Carvana CVNA has seen its stock rebound over 400% from the March lows benefiting from the transition to everything online due to COVID19.

Carvana’s business model is fundamentally similar to its larger competitors such as CarMax, Inc KMX and AutoNation, Inc AN; purchase vehicles at auctions or as trade-ins, recondition them and re-sell them to customers while also offering financing options. As most auto retailers do, used cars are available online for viewing but Carvana claims a key competitive advantage of its business model is the centralization of the vehicle inventory pool in low-cost locations, hence reducing fixed costs and giving customers a larger selection of cars. Carvana prides itself on offering a great customer experience and then by shipping the vehicles to customers, trading fixed costs for variable costs. As a side note, Carvana also sells cars in giant vending machines, which appears to be more of a marketing gimmick rather than a strategic or financial advantage.

Carvana has been growing very fast since its IPO and revenue has now exceeded $1B for 3 consecutive quarters. At first glance, Carvana appears to sell comparable vehicles for about $1,000 less than its competitors; providing a very compelling value proposition to customers. As Carvana has yet produced a single profitable quarter since IPO, it remains unclear if Carvana has a structural advantage to enable such pricing differentiation or not.

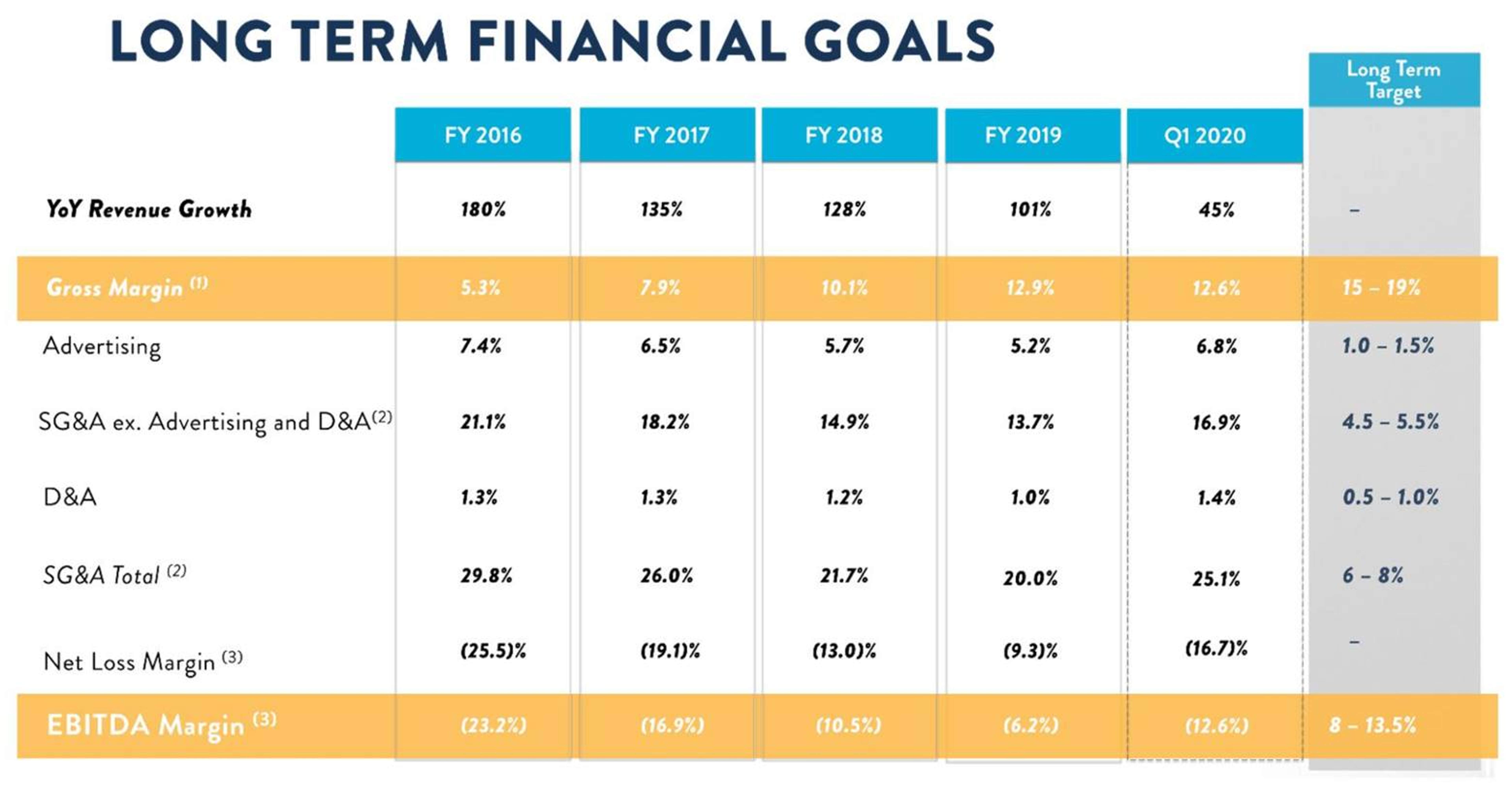

In Q1 2019, Carvana car sales have grown over 43% over the previous period demonstrating strong top-line performance. Carvana has outlined some aspirational goals for its bottom line with a goal to reach 8-13.5% EBITDA margin. To do so, they will need to reduce SG&A by over 17% as shown below from Q1, 2020 levels.

The benefit of scaling a business normally results in operating leverage as revenue growth outpaces fixed costs. In order to reach these EBIDTA levels, Carvana will need to turn around some very concerning trends in their business model, specifically as it related to the number of vehicles sold vs the investment required to sell each additional car.

As shown below Advertising costs are growing rapidly, now exceeding $1,400 per car sold from $1,000 one year ago. Carvana is investing aggressively to promote its brand, reach customers and enter new markets. Carvana already covers 68.7% of the US population and entering more markets will come with diminishing returns. Carvana needs to bring advertising costs down by 75% to achieve its EBIDTA target of 1% to 1.5% as outlined above. So either Carvana needs to reduce its spend, or quadruple the revenue while keeping advertising stable.

As Carvana centralizes its vehicle inventory, its fixed cost should be going down with the number of vehicles sold. However, this is also not the case. In fact, occupancy costs are increasing. The good news is that at $150 per vehicle, these costs are relatively low compared to traditional retailers.

Logistics costs have been trending in the right direction since Q1, 2019 but have reversed course in Q4, as Carvana is trying to reach customers further away from its re-conditioning centers and likely because of an uptick in customer returns.

Finally, Carvana accounts for the balance if its SG&A in a final category, which they classify as Others. This category also includes many functions such as general administrative, IT expenses, corporate occupancy, professional services and insurance, limited warranty, and title and registration. These costs should be trending down with more cars sold but keeps increasing, reaching $1,700 per vehicle sold in Q1, 2020.

Carvana is also being dragged down by other expenses, such as increasing interest expenses on its credit lines as well as the interest payments on the convertible debt they have issued. The overall effect is that the more vehicles they sell the more cash they burn per vehicle as seen below. At a $3,500 loss per vehicle sold in Q1 2020 amounts to a cash burn of approximately $185M per quarter.

Carvana has about $1 billion in liquidities but is burning cash at an increasingly rapid pace (because vehicle count is going up and so is the loss per car). Their business model appears to be broken, they are unable to leverage scale to increase operational efficiencies. Unless they make dramatic changes, they are at the mercy of new investments in order to continue funding their top-line growth. If they start cutting back their costs such as advertising or increase vehicle pricing to improve the bottom line, it is very likely they will kill their top-line growth and risk being re-valued similarly to other used car retailers. With falling used car prices combined with jobs losses in its target customer base, Carvana is reaching a tipping point.

Because of the scale they have already achieved, burning $200 million per quarter will not be sustainable for long, and the appetite of new investors to add more fuel to the fire may be limited.

The author has no position in Carvana

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.