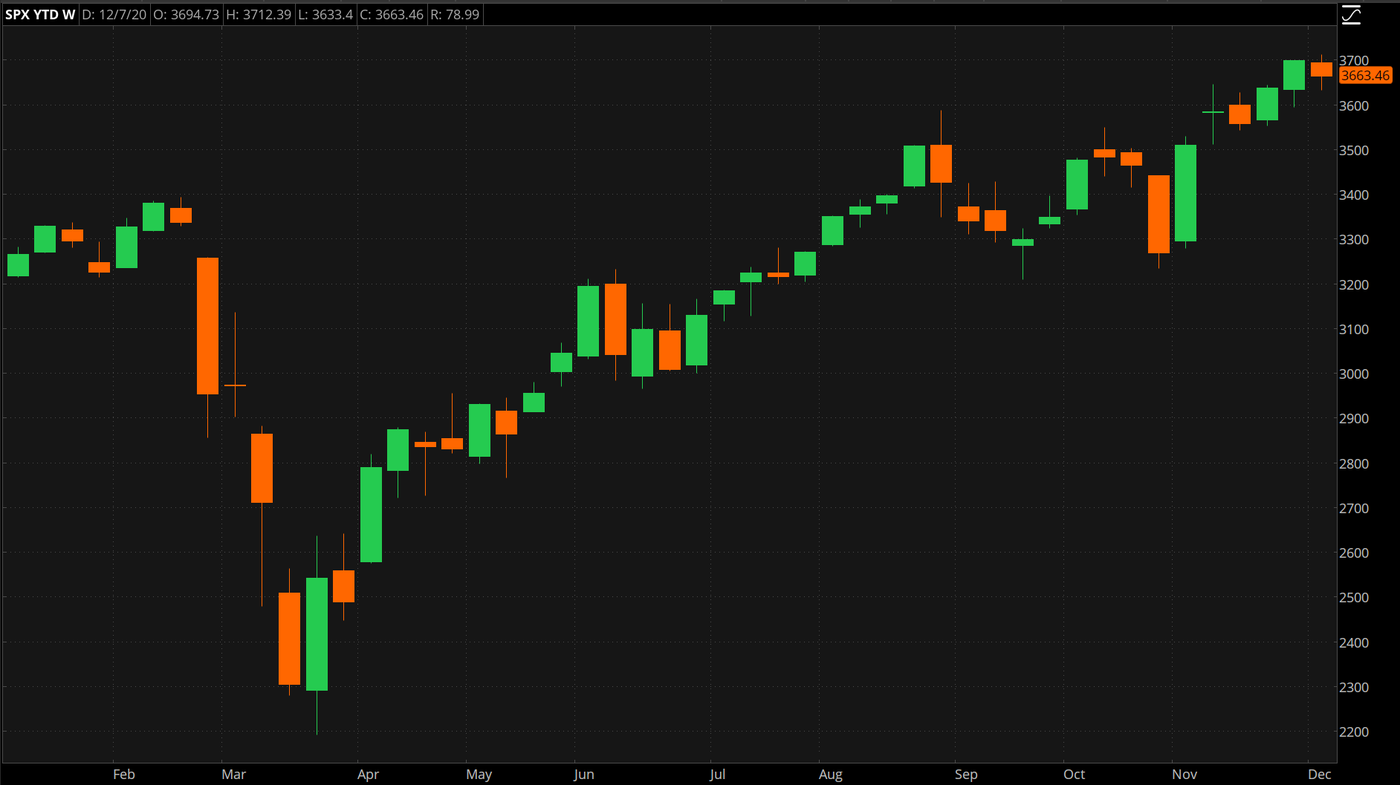

CHART OF THE DAY: After reaching into record territory, the S&P 500 Index (SPX—candlestick) ended up having its first down week in three, as you can see from this chart of weekly gains and losses so far this year. Stocks lost some momentum as the congressional debate over a new coronavirus stimulus package continued to drag on. Rising infection numbers, worse-than-forecast jobless claims data, and Brexit worry didn’t help. Data source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Not Out of the Woods: Although the latest consumer sentiment index from the University of Michigan showed a surprising gain, the chief economist for the university’s Surveys of Consumers, Richard Curtin, had some sobering words. Most of the early December gain was due to a more favorable long-term outlook following the presidential election. But expectations for the year ahead for the economy and personal finances remained unchanged. “In the immediate future, job losses and income declines due to shutdowns are expected to increase, and the long priority queues before most consumers can be vaccinated will make the wait amid rising deaths all the more difficult to endure,” Curtin said in commentary accompanying the numbers. While he said a new round of federal stimulus will prevent much greater financial harm to households, small businesses, and local governments, “even if immediately adopted, the payments will not reach recipients for at least a month, allowing renewed hardships to dominate the holiday season.”

Holiday Shopping: This week, the monthly retail sales data may be particularly of interest to investors as those numbers offer a good way to get a sense of the pulse of the domestic consumer. The figures will be for November, which included Black Friday, a day many retailers rely on to get themselves out of the red and into the black. A strong showing could bode well for all of the holiday shopping season, but a poor showing might portend the opposite. A good bit of how well retailers did probably has to do with how well they were able to capitalize on promotions for online shoppers who remained at home amid the resurgence of the COVID-19 pandemic.

Glowing Embers: Inflation readings were pretty tame last week, as you might expect with the economy still weighed down by the pandemic. But there was inflation, and the fact that it registered at all seems to be a good sign. The November core consumer price index showed 0.2% month-on-month growth, which was in line with a Briefing.com consensus. And the core producer price index came in at 0.1% growth, slightly shy of a Briefing.com consensus expectation of 0.2%. When you look at annualized data for core CPI, it was 1.6%, which is well below the Fed’s 2% inflation target. (Keep in mind that the Fed’s preferred inflation gauge is the core personal consumption expenditures price index.) Some inflation can indicate a healthy economy, but too much can mean things are overheating. We seem quite far away from that latter scenario and the Fed rate tightening that would probably go with it. As Briefing.com put it, in reference to last week’s CPI report: “There aren’t any inflation alarm bells (or rate-hike bells) ringing in this report for the Fed.”

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Hans Reniers on Unsplash

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.