If investors judge the value of Apple Inc. AAPL on its stock movement alone, the Cupertino, California, juggernaut looks to be a clear winner, with shares having advanced over 65% since bottoming out in March.

But investors know a company with the size and market capitalization power of AAPL—tapping an astonishing $1.6 trillion as of July 24—has many arms that stretch in myriad ways through product upgrade and innovation to regulatory issues in the U.S. and abroad. That makes putting together a pre-earnings rundown for the consumer tech juggernaut a tough task.

It becomes even more difficult when considering the potential impact of a COVID-19 “second wave” that may or may not manifest itself in the fall. Many companies have pulled guidance altogether, while some have offered up “cautious” or “qualified” forecasts. AAPL, however, was among the first U.S. companies to warn of the potential impact of the coronavirus—even before it was labeled a pandemic—one that would likely smack sales and supply chains.

Considering AAPL’s global reach and close ties to the consumer market, when CEO Tim Cook steps to the microphone next week, his words will likely be of particular interest to analysts and investors.

The Apple Store Closing Index?

Having had experienced coronavirus-related disruptions in China, AAPL also was among the first major retailers to turn the lights off at its stores in early March, cautioning then that the far-reaching impact from China to the U.S. could prompt a global recession.

AAPL has been so precise in the timing of its closings, openings, and re-closings that the Wall Street Journal is likening Apple’s COVID-19 store strategy to the so-called “Waffle House Index,” the 24/7 breakfast food chain whose menus and store openings have become an informal guide to the severity of a natural disaster like a hurricane, tornado, or tropical storm.

That’s also helped the company get a better grasp on what earnings might look like ahead. When AAPL first offered Q2 guidance in conjunction with its earnings release, it flung a wide net of expected revenues from $63 billion to $67 billion. But by February, it knew even that range would not be met.

Remember this about AAPL, its earnings, its operations, and the worldwide pandemic: Not only does the tech giant lose sales and service revenue at stores when they’re closed, but economic woes, in general, tend to drag down sales—those iPhones and iPads are expensive. On the other side of the equation, AAPL’s supply chain got hammered too when much of the world shut down, pausing manufacturing of its products.

No Guidance + Store Closings = Uncertainty

For its fiscal Q2 results for the period ending March 31, AAPL posted a 1% gain in quarterly revenue, to $58.3 billion—well below that wide range and soft by most standards, as it reported mixed sales results in its largest product categories:

- iPhone – down 7.5% to $28.9 billion from $31 billion

- iPad – off 1% to $4.4 billion from $4.9 billion

- Mac lost 3% to $5.35 billion from $5.5 billion

- Wearables up 22% from $6.3 billion to $5.1 billion

- Services higher by 17% to $13.4 billion from $11.5 billion

AAPL Chief Executive Tim Cook said then the firm was taking “significant” steps to battle the sales drop offs but did not offer a forecast for the quarter, an uncharacteristic move that was prompted by, you guessed it, the cloud of uncertainty created by the pandemic.

It looks like the consumer tech giant might have been more prescient than initially thought. As already noted, AAPL was among the first retailers to shut down its U.S. stores in March, then reopen a number of them starting in late May and into June, only to have to switch the lights off again in a handful of them in Florida, California, and Texas.

Some analysts are expecting that AAPL might again decline to offer Q4 guidance, falling back on the ambiguity that the pandemic continues to create. But final numbers aside, many said they do want to know what the forecast is for the iPhone 12 models. Will they be available by September?

Analysts Said ...

Goldman Sachs Group Inc GS analysts led by Rod Hall said last week that the arrival of the iPhone 12 could be crucial to Q4’s bottom line. A one-month delay might lead to a 7% punch to revenues and a 6% pullback in earnings, fueling an already dire outlook.

By Goldman’s thinking, demand will continue to weaken through the end of the year and could lead to what would amount to an astonishing slide in profits that might fall 16% below Wall Street’s consensus.

“On this basis, we see Apple’s recent stock performance and absolute trading level as unsustainable and would continue to recommend that investors avoid the stock,” the research note said.

FIGURE 1: PRE-EARNINGS JITTERS? Since March Apple (AAPL—candlestick) has rallied along with the S&P 500 Index (SPX—purple line). In the last month AAPL slightly outperformed SPX although in the last few trading days the stock seems to have lost some of that edge. Data Sources: Nasdaq, S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

That’s harsh but keep this in mind: Though Goldman put a sell rating on the stock, it also raised its price target to $299 from $268. That’s where AAPL shares were trading back in May.

And, not every analyst thinks the same. Morgan Stanley (MS) analyst Katy Huberty said in her note to clients last week she believes AAPL will outpace Wall Street’s earnings outlook because of better-than-expected hardware sales as well as double-digit gains in services

“Investors are coming to realize that Apple may not be as dependent on significant iPhone cycles to sustain growth as they once thought, and that the ecosystem Apple has created is differentiated and worthy of a platform valuation multiple,” Huberty wrote.

Even still, she thinks the iPhone 12 will come out in October, admittedly later than the usual September rollout, but in time for the holiday gift-giving extravaganza. What’s more, she thinks consumers will glom on to them based on surveys she’s seen that suggest 34% of respondents plan to upgrade their smartphones within the next six months.

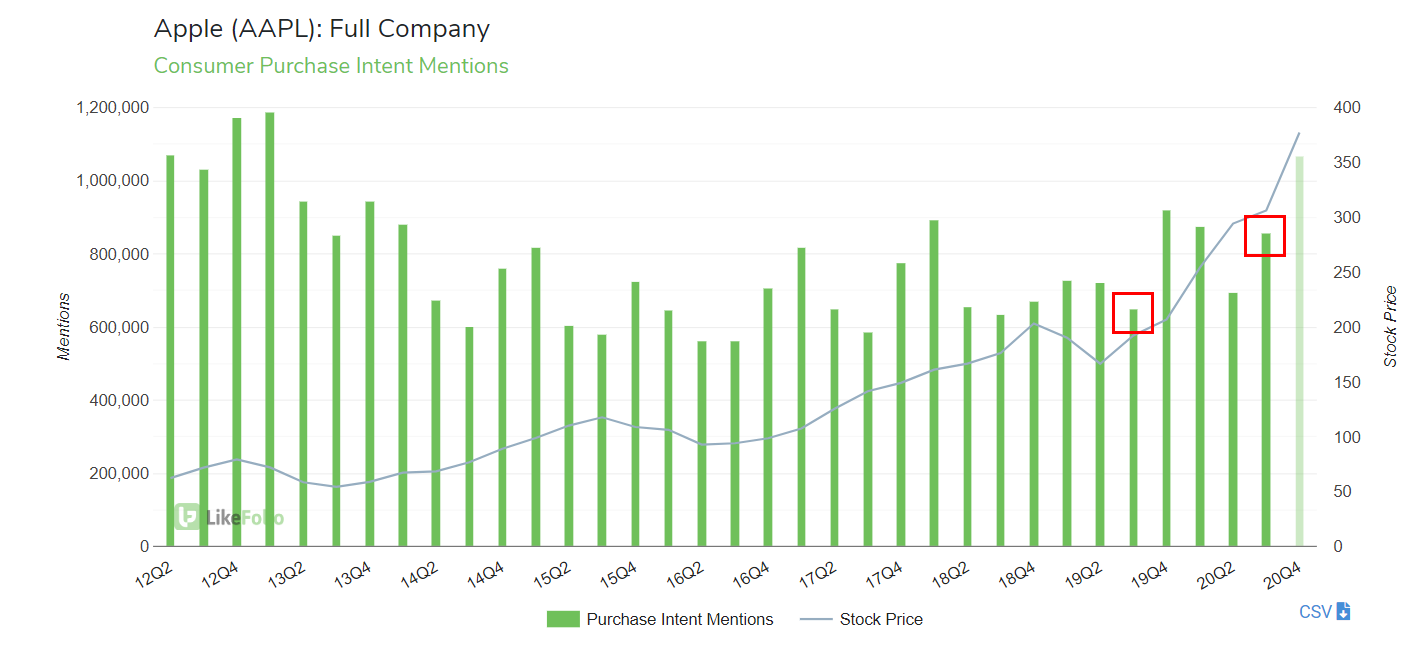

That pairs well with what LikeFolio, which tracks product mentions on social media, has been seeing. Consumer mentions of purchasing any AAPL product shot up 32% in Q3 compared with the year-ago mentions, according to its data. The Purchase Intent mentions for Q4 are the highest they’ve been since Q1 of 2013 (see figure 2). The 30-day moving average for purchase intent is in double-digit year-over-year growth for the iPad, up 50%; Mac higher by 47%, and iPhone gaining 19%, according to LikeFolio data.

FIGURE 2: GETTING SENTIMENTAL FOR AAPL? According to sentiment data from LikeFolio, Purchase Intent mentions for Q4 have been running at a multi-year high. Data source: LikeFolio. For illustrative purposes only. Past performance does not guarantee future results.

Who’s right and who’s wrong? Time will tell and this is always a good time to remind investors that past performance is no guarantee of future results.

Does Anyone Really Know About Apple Watch?

Speaking of wearables, AAPL Chief Financial Officer Luca Maestri offered a somewhat unexpected comment about Apple Watch on the Q2 earnings calls. It struck a chord because any kind of wearable device during a stay-at-home pandemic didn’t seem to be a natural fit. But Apple Watch might have been the exception.

“Apple Watch continues to expand its reach as over 75% of the customers purchasing Apple Watch around the world during the quarter were new to the product,” Maestri said on the call.

Did the addition of the Fitness app and the sleep catcher drum up interest? Like Huberty, some analysts believe wearables and services could be big growth drivers for AAPL. Listen in to hear if Maestri makes similar comments on this week’s call.

Before all is said and done with AAPL, some analysts have worried if all the regulatory clouds hanging over AAPL—and other like tech players—could impact bottom-line dollars if fines are imposed or services are pulled.

Cook and Co. aren’t likely going to be able to address those concerns, but it doesn’t hurt to ask. Stay tuned.

Apple Earnings And Options Activity

When Apple reports earnings Thursday afternoon, it’s expected to report adjusted EPS of $2.04, vs. $2.18 in the prior-year quarter, according to third-party consensus analyst estimates. EPS estimates seem to vary widely among analysts, with a reported range between $1.55 and $2.47.

Revenue is projected at $51.75 billion, down 3.8% from a year ago.

The options market has priced in an expected share price move of 4.3% in either direction around the earnings release, according to the Market Maker Move™ indicator on the thinkorswim® platform.

Looking at the July 31 weekly expiration, put volume has been heaviest at the 360 and 350 strikes, but more activity has been seen to the upside, particularly at the 390 and 400 call strikes. The implied volatility sits at the 23rd percentile as of Monday morning.

TD Ameritrade® commentary for educational purposes only. Member SIPC. Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options.

Photo by Medhat Dawoud on Unsplash

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.