Macau gaming continues to struggle, as rising staff cuts and negative operating leverage numbers continue to tarnish investor appetites toward the region.

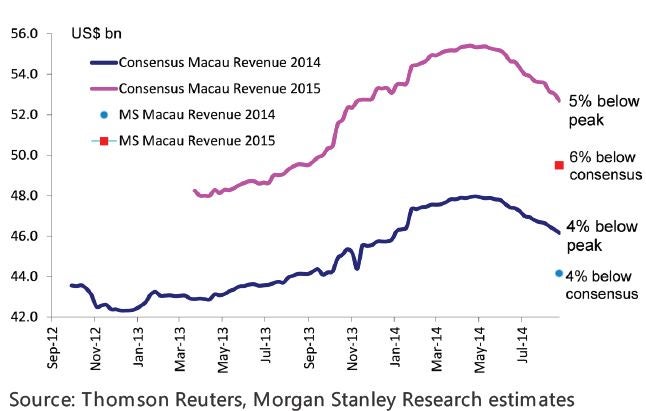

Morgan Stanley opined in a note Tuesday morning that Macau’s Gross Gaming Revenue (GGR) growth for 2014 has been cut from +12 percent to +6 percent. The expected pressure on revenue growth caused Morgan Stanley to upgrade Melco Entertainment MPEL from Equal-weight to Overweight. The bank also downgraded Sands China from Overweight to Equal-weight.

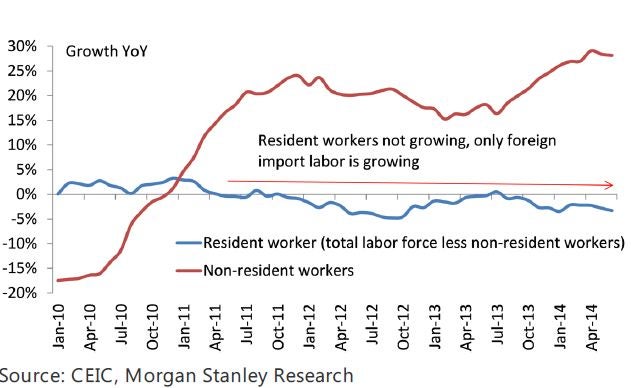

The staff cuts haven't helped expand per table revenues and the local workforce has remained flat as non-resident imported laborers grew materially since July 2013.

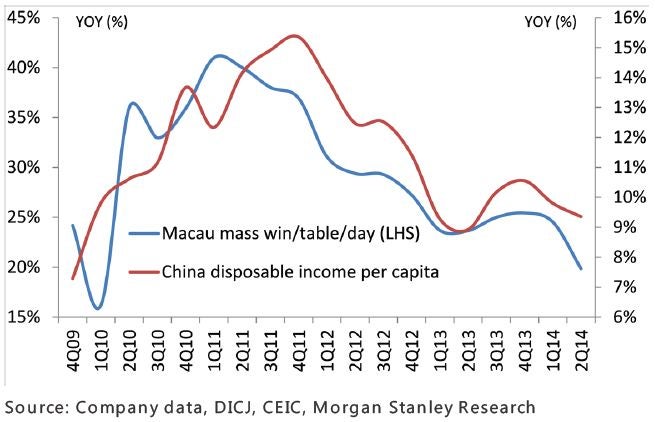

The slippage to China's disposable income fell alongside Macau's mass win per table per day. Mass table growth expanded 12 percent year over year in Q1 2014 and then four percent year over year in Q2 2014. Morgan Stanley sees growth remaining subdued in the low single-digit range, further dampening expectations of a growth rebound.

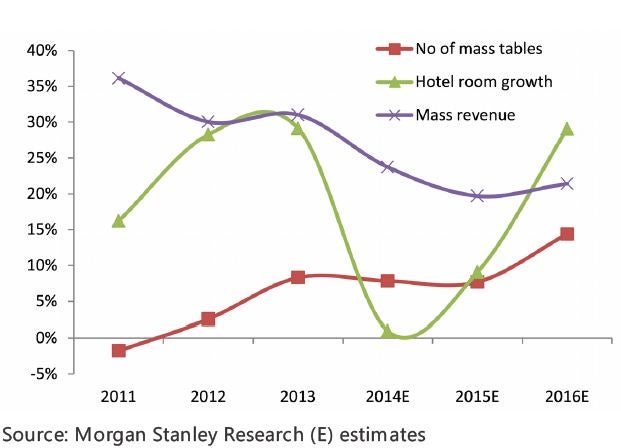

The standout for casino revenue growth has been the rebound in Hotel Room Growth:

The gaming industry labor force is becoming more aware of its standing also. Casino employees "have frequently protested against casino operators for more wage increases and benefits, having become more aware of their rights and in view of huge profits reported by the casino companies." noted Morgan Stanley.

Efforts by casino to retain talent have increased staff costs by 10-15 percent year over year. Staff costs alone are taking up 50 percent of fixed operating costs as of 2013.

Macau casino operators are in trouble, as no new casinos have been added in 2014, resulting in expectations that hiring will become difficult in 2015 as all casinos hunt for talent and use employment "sweeteners" to attract said talent which will eat further into margins.

Weakness in hiring and margin sustainability in light of increased tourism (+7 percent year over year according to MacauBusiness.com) gives analysts hope that Macau revenue growth will return in Q3 2014.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.