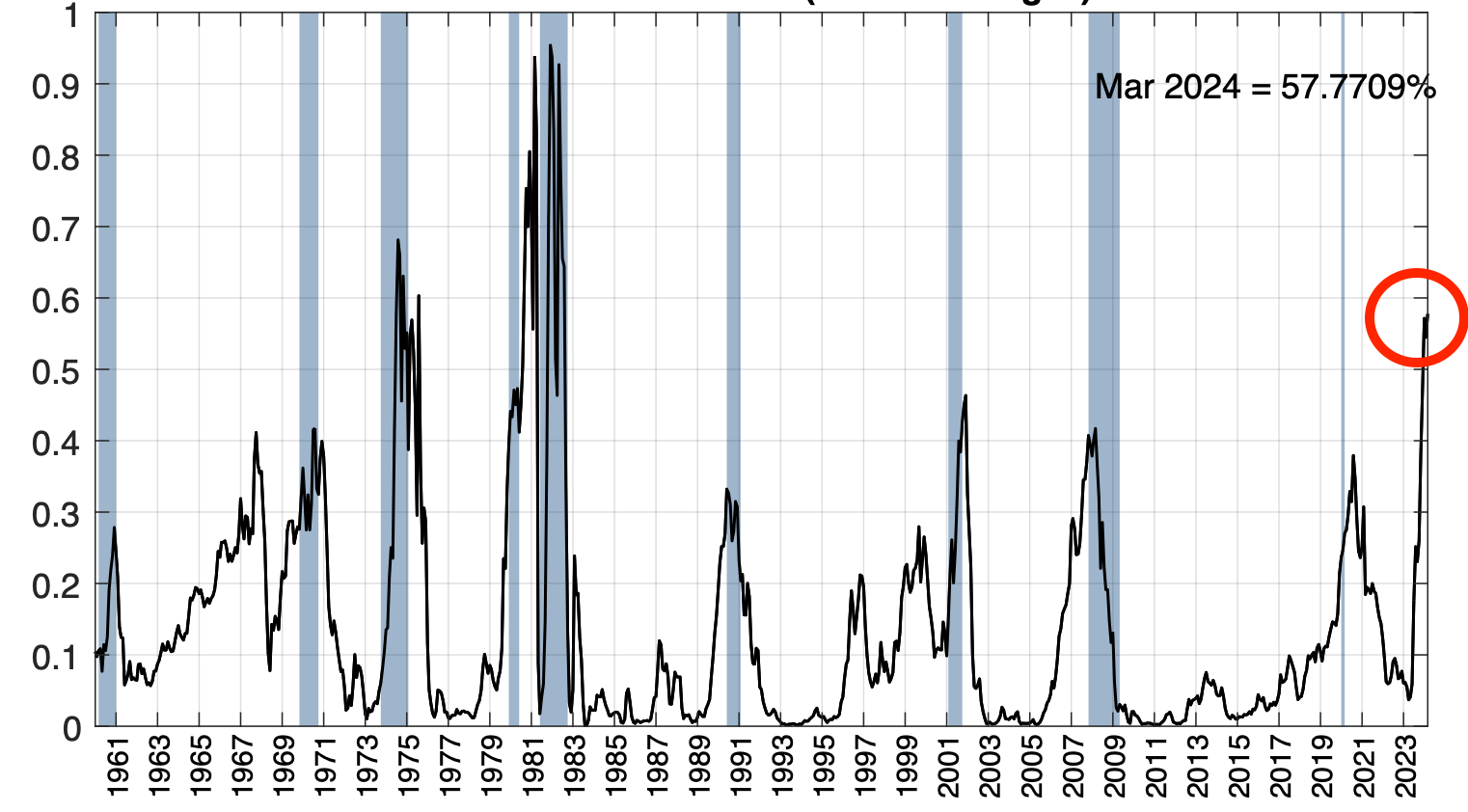

The likelihood of a recession in the United States within the next year has risen to almost 58%, the highest level since August 1982, according to the New York Federal Reserve.

The recession-risk indicator is now greater than it was in November 2007, just before the subprime-Lehman crisis, when it stood at 40%, and December 2001, when it was at 46%.

Chart: Probability of U.S. Recession Twelve Month Ahead

Source: Federal Reserve Bank of New York

Read Also: Economist Lists 3 Recession Red Flags Investors Should Be Watching In 2023

The Bond Yield Curve Slope As Recession Predictor

The New York Federal Reserve's model uses the yield curve's slope, or "term spread," to predict a U.S. recession twelve months ahead. The term spread used by the New York Fed refers to the gap in yields between the 10-year Treasury bond and the 3-month bill.

When yields on shorter-term bonds are higher than yields on longer-term bonds, the yield curve is considered inverted.

An inverted yield curve has reliably predicted each of the previous eight U.S. recessions since 1970.

Chart: Treasury Yield Curve Slope 10y Bond Yield Minus 3-Month Bill Yield; Shaded Areas Indicate U.S. Recessions Source: Federal Reserve Bank of New York

Source: Federal Reserve Bank of New York

Why Does an Inverted Yield Curve Indicate a Recession?

When a yield curve is inverted, investors fear that the current high level of interest rates, reflected in elevated shorter-term yields, will push the economy into a recession, causing the central bank to cut interest rates in the future, thus discounting presently lower longer-term yields. This is why an inverted yield curve is often a precursor to a recession.

The SPDR Bloomberg 1-3 Month T-Bill ETF BIL, is a popular ETF which offers exposure to the ultrashort end of the Treasury curve, investing in zero coupon U.S. T-Bills with less than three months until maturity.

The iShares 7-10 Year Treasury Bond ETF IEF, instead offers exposure to Treasury bonds with seven to 10 years to maturity.

Treasury Yield Curve Inversion: Where Are We Now?

In March, the term spread was negative 1.15%, as 10-year rates were around 3.5% and 3-month yields were around 4.65%. The 10-year-3-month yield differential has further worsened to a negative 1.6% at the time of writing, with the 3-month yield jumping to 5.2% and the 10-year yield trading at 3.6%.

If such a spread holds or expands further in April, then the next month's New York Fed recession probability indicator will likely become even more negative than its previous assessment of a 57.8% chance of a recession occurring before March 2024.

Now Read: BofA Fund Manager Survey: Investors Underweight In Stocks Reaches 2009 Crisis Levels

Photo: Shutterstock

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.