By Shira Gonen

Jefferies analysts weighed in on pharma giant Gilead Sciences, Inc. GILD and oncology research firm CytRx Corporation CYTR in light of patent litigation with Merck and 4Q:15 earnings, respectively.

Gilead Sciences, Inc.

Jefferies analyst Brian Abrahams weighed in on pharma giant Gilead following court events from its patent infringement litigation with rival Merck, where the latter is suing Gilead for illegal use of its ‘499 and ‘712 patents to manufacture sofosbuvir, the active ingredient in its Hep C treatments Sovaldi and Harvoni. Merck is seeking damages from Gilead in the form of royalties from the sales of the two drugs. Abrahams states that "both sides showed strengths and weaknesses" following court events that discussed the validity of Merck's patents.

After Gilead presented its evidence, three expert witnesses explained whether or not MRK patents "had adequate written description to show that a skilled expert would understand what the invention encompassed and how to use it." The descriptions favored Gilead, as the witnesses "provided convincing arguments" that the patents were not descriptive enough, lacking necessary data and "that one would not know how to use the invention without excessive experimentation." However, the analyst states, "Upon cross-examination by MRK, in our view, arguments that the patents would be interpreted as not useful did not seem as strong — this is important, because claims 9-11 of the ‘712 patent are much narrower, and may be harder to invalidate."

The analyst also comments on Gilead's argument that Merck stole the patents from biopharma company Pharmasset. According to the analyst, it is "less likely" MRK stole its patents as it "appears to have invented the class of compounds many years prior to Pharmasset, the compounds were encompassed by the MRK patents, and Pharmasset was well aware of these patents and used them in their inventions, licensing activities, and grant applications." As a result, Abrahams questions whether Gilead can "meet the high burden-of-proof to show MRK derived the invention from Pharmasset."

The analyst also states, "GILD did not present evidence at the trial that the MRK patents do not disclose how to make the invention, which MRK was planning to include as a major part of their testimony. GILD could have done this for a variety of reasons (want jury to focus on other arguments, limited time, or evidence not strong), and they will now rely more on lack of written description/how-to-use arguments."

The two parties are expected to give closing arguments on Wednesday, with a jury decision expected on Friday regarding the patent validity. The analyst notes that if one of Merck's claims is valid, "the case moves forward to damages determinations, but we won't know if these damages will be awarded until after the bench trial, where GILD has a second chance to render the MRK patents invalid or unenforceable." However, if all claims are invalid, the case will be dismissed and MRK will not receive royalties from GILD. The analyst also point to the unlikely scenario where MRK will file a judgement as a matter of law, where the judge will make a ruling without jury deliberation, as they are only 20% successful.

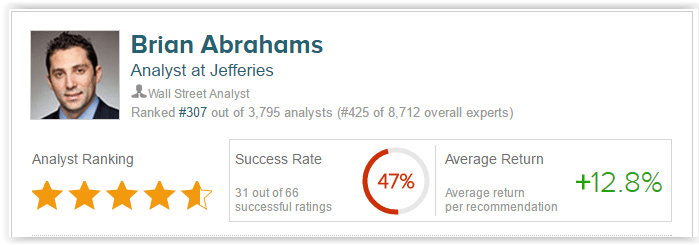

The analyst reiterates his hold rating and $100 price target pending results from the trial. Brian Abrahams has a 47% success rate recommending stocks with a 12.8% return per recommendation.

According to TipRanks, out of the 18 analysts who have rated Gilead in the last 3 months, 15 are bullish and 3 remain on the sidelines. The average 12-month price target for the stock is $116.87, marking a 28% upside from current levels.

CytRx Corporation

Analyst Chris Howerton of Jefferies weighed in on CytRx after the company released 4Q:15 earnings. The company reported a wider than expected net losses of ($58.6M), compared to estimates of ($50M) and a loss of ($0.97) per share, compared to estimates of ($0.78) per share. Despite weaker than expected earnings, the analyst though believes expected pipeline results and a commercial launch of a drug will represent catalysts for the stock.

Howerton states that "2016 will likely be a transformational year for CYTR: the critical ph 3 topline results for Aldox in 2nd-line STS is exp. in 2Q16 & incremental updates for DK049 could happen throughout the year (IND exp YE16). Of note, CYTR secured up to $40M in debt financing which mgmt expects to fund Aldox launch under supervision of new CCO."

The analyst reiterates a Buy rating though his lowers his price target from $3.00 to $2.50 due to interest expense associated the loan facility used to launch Aldox and his adjusted OPEX estimates. Chris Howerton has a 56% success rate recommending stocks with an average loss of (6.8%) per recommendation. According to TipRanks, only Howerton rated the stock in the last 3 months.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.