The Office of the Comptroller of the Currency released the Q1 2016 report on Bank Trading & Derivative Activities yesterday. The report highlights the boost banks saw in Q1 on their trading desks. According to OCC, Q1 saw bank trading revenues increased 35.3 percent MoM primarily driven by " increase in both combined interest rate and foreign exchange revenue, and credit revenue."

The derivatives market continues to expand as a notional $12 trillion was added to the total US Commercial Bank derivatives accounts, primarily in the form of interest rate notionals, bringing the current level to $192.9 trillion.

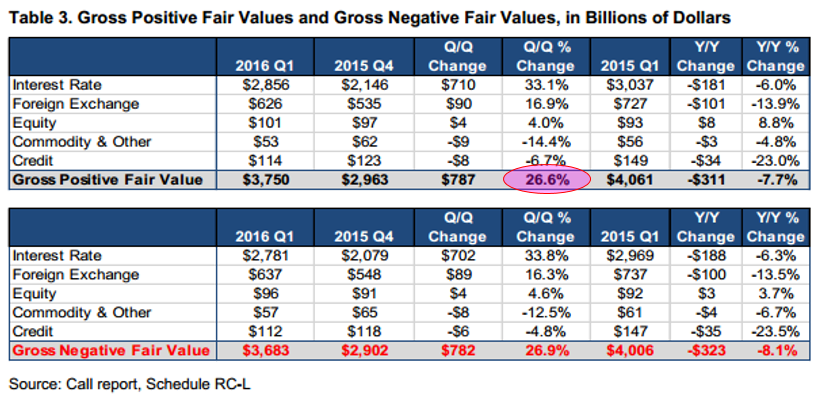

When it comes to the greatest financial innovation ever, Credit, the OCC tells us gross positive fair value (GPFV) rose 26.6 percent in Q1, reaching $3.8 trillion which was mostly comprised of 29.9 percent increase in receivables from interest rate & FX contracts.

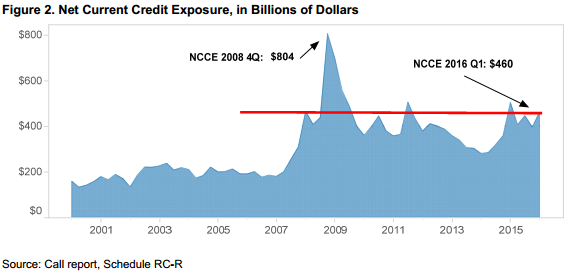

"The significant decline in NCCE since 2008 has largely resulted from declines in the GPFV of interest rate and credit contracts. GPFV from interest rate contracts has fallen from $5.1 trillion at the end of 2008 to $2.9 trillionat the end of the first quarter of 2016. On March 31, 2016, exposure from credit contracts of$114.4 billion was $1.0 trillion lower (89.8 percent) than the $1.1 trillion on December 31, 2008. New regulations and a decrease in client demand have led to the reduction in credit derivative notional amounts."

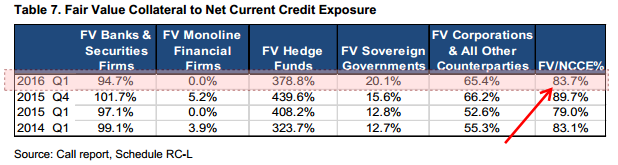

"Reporting banks held collateral against 83.7 percent of their total NCCE at the end of the firstquarter of 2016, down from 89.7 percent in the fourth quarter of 2015. The reduction in the ratio of collateral held against counterparty exposure was due primarily toweaker collateral coverage of exposures to banks and securities firms, which decreased from101.7 percent to 94.7 percent. Collateral held against hedge fund exposures decreased in the firstquarter, but coverage remains very high at 378.8 percent. Hedge fund exposures have always been secured well, because banks take “initial margin” on transactions with hedge funds, inaddition to fully securing any current credit exposure. Collateral coverage of corporate,monoline, and sovereign exposures is much less than coverage of financial institutions and hedgefunds, although coverage of corporate exposures has been increasing over the past several yearsbecause of increases in the volume of trades cleared at central counterparties."

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.