Fintech’s role as a disruptor in the financial space often aligns it with other technologies that have fundamentally altered the industries to which they were introduced. Just as streaming effectively drove video rental to digital-only, the promise of fintech is often portrayed as the displacement of stodgy brick-and-mortar banks in favor of primarily online banking.

While that’s certainly a component of fintech’s influence on the financial industry, the way in which it is playing out in lending—arguably the largest aspect of fintech’s disruption in finance—reveals a far more complex relationship between big banks, community banks and their fintech counterparts,

A Slice Of The Loan Size Pie

At the moment, the lending ecosystem seems to encourage parity between the three classes of lenders. According to information gathered from ValuePenguin, the average business loan among large, national banks is $593,000 and those among smaller community banks is $146,000, while small business lending fintech, Credibly, puts their average loan at about $55,000.

Intuitively, these ranges seem to suit the loan portfolios of the financial entity servicing them, with large banks focusing on large accounts, fintechs addressing smaller, underserved loans, and community banks covering some range in the middle.

However, another takeaway might be that, as fintech lenders gain greater awareness and sophistication, the size of the loans they could effectively service will start to cut into the loans of regional and community banks. In fact, there are some indications that this may already be taking place.

Credibly’s Director of Marketing, Jeffrey Bumbales, noted that “While our average loan size hasn't changed much, the units certainly have. We see a lot more in the $5,000-$10,000 range than we used to, which is being offset by larger loans that maintain that $55K - $65K average.”

Couple that with the rapid decline in the total amount of banks over the past 30 years, from more than 14,000 in 1986 to fewer than 5,000 in 2017, and it’s not difficult to see the existential threat fintechs seem to pose smaller financial institutions.

Strange Bedfellows

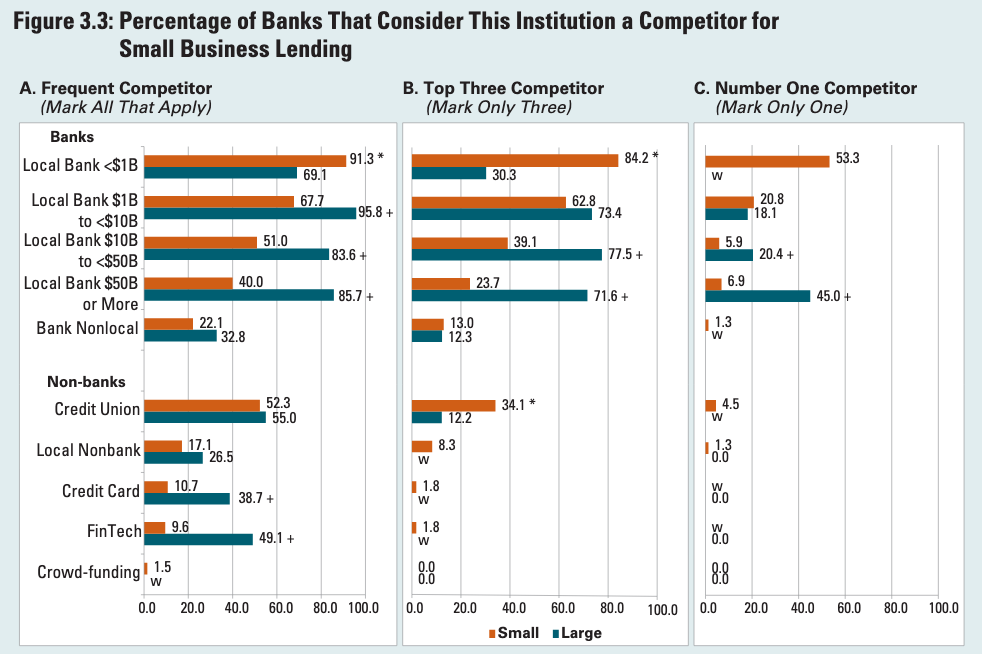

It might then be surprising that, according to the 2018 FDIC Small Business Lending Survey, it was large banks that noted fintech as among the biggest non-bank competitors, just behind credit unions. While more small banks did list fintech as a more direct competitor to their business lending than big banks, larger banks were by far a larger concern.

Source: FDIC Small Business Lending Survey

While this might seem puzzling, fintech’s relationships with small banks has never really been adversarial. Instead, community banks have found a powerful partner in financial technology startups that have allowed them to hold their own against financial monoliths like JPMorgan Chase & Co. JPM and Goldman Sachs Group Inc. GS, which have invested tens of billions of dollars into developing their own digital offerings.

Small Town Tech

Following the regulatory and technological upheaval that trailed the 2008 financial crisis, many community banks recognized the unique position they were in to foster these technologies through stringent and constantly changing federal oversight while also gaining a leg up over their national counterparts. Examples of partnerships like Radius Bank’s relationship with personal loan origination platform Prosper, or the heavily tech-invested Cross River Bank into startups like GreenSky Credit and Marlette show how these relationships can develop into long-term symbiotic collaborations.

Other partnerships, like the one forged between Crestmark Bank and Credibly shortly after the fintech’s launch in 2010, serve as vital benchmarks for how successful financial technology companies can be fostered, despite a dearth of oversight in the digital lending space.

Credibly’s success is in part due to its institutional focus on risk management and culture of compliance, fostered by its early relationship with Crestmark. According to Bumbales, it’s because of this relationship that Credibly’s loan loss rates have remained significantly lower than the business lending industry average, despite lending to clientele with a generally lower FICO.

During that partnership, Crestmark itself was able to expand through acquisitions in New York as well as establishing offices in California. The bank was acquired by MetaBank in 2018 and maintains offices in five different states.

Crestmark’s regulatory and compliance expertise eventually allowed Credibly to offer that same degree of success in loan origination and servicing to other financial institutions, even permitting them the servicing rights to another fintech lender’s $250 million portfolio.

Twin Fates

As a greater number of fintech companies establish similar reliability, community banks are quickly tapping fintech servicers through the use of APIs or referral programs. In a 2018 survey of the American Bankers Association member banks’ outlook on fintech integration, more than 50 percent of the 193 respondents expressed interest in exploring referral model relationships in all aspects of commercial and personal loans, including mortgage lending, small business lending and consumer lending.

And, while the total number of banks are still clearly in decline, the prevalence of bank branches has remained fairly steady. While there is no telling how consumer demand will shape this trend in the future, it’s clear that community banks and fintechs are, for the foreseeable future, inexorably linked in a battle to serve clients overlooked by the financial giants.

Image Credit: Rocco S Cetera via Wikimedia Commons

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.