(Thursday Market Open) The Bank of England (BoE) raised its key lending rate by 50 basis points, its biggest hike in 27 years.

Potential Market Movers

The BoE, unlike the Federal Reserve, is expressing strong concerns about a potential recession. It also emphasized that it could be battling inflation for some time. In reaction to the news, the British pound strengthened against the U.S. dollar in the spot market and the London FTSE 100 was up 0.56% before the U.S. markets opened.

U.S. investors are trying to make sense of the weekly EIA inventories report that showed an unexpected increase in crude oil and gasoline. While the news is helping push oil and gas prices lower, this new reading on lack of demand raises concerns over the strength of the U.S. economy as consumers appear to be staying closer to home.

Adding to the economic picture, initial jobless claims came in a little higher than expected at 260,000, just above the forecasted 259,000. The Challenger Job Cut report showed that layoffs have increased 36.3% year-over-year but at a lower rate than the previous month. Additionally, The Wall Street Journal reported that retail giant Walmart WMT would be cutting 200 corporate jobs across various departments. All of this news is ahead of tomorrow’s biggest job numbers in July’s Employment Situation report.

While they wait, investors have a slew of earnings announcement to sift through from after last night’s close and before today’s opening bell. All stock movements here reflect premarket trading:

- Albemarle ALB rose 6% after the lithium miner soundly beat its earnings estimates and increased its forward earnings guidance.

- Booking BKNG reported better-than-expected earnings despite missing on revenue, but the stock fell 3% on a weaker third quarter outlook.

- Clorox CLX dropped 6.1% after missing on earnings and revenues estimates and issuing weaker-than-expected earnings guidance.

- ConocoPhillips COP beat on earnings estimates after earning $5 billion for the quarter, doubling its earnings from the previous year. COP rose 3.21%.

- Cigna CI topped earnings and revenue estimates and increased its 2022 earnings outlook prompting the stock to rise 3.66%.

- Eli Lilly LLY fell 4% after missing on top- and bottom-line estimates and cutting its earnings forecast.

- Paramount Global PARA fell 3.55% despite beating on earnings and revenue estimates but reporting weaker-than-expected streaming subscriptions.

- Toyota TM beat on top- and bottom-line estimates but fell 3% as the company reported supply chain problems and appeared to rely on the strong dollar as a boost for earnings.

Outside of earnings news, EV car maker Lucid LCID fell more than 12% in premarket action after announcing that it expects to ship 6,000 to 7,000 vehicles in 2022, well below its May guidance of 12,000 to 14,000.

Reviewing the Market Minutes

The S&P 500® index (SPX) made a run at its May highs yesterday but failed to break through despite jumping 1.56%. The Nasdaq ($COMP) was able to close above its February and March lows on a rally of 2.59%. The Dow Jones Industrial Average ($DJI) also gained 1.29% to trade near its May highs.

Despite the major indexes testing old highs and lows, the Cboe Market Volatility Index (VIX) fell below 22 for the first time since April. Investors appeared to ignore hawkish comments from St. Louis Fed President James Bullard earlier in the day and felt some relief in falling oil prices as well as China’s relatively uneventful reaction to Speaker Nancy Pelosi’s visit to Taiwan.

According to Briefing.com, the breadth of the rally was mixed with advancers outpacing decliners at a ratio of 11-to-5 on the NYSE and the Nasdaq, but trading volume wasn’t particularly heavy.

Stocks rallied in 10 of the 11 market sectors, led by technology and consumer discretionary. Energy was the only sector to close in the red.

The bulls were also helped by a positive ISM Non-Manufacturing Index report, which surged in July at 56.7, well above the forecasted 53.8 and higher than June’s 55.3 reading. This is a good sign for the service sector of the U.S. economy. The expansion in this sector of the economy is good for those concerned about recession, but it doesn’t necessarily play into the narrative that the Fed will be pivoting from rate hikes to cuts very soon.

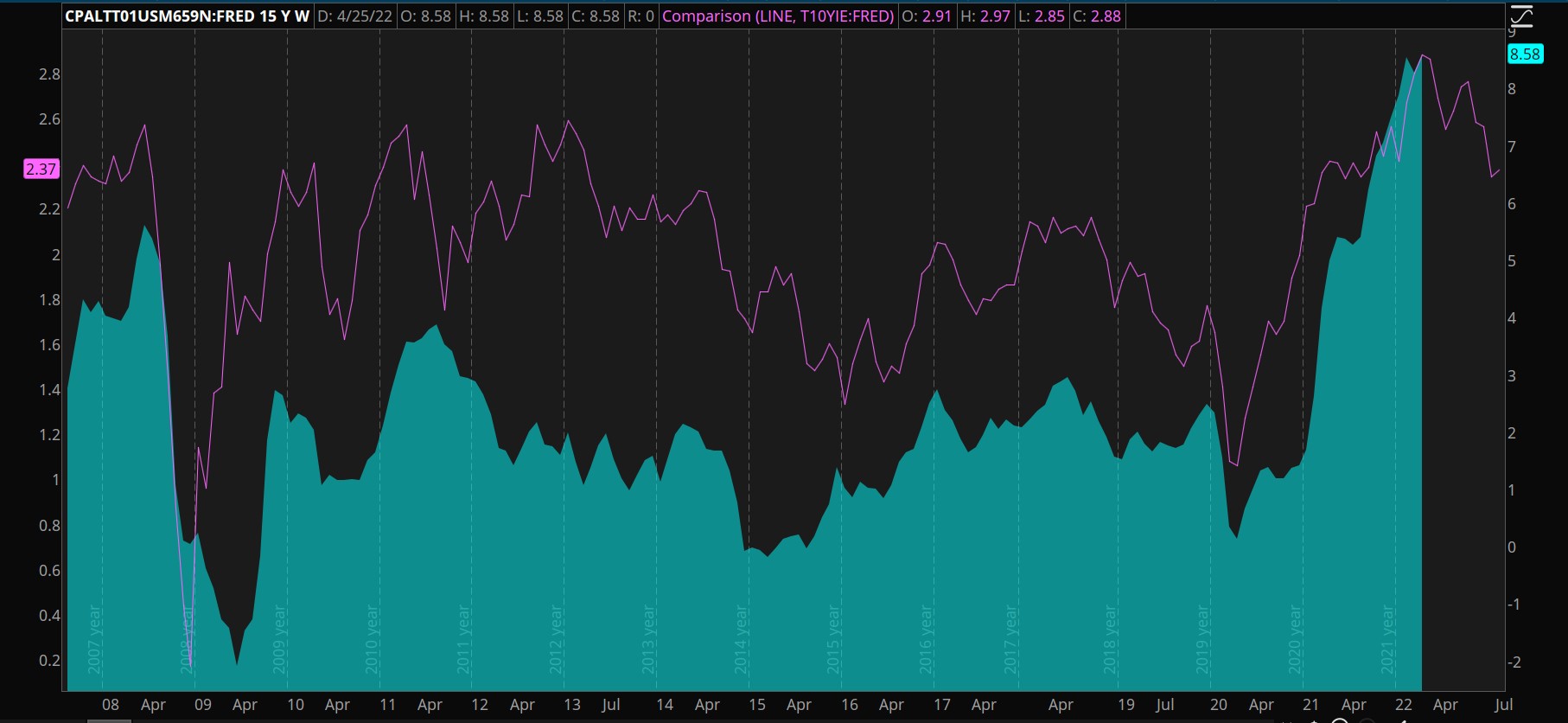

CHART OF THE DAY: MEETING EXPECTATIONS. The 10-Year Breakeven Inflation Rate (T10YIE:FRED—pink) compares the 10-year Treasury yield to the TIPS Yield to calculate the market’s expected inflation rate. When compared to the Consumer Price Index (CPALTT01USM659N:FRED—blue), investors can see the market is anticipating the CPI’s year-over-year inflation to fall to 2.3% in the next few months. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

OIL SLIPS: The WTI crude futures broke below support around the $95 level on Wednesday after settling 3.6% lower to $90.91 per barrel. The break, if sustained, is likely to be good news for the rate of inflation going forward. However, natural gas futures surged about 7.5% on the day and heating oil futures held its own level of support after closing 1.15% higher. Natural gas and heating oil are much smaller sectors of the energy complex than crude, so they are likely to be overshadowed on the inflation numbers.

The futures market could be reflecting the potential changes in supply and demand for energy products. The peak travel season for North America is starting to wind down as school starts up in many states toward the end of August. Additionally, European Union nations are starting to cut their use of Russian natural gas this month, which may result in higher demand for U.S. natural gas and heating oil as these nations look to meet their energy needs as cooler weather arrives.

Heating oil is a refined version of crude oil, so it does tend to rise and fall with crude prices. While the changing seasons should increase demand for heating oil, demand-driven price increases could be offset if crude continues to slide.

BELOW AVERAGE: Analysts are considering recent changes in gross domestic product (GDP)as they readjust their Q3 earnings estimates. According to FactSet, the aggregated Q3 earnings per share for S&P 500 companies decreased by 2.5% from June 30 to July 28. It’s common for analysts to make these adjustments the first month of the quarter. The average decrease over the past five years was 1.3%, 1.8% for 10 years, 2.1% for 15 years, and 1.7% for 20 years.

Looking at the earnings adjustments by sector, communications saw the largest declines, followed by materials and consumer staples. Energy and utilities were the only sectors to see an increase.

FORECLOSURE FRENZY? On July 30, MarketWatch reported a ‘dramatic increase’ in foreclosure filings. According to ATTOM Data Solutions’ midyear 2022 U.S. foreclosure market report, first public foreclosure notices are up 219% from the beginning of the year. Additionally, the number of foreclosure filings were up 153% year over year.

While the numbers look bad in the context of the negative housing market reports that came out in July and the increase in provisional loan losses (for all loans, not just mortgages) by banks this earnings season, previous foreclosure prints were at historical lows. So, what we could be seeing here is a simple reversion to the average.

Notable Calendar Items

Aug 5: Employment Situation Report and earnings from EOG Resources EOG, DraftKings DKNG, and Norwegian Cruise Line NCLH

Aug 8: Earnings from Dominion Energy D, AIG AIG, BioNTech BNTX, Tyson Foods TSN, and Principal Financial PFG

Aug 9: Earnings from Emerson EMR, Sysco SYY, Roblox RBLX, Coinbase COIN, and Hyatt H

Aug 10: Consumer Price Index (CPI) and earnings from Walt Disney DIS, and Honda Motors HMC

Aug 11: Producer Price Index (PPI) and earnings from Brookfield BAM, Illumina ILMN, Rivian RIVN, and Cardinal Health CAH

Image sourced from Shutterstock

TD Ameritrade® commentary for educational purposes only. Member SIPC.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.