Round two of big bank earnings looked a lot like round one: A knockout. It’s nice to not only see good earnings, but optimistic views going forward, which is very important this particular reporting season.

Bank of America Corp BAC and Citigroup Inc C both easily topped analysts’ expectations with their Q1 results, and that’s not all. BlackRock, Inc. BLK and PepsiCo, Inc. PEP also had upbeat quarters. It’s extremely early, but investors seem to like what they’ve seen so far from reporting companies, and major indices took the high road in pre-market trading Thursday after a forgettable performance the day before.

There’s nothing forgettable about today’s surging retail sales and decreasing jobless claims. We’ll get to those a bit farther down.

More Banks, More Earnings Strength

Financials continued with really solid results and positive outlooks expressed in their calls this morning. We’re off to a good start in earnings.

Like other big banks reporting this week, BAC had a strong investment banking and trading quarter, with gains in both the equity and fixed income sides of the field. Earnings per share of $0.86 easily surpassed Wall Street analysts’ expectations for $0.66, and revenue of $22.9 billion topped the consensus view of $22.1 billion.

In the meantime, C posted profit of $7.94 billion, or $3.62 per share, topping analysts’ estimate of $2.57. Revenue of $19.3 billion came in above the Street consensus of $18.8 billion. In a repeat of yesterday’s action, C and BAC released billions of dollars from their loan loss reserves, the stash of cash they’d put aside last year for possible loan defaults from the Covid crisis. The release of these reserves is adding to banks’ Q1 profits, even though arguably that’s not organic growth.

Shares of both companies popped in pre-market trading, so maybe investors are prepared to reward them for their earnings beats, which isn’t always a given around bank reporting season. News of BAC planning a $25 billion buyback might be one thing supporting shares this morning. For C, the announcement that it would be streamlining its operations across Asia-Pacific and emerging markets—pulling out of 13 markets to concentrate on four larger Asian banking centers—seems to have drawn some applause in the premarket.

What people appear to like is that C is getting more focused. The Street likes when a company says, “Here’s what our goals are and we won’t try to be everything to everyone.”

That may be true for Citigroup, but retail sales this morning arguably did have something for everyone in the market—except bears. They jumped a huge 9.8% in March, so it looks like people are back out there shopping as the economy reopens. Keep an eye on consumer discretionary shares to see if they benefit from this data, which compared with analyst expectations of around 5%.

If things seem like they couldn’t get more positive this morning, get ready because they did. Initial weekly jobless claims of 576,000 were by far the lowest since Covid struck, down from 769,000 the previous week and expectations of 695,000. It’s just one week of data, but it is very encouraging and appears to show the recovery gaining steam.

Meanwhile, volatility keeps getting beaten up, with the Cboe Volatility Index (VIX) remaining below 17 this morning. It’s amazing how little volatility there is in these markets, though it makes some sense considering many stock indices are at all-time highs. Overall, as much as the hand-wringing goes on, the market is saying things look pretty good and now earnings are backing that up.

Bank Leaders Sound Optimistic

Of the three big banks that reported yesterday, Goldman Sachs Group Inc GS and Wells Fargo & Co WFC ended up with nice gains, but JP Morgan Chase & Co. JPM shares never got above the water line. Though earnings and revenue came in above expectations for all three, one impediment for JPM could have been that a decent portion of its earnings beat came from the company’s decision to pull back cash it had set aside for possible loan defaults. Not that it wouldn’t have beaten pretty handily even without any help, but maybe that took away some of the fizz.

WFC also benefited from pulling back loan reserves, but it was good to see the stock move solidly higher considering all the regulatory pressure they’ve been under the last few years. Investors seemed cheered by WFC’s earnings call, with the stock making more gains as the call took place. WFC executives sounded optimistic about both the consumer and corporate business outlooks, and that’s the bread and butter for WFC, considering they don’t have the same kind of exposure to Wall Street trading as many of the other big banks.

The executives at WFC weren’t the only bank leaders sounding optimistic about the economy yesterday. Same goes for JPM and GS, but that’s not too surprising considering all the positive remarks we’ve heard from industry leaders the last few weeks. If there’s something that might make people worry, it’s wondering how much the big banks can improve on Q1 numbers, especially when it comes to trading and investment banking. They’ve set a pretty high bar for themselves that’s going to mean some tough comparisons down the road.

Besides the banks and reopening sectors like Energy, entertainment, and hotels (which may have gotten some of their tailwind from the banks’ positive outlooks for the economy), there wasn’t really any driving force in the market yesterday. Earlier this week, big Tech had set the pace, but most of those stocks, including Monday and Tuesday stalwarts Tesla Inc TSLA and NVIDIA Corporation NVDA, couldn’t follow through Wednesday. That left kind of a leadership vacuum as the Nasdaq (COMP) tumbled about 1%, even though the Dow Jones Industrial Average ($DJI) and the Russell 2000 Index (RUT) both received some support from the Financial rally.

You can’t blame the 10-year Treasury yield for the poor Tech performance yesterday, with that closely watched metric staying near recent levels in the 1.63% range before dipping briefly below 1.6% this morning. That’s not a number that’s likely to scare anyone, but Tech weakness might have just reflected a bit of a swing back toward the “value” sectors after a strong start this week for Tech and other growth areas. The growth vs. value pendulum keeps swinging.

Gold continued to edge lower this week even though the dollar is also struggling, which is a bit of a head scratcher. Typically those two move in different directions. A weaker dollar, if that’s what we’re seeing here, could be bullish for stocks, especially multinationals that do a lot of their business overseas. However, it’s hard to see a lot of softness developing in the dollar if U.S. data and earnings keep looking solid.

On another note, yesterday saw Coinbase Global Inc COIN shares begin trading after their direct public offering (DPO) on Nasdaq. COIN operates an online exchange where buyers and sellers can meet to trade Bitcoin and other cryptocurrencies. The debut drew a lot of interest, and the company finished Wednesday with a valuation of around $86 billion. The exciting part about cryptocurrencies is watching over the next 10 to 20 years to see how they develop. There are still questions about ease of use and government regulations around these products, but for right now many investors are very excited about them.

Crude Comeback

If you’re looking for rallies, check what crude did yesterday. Remember, crude tends to get volatile around Tuesday and Wednesday every week when supply numbers come out. The U.S. price has been vacillating around the $60 per barrel mark for weeks, but seemed to break out of that Wednesday on a big draw of U.S. stockpiles, as my TD Ameritrade Network* colleague Kevin Hincks, Senior Equity Strategist, said yesterday. Now we’re clearly through $60, so we’ll see if that level continues to hold.

Crude prices now aren’t really at levels that would necessarily get anyone nervous about margins for transport companies, but any sign of a move up toward $70 might get people worried.

Today delivered a full plate of data, with more on the way tomorrow. That includes University of Michigan sentiment, where analysts see a consensus headline figure of 88.0, up from 84.9 last time out. Also keep an eye on housing starts and building permits for March. Both have leveled off recently after an amazing start to 2021. Tomorrow also brings earnings results from Morgan Stanley MS.

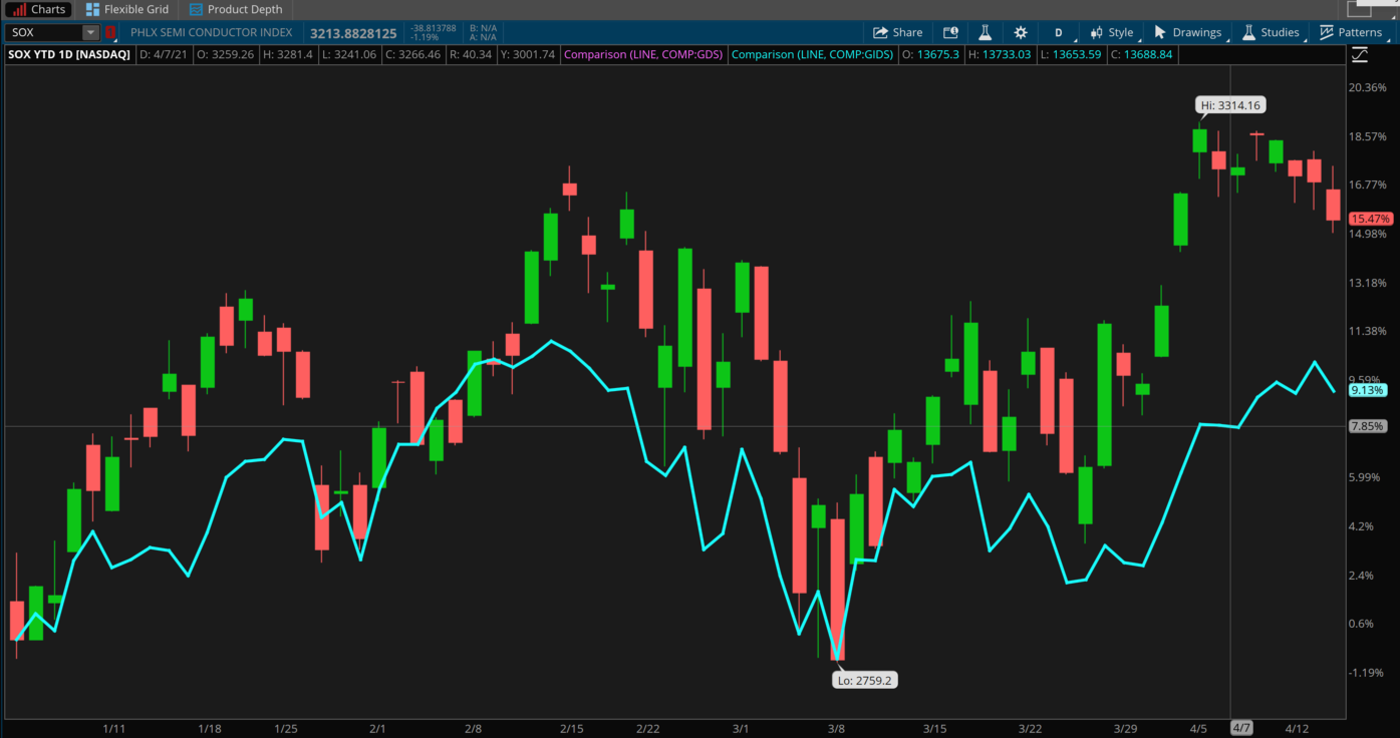

CHART OF THE DAY: SAME SECTOR, DIFFERENT STORY. Just to show that a sector doesn’t always trade in sync, here’s a three-month chart of the Philadelphia Semiconductor Index (SOX—candlestick) vs. the Nasdaq (COMO—blue line). Chip stocks recently came slightly off their highs, but remain near those peaks. The broader COMP, which is heavily tilted toward Tech, is up over the last few weeks but hasn’t made a new high since February. Data Source: Nasdaq. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Powell Talks Tactics: On the monetary front, it was interesting to hear Fed Chairman Jerome Powell yesterday hint that the Fed is likely to use the same playbook it followed coming out of the 2008 financial crisis, with tapering coming well before hiking rates. “We will reach the time at which we will taper asset purchases when we have made substantial further progress towards our goals from last December,” Powell said in comments to the Economic Club of Washington, Reuters reported. “That would in all likelihood be before, well before, the time we would consider raising interest rates.

Related content: Benzinga's Full Economic calendar

The Fed is under pressure to avoid sending the market into another “taper tantrum” like we had back in 2013 when it began trying to withdraw some of its support (it didn’t execute a rate hike until late 2015). Powell has said again and again he’d give the market plenty of warning before making any move to taper. However, even an early warning might cause turbulence. That being said, traders are seeing a greater chance of a rate hike before the end of this year— 18% as of this morning, up from about 8% yesterday and a mere 2% a month ago—according to the CME FedWatch tool. This is an emerging trend worth following, as the Fed has said in previous statements it plans to stand pat on rates for the foreseeable future. The next Federal Open Market Committee (FOMC) meeting is in less than two weeks.

Bumpy Landing: Airline Q1 earnings are expected to show more pressure, with analysts forecasting big losses for Delta Air Lines, Inc. DAL going into its earnings report this morning. United Airlines Holdings Inc UAL, American Airlines Group Inc AAL, Southwest Airlines Co LUV, and Alaska Air Group, Inc. ALK are all on the calendar next week, and Wall Street consensus shows all of them in the red on earnings per share and well below their Q1 2020 performance. None of which should come as a surprise to anyone, considering the passenger numbers last quarter were typically only around 40% of year-ago levels during what UAL called “the most disruptive crisis in aviation history.” When airlines report, keep an eye on how much cash they’re burning as the crisis continues, where they’ve been able to identify new possible ways to save money, and how passenger loads have looked. It also might be interesting to get feedback from the airlines on how things are going with Boeing Co’s BA 737-Max, now back in service for several months but recently in the news for more problems. Southwest has the most Max’s in service.

The bigger question for travel stocks, including airlines, this time around isn’t as much what happened last quarter, but what they think might happen this summer when hopefully vaccinations allow more people to return to normal life. Guidance is going to be the gorilla in the room for airlines, hotels, casinos and restaurants.

Sent to Bed Early: For a fresh example of how guidance can trip up a stock, check out Bed, Bath & Beyond Inc. BBBY yesterday. Most of the company’s quarterly metrics, including same-store sales, looked pretty solid, and earnings and revenue both beat analysts’ expectations. Digital sales rose an eye-popping 86%. BBBY even reaffirmed previous guidance for full-year sales of between $8 billion and $8.2 billion. Then the stock fell 9% once trading opened. Why? It might have been because the average analyst projection for revenue was $8.2 billion, and the company’s guidance showed it might not hit that level. Bang, zoom. There were other issues besides guidance that contributed to the stock’s plunge Wednesday, including questions about store closures and quarterly revenue not quite matching some analysts’ expectations. But don’t discount the role guidance can play.

What the market gives, it often takes away. And the takeaways often happen when investors have trouble picturing better future growth. On Wall Street, it’s not “what have you done for me lately?” It’s more like, “Thanks for all that nice stuff, but what about tomorrow? And the day after…” We might be in for more of this kind of action in Q1 earnings season than normal, simply because investors built so many positive hopes into stock prices. BBBY hasn’t performed well in recent years, but shares did rise from below $5 a year ago up to $30 before earnings. Not every company can say its stock is up six times in 12 months, but even for stocks that didn’t deliver that kind of punch, investors might be quick to find fault if earnings aren’t amazingly bright and shiny.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Austin Distel on Unsplash

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.