This article was originally published on iREIT Investor.

In my upcoming book, Trump: It’s All Business, I examine the amazing world of Donald Trump and the mysteries behind his global real estate empire. As I explain in the book’s introduction, my research related to Trump’s vast holdings has taken me to many places across the globe and the journey has been surreal.

I liken the adventure to my favorite childhood book, Willy Wonka and the Chocolate Factory. If you can imagine, I am Charlie Bucket, the poor boy who delivers newspapers (I’m not rich and I write for Seeking Alpha and Forbes) and Trump is Wonka, the illuminating confectionist who takes pride in his unusual candy craftsmanship – it’s all about perfection.

At any rate, my book serves like a guide through the luxurious land of Trump-dom, as told by yours truly – the boy with the golden ticket.

In Willy Wonka-land you may recall the Oompa-Loompas, these unique characters played by dwarfs in the 1971 film. The complexities with the Oompa-Loompas are part of the mystery inside the Chocolate Factory and while the mischievous midgets are funny, they are also serious, that makes them strange creatures that always keep you second guessing.

We also find the same strange creatures in REIT-dom, these are the more complex REITs that offer a seemingly intricate investment strategy differentiated by there not so common product offerings. Due to these complexities, Mr. Market is often confused as these misunderstood alternatives appear riskier due to the disconnection that makes them complex.

Complexity Risk In REIT-Dom

Perhaps driven by this low interest environment, it appears that REITs have responded to Oompa-Loompa pitch by engineering more complex alternatives.

These alternative new REIT products are designed to allow investors access to different types of asset sectors (energy, wind, cell, transmission, etc…) in an envelope that was previously only available to professional investors.

The backbone – or meat and potatoes – for the REIT world was once core driven sectors like office, industrial, and retail. However, the new REIT-dom consists of a growing variety of sub-sectors that offer just about everything but the kitchen sink.

At some point there could even be a kitchen sink REIT. I’m just joking but the real estate test has become less difficult to prove and that’s why we now have REITs like Hannon Armstrong that owns thermostats and pump systems.

I never imagined that I would be researching natural gas lines, cell towers, billboards, transmission lines, prisons, casinos, solar panels, or racking systems. However, the REIT universe is growing steadily and as long as the demand is there, the new Oompa-Loompa’s should follow.

Today I’m going to provide you with a list of more complex REITs, not just one’s that are misunderstood due to their sector orientation, but instead a list of companies that appear to be viewed as complex in the eyes of Mr. Market.

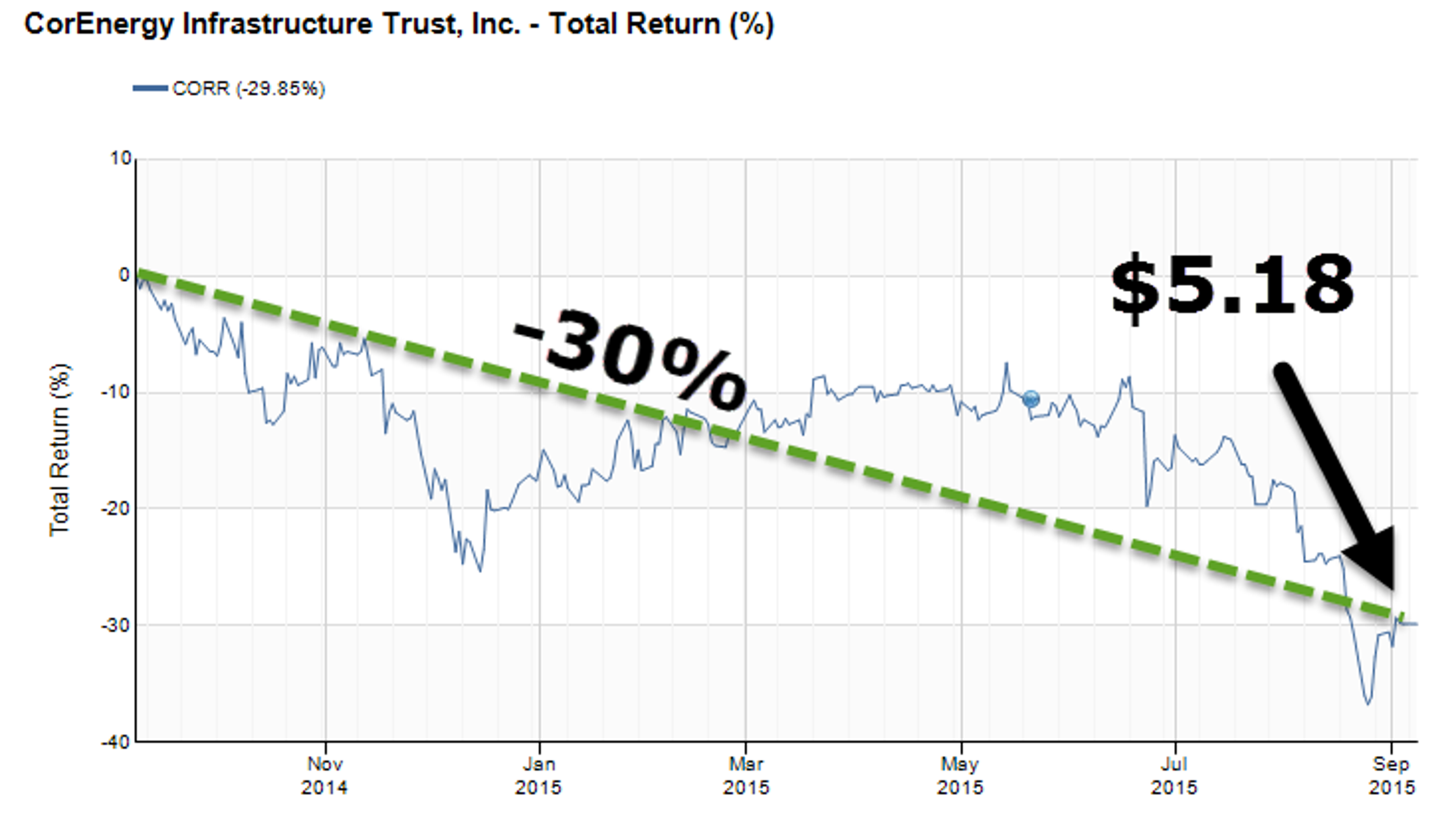

Take for example, Corenergy Infrastructure Trust Inc (NYSE: CORR). I recently wrote on this Infrastructure REIT that is now trading at a discount. Much of CORR’s cheap valuation has to do with its limited diversification, but the complex products are also misunderstood making it difficult for the average REIT investor to evaluate the risks. By restructuring as a REIT (CORR was previously a BDC) the company started acquiring real property (to qualify as a REIT) while still focusing on energy infrastructure.

Although CORR does not have a private ruling letter from the IRS (a moderate risk) the company does have a legal opinion, and the energy infrastructure sector is comparable to other real estate asset classes (cash flow is a high component of total return).

The common misconception is that CORR is an MLP; however the company is simply a landlord that primarily owns midstream and downstream U.S. energy infrastructure assets subject to long-term triple net participating leases with energy companies. As a consequence, Mr. Market views the energy-like security as an MLP.

The rationale is understandable since the businesses are similar; however, the differentiated investment thesis is clearly less understood by the market and that’s why the price behaves more like it’s an Oompa-Loompas. CORR is now trading at $5.18 per share with a P/FFO multiple of 7.1x. The 10.4 percent dividend yield is a clear sign that this Oompa-Loompa is quite unique.

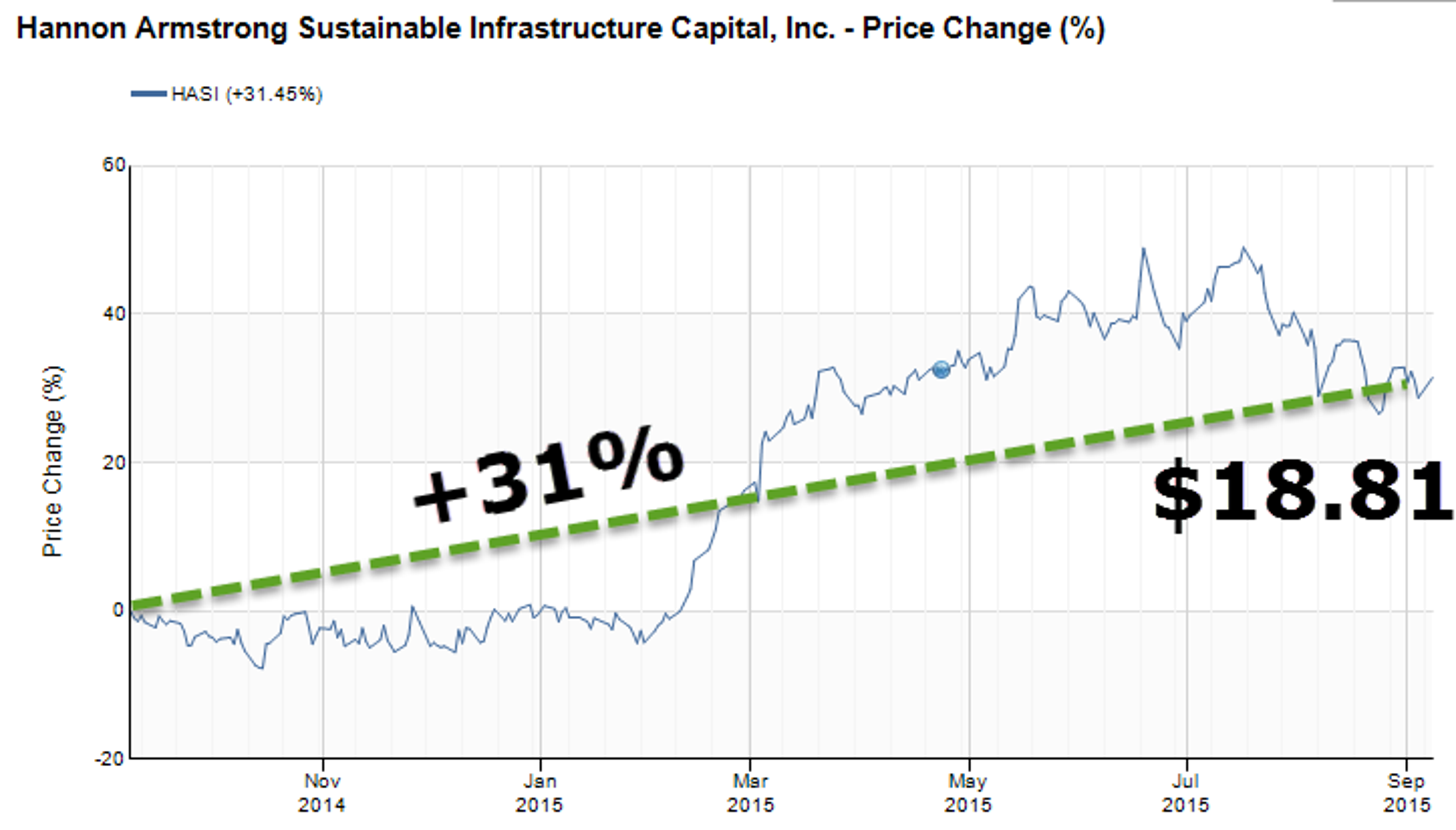

Another Oompa-Loompa that I have written frequently about is Hannon Armstrong Sustnbl Infrstr Cap Inc (NYSE: HASI). This clean energy REIT listed over two years ago (April 2013) after clarifying the definition of real property for REITs (REG – 150760 -13) in which the IRS provided defines what constitutes real property for REIT purposes.

What makes HASI unique is the fact that the company aggregates assets in multiple categories, all pertaining to clean energy real estate projects. For example, HASI invests around 53 percent of its capital in energy efficiency assets such as HVAC, Lighting, Controls, and Pumps.

Needless to say, these are all considered “real estate” assets as described and clarified in the above-referenced IRS ruling. HASI also targets wind (30 percent of revenue) and solar (17 percent of revenue).

Again, these are not the ordinary “meat and potatoes” that were on the REIT menu ten years ago, so the more complicated offering provides a higher degree of research and understanding.

Although HASI is a seemingly more complicated REIT model, Mr. Market has become more attracted to this Oompa-Loompa and especially the 14 percent dividend increase in 2014, a more predictable history (that suggests another wonka-boost in Q4-15) of growing core earnings generated by high-quality tenants (most are investment-grade). HASI is trading at $18.81 per share with a 5.5 percent dividend yield. Ironically, HASI has returned over 30 percent year-to-date- almost the exact opposite as CORR.

Most REITs subjected to complexity risks under-perform their Equity REIT peers.

HASI seems to be an outlier, other REITs that I consider to be trading at a complexity discount levels include Lexington Realty Trust Real Estate Trust (NYSE: LXP), Preferred Apartment Communities Inc. (NYSE: APTS) and Vornado Realty Trust (NYSE: VNO).

LXP and VNO have been working to become simpler enterprises by reducing non-core properties (and that’s a catalyst and reason I own LXP) and APTS has a unique investment strategy that combines multi-family with a sprinkling of shopping centers (and another reason I see the disconnect as attractive). Nonetheless, they are viewed as more complex Oompa-Loompas and it requires a higher-degree of research to evaluate these non “pure-play” alternatives.

Later this week I will be writing on the “ultra” Oompa Loompa’s in REIT-dom, Mortgage REITs. Needless to say, you should always weigh the complexity attributes when thinking about investing in order to determine the alpha being generated, that is, the price you are paying for the return you are receiving. Better said, “is the thrill of victory worth the agony of defeat?”

I own shares in CORR, APTS, and LXP.

Sources: SNL Financial.

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals, and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.