This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

(Thursday Market Open) The bulls were looking to make a run overnight, but the stampede appears to have slowed down or gotten lost before the opening bell. However, investors appear to have interest in mega-cap stocks. Otherwise, they may just be waiting for the next round of earnings.

Potential Market Movers

The selling over the last two days may have been overdone because few stocks appear to be bouncing back in pre-market trading. Once again, investors appear to be focusing on the mega-caps stocks like Apple AAPL, Meta FB and Amazon AMZN because they were getting a bid before the open. Equity index futures started higher but have bounced around as the morning matured.

Hopefully, there’s still an appetite for equities and investors will return to the “buy the dip” attitude they’ve exhibited the last few years. But a slight uptick in the Cboe Market Volatility Index (VIX) seems to point to some uncertainty.

You can see where TD Ameritrade clients are putting their money with my latest edition of the Investors Movement Index ® (IMXSM). Overall, our clients reduced their exposure to equities in March which caused the IMX to move lower. Clients were net buyers in consumer discretionary, financials, and industrials and net sellers in energy, information technology, and materials.

Overall, clients appeared to be looking for safety; they were net buyers of fixed income as well as mega-cap stocks like Apple AAPL, Meta FB, Alphabet GOOGL and Microsoft MSFT. The purchasing of large- and mega-cap stocks is common during market downswings as investors tend to have a so-called “flight to quality.”

While the influx of earnings will start next week, two noteworthy consumer staples companies announced earnings before the opening bell. First, Constellation Brands STZ reported lower-than-expected earnings despite higher-than-expected revenues. The international beverage and alcohol company still rallied 1.38% despite the earnings miss in premarket trading.

The other stock, ConAgra CAG, beat on earnings and revenue prompting a rally of 1.19% in pre-market trading. Unfortunately, the producer of brands like Duncan Hines, Healthy Choice, Hunt’s and more lost its gains as the stock sold off due to the company forecasting rising cost pressures.

Earlier in the week I warned we’ll likely see analysts adjusting earnings estimates ahead of earnings season. This morning, JPMorgan JPM analysts did just that, cutting their expectations on Apple. Look for more analysts to adjust their forecasts.

In other stock news, computer hardware company, HP HPQ, rallied more than 11% in pre-market trading on the news that Warren Buffett’s Berkshire Hathaway (BRK/A) has taken a $4.2 billion stake in the company. Berkshire must be in a buying mood; last month they revealed a stake in Occidental Petroleum OXY and plans to acquire Alleghany Y.

Reviewing the Market Minutes

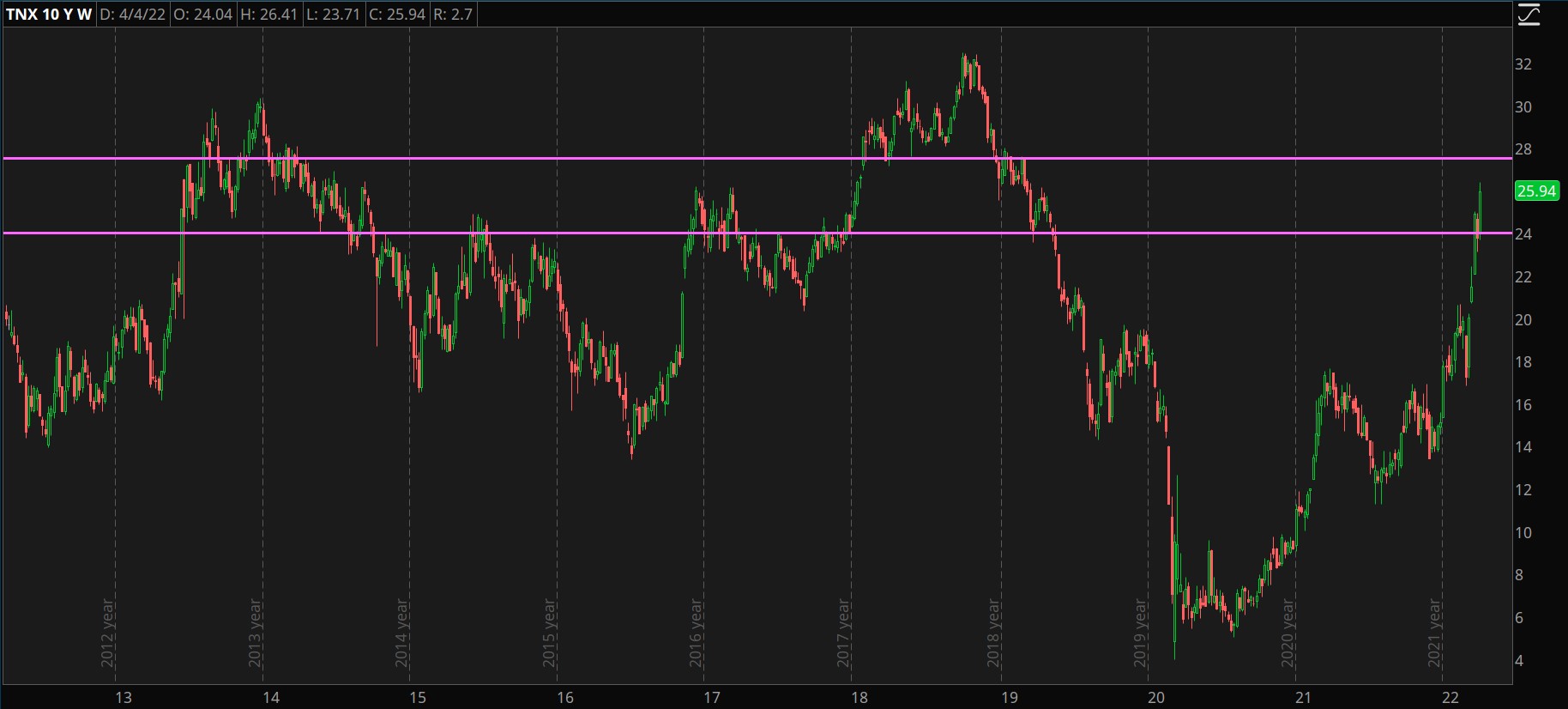

Wednesday began with a spike in interest rates and a drop in stocks as investors continued to react to Fed Governor Lael Brainard’s hawkish remarks Tuesday on the aggressive way she thinks the Fed should reduce its balance sheet. The 10-year Treasury yield (TNX) climbed to 2.641% but pulled off its highs to close around 2.6%.

Rising interest rates caused investors to rethink stock valuations once again, which hit growth and technology stocks the hardest. The Nasdaq Composite ($COMP) led the sell-off, falling 2.22%. The S&P 500 Pure Growth Index fell 1.64%, while the Technology Select Sector Index dropped 2.51%.

Stocks attempted to mount a comeback in the afternoon when it was hit with the FOMC Meeting Minutes. The minutes of the March Fed meeting revealed that the Fed plans to shrink its balance sheet of Treasuries and mortgage-backed securities by $95 billion per month, which will likely begin in May, split at around $60 billion in Treasuries and $35 billion in mortgage-backed securities. Additionally, the minutes indicated what the market had already guessed—the Fed is looking to raise the overnight rate by 50-basis points in May. In fact, the minutes revealed that the Fed was set to do a 50-basis-point hike in March but backed off because of the war in Ukraine. Judging from the minutes, it appears the doves have left the ark because most members are onboard for a more aggressive approach to battling inflation.

Oil prices helped the inflation situation because oil futures fell 4.89% on the day and closed well under $100 at $96.97 per barrel. Oil also passed below an important technical level by breaking its 50-day moving average, which could bring in a few more bears to add to the selling.

Falling oil prices could be good news for airlines, which have been devastated by higher fuel prices on top of COVID-19 restrictions. Speaking of airlines, JetBlue JBLU fell 7.7% on Wednesday after making a surprise all-cash offer of $3.6 billion offer for Spirit Airlines SAVE. Spirit appears to be stuck in a love triangle because it previously agreed to merge with Frontier Group ULCC for $2.9 billion in cash and stock. Despite the offer, Spirit fell 2.38% on the day.

CHART OF THE DAY: THE 10-YEAR OVER 10 YEARS. The 10-year Treasury yield (TNX—candlesticks) has broken a long-term resistance level and could rally as high as 2.8% if it rallies to the next resistance line. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

Timing the Curve: Last week, there was a bit of a kerfuffle over the yield curve inverting and rightly so. The yield curve when measured by the 2-year Treasury yield and the 10-year Treasury yield has been a reliable harbinger of a recession. The problem with the 2s10s ratio is that recessions have occurred within six to 24 months after the inversion. The large difference in time makes the signal unactionable for the majority of investors.

However, another popular spread is the 3-month Treasury yield versus the 10-year Treasury yield. When the curve inverts using these points, then a recession usually follows within a year’s time. The good news is that this ratio is positive and has actually steepened over the last year despite the 3-month Treasury yield rising at the fastest pace of any other yield on the curve and moving from 0.08% to 0.65% year to date.

Dimes and Dollars: Rising yields have helped strengthen the dollar, which has trended higher since January 2021 against a basket of other currencies in the U.S. Dollar Index. On Wednesday, the index created a new 52-week high for the second day in a row. Unfortunately, the strong dollar could be bad news for international companies because their goods and services are more expensive to foreign consumers.

As earnings season kicks off next week, look for currency risk to become a theme among international companies when providing forward guidance. With the Fed getting more hawkish, the dollar could continue to rise because higher yields will likely attract foreign investors looking to capitalize.

Banking On Hikes: The banking credit spread should be widening with rising yields and creating bigger provides for banks, but the PHLX KBW Bank Index (BKX) fell 1.36% on Wednesday adding to a six-day losing streak and is testing a yearlong support level. Now that the hawks pushed the doves out of the Eccles Building, some investors are concerned that the Fed is going to be too aggressive in attacking inflation and cause a recession. So, while the spread is increasing for banks, a recession would likely mean less borrowing.

Additionally, with the Fed looking to unload its balance sheet, it will be selling longer-term Treasuries out of its inventory, which will likely drive yields on the longer end of the curve higher. This could also make borrowing even more expensive.

This might seem like a lot of overthinking for a Fed that has just barely ended its bond-buying program and just raised its discount rate to 0.25%. Only time will tell if investors are playing chess or hatching conspiracy theories.

Notable Calendar Items

April 8: Wholesale Inventories, WASDE

April 12: Consumer Price Index (CPI), Albertsons ACI earnings, CarMax KMX earnings

April 13: Producer Price Index (PPI), JPMorgan JPM earnings, BlackRock BLK earnings, Delta Air Lines DAL

April 14: Retail Sales, UnitedHealth UNH, Wells Fargo WFC, Morgan Stanley MS, Goldman Sachs GS, Citigroup C

April 15: Markets closed for Good Friday

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Unsplash

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.