The prospect of saving for retirement can seem like slaying an almighty dragon. If you’re still in your 20s, you may not have even begun to think about saving for the ripe old age of 66 (the “full retirement” age if you were born between the years of 1943 and 1954).

However, the earlier you begin to think about saving for retirement, the better—and no matter what your age, you can benefit from learning more about how to tackle the “saving for retirement” beast. Are you going to lean into Social Security? Do you have a workplace retirement plan? Have you invested in insurance products? Take a look at the investment strategy options that you might have.

Quick Look at the Best Retirement Accounts:

- 401(k) or 403(b)

- Traditional and Roth IRAs

- SEP IRA

- Health Savings Accounts (HSA)

What to Consider When Choosing How Much to Invest

Before you choose a retirement account type, you need to decide how much you will contribute. At the same time, you need to weigh several factors when making these choices. Yes, you need a steady retirement income, but you also need to invest in retirement so that you can make the most of this money.

Times can change, and you must learn to be flexible with your retirement account and your funds. Retirement investing involves a few factors that you should consider, including your retirement plan and:

1. Your Age

The earlier you start saving for retirement, the more money you will have when you decide to stop working and enjoy your golden years. This is thanks to a principle known as compound interest or interest accrued on the interest that you’ve earned previously. A 25-year-old who puts $3,000 into an investment account that returns 7% each year (a conservative estimate, as the American stock market has traditionally returned more than 10% annually) each year for 10 years will have more than $338,000 when he retires, even if he doesn’t contribute another dime ever again after he turns 35.

That can make up a considerable nest egg for some people. At the same time, your investment strategy can yield more. You might also add retirement funds, cash out of a retirement system or participate into a retirement/pension fund.

On the other hand, a 35-year-old who saves $3,000 annually for retirement will have invested $90,000 of his own money by the time he turns 65, and will only be left with about $303,000. Younger investors have the power of time on their side—older investors need to play catch-up and contribute more money annually if they want to retire at the full retirement age. A retiree gets to make this choice for themselves, but they must balance that with the retirement income that’s required.

2. Your Income Level

Ideally, you should aim to save a percentage of your income for retirement rather than a set dollar amount. Some employers offer a 401(k) match program where they will contribute an equal amount to your retirement fund as you do monthly, up to a certain percentage, essentially giving you free money for retirement. Try to contribute your employer’s highest percentage of matching or max out your contributions annually (more on that later) for the most robust retirement account. You may also need help with investment management, and an investment advisor or tips from Benzinga could be a great help.

3. Your Emergency Fund

From a broken leg to an unexpected layoff at work to a sudden auto breakdown, life in unexpected. If you are unprepared for a financial emergency, you’ll have to take out loans to cover necessary expenses, which can lead to a years-long struggle with debt. Before you even think about saving for retirement, build up a $1,000 emergency fund that cannot be spent except in dire circumstances.

Remember, an emergency can interrupt your retirement journey, and you don’t want to dig out cash from your retirement portfolio or investment fund. Keep a considerable insurance portfolio on hand.

After that, you can start contributing to your retirement account—but you should still work to save up enough cash to cover about 6 months’ worth of expenses in your emergency fund. This is just one part of your savings plan because you want to use something like a retirement calculator to learn more about your needs and continue to save further to reach your retirement goals.

4. Jobs and Passion Projects

When you retire, you may choose to work part-time to keep your mind in the game. Some people take on passion projects, and others have specific things they’ve always wanted to do. You must weigh the difference between how much money you’ll make from part-time work with the passion projects you with to take on. There’s nothing wrong with remaining active in retirement, but you need to make sure the numbers work out. But also remember that these will be cash investments because you are now on a fixed income.

Choose the Types of Retirement Accounts You Want to Use

There isn't just one way to save for retirement. You can use any of the methods below or combine them to hit your saving and investing goals.

1. 401(k) or 403(b)

A 401(k) account or a 403(b) account is the easiest way for most people to save for retirement. You can authorize your employer to take a certain percentage of your paycheck each period and contribute it to a sponsored retirement account.

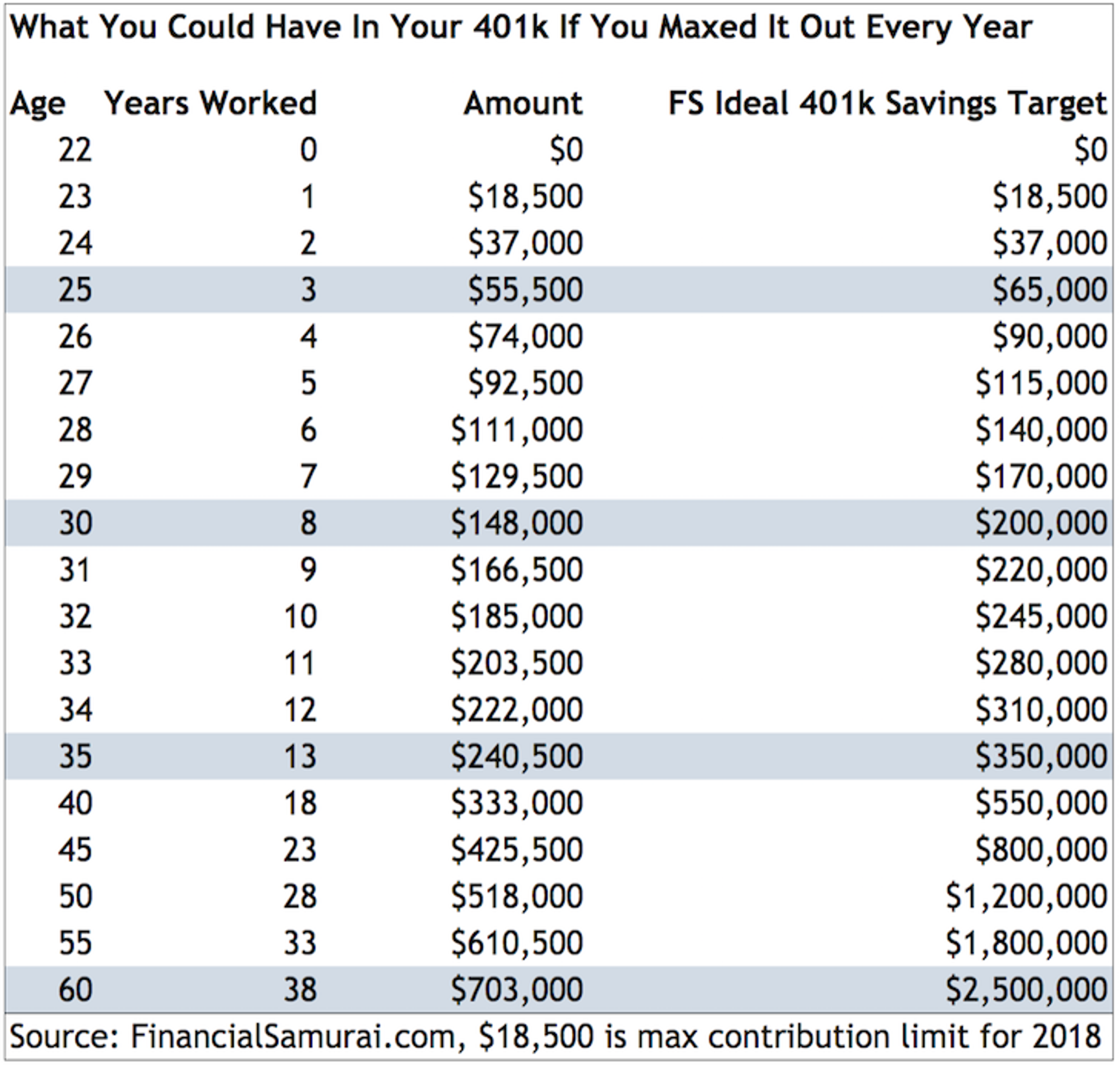

Beginning in 2018, you can contribute up to $18,500 of your pretax income annually to your 401(k) account if you are under the age of 50, and $24,000 if you’re over the age of 50.

2. Traditional and Roth IRAs

An Individual Retirement Account (IRA) is a type of supplemental retirement savings account that many individuals have in addition to their 401(k) or 403(b) accounts. If you have a traditional IRA, you do not have to pay taxes on your contributions, but you will have to pay up when you withdraw the money.

A Roth IRA is the opposite—you pay tax on your contributions when you make them, but you can withdraw the money tax-free during retirement. For most individuals, Roth IRAs are a better option because they allow your money to accrue interest without getting bogged down by taxes. IRA contribution limits are stricter than employer-sponsored plans; you can contribute only $5,500 a year to an IRA or $6,500 if you’re over 50 years of age. Limitations on Roth IRAs are also placed on individuals who make more than $116,000 annually and couples filing jointly who earn more than $183,000.

You can use IRAs to invest in a range of assets, including:

- ETFs

- Consumer defensive stocks

- Blue chip stocks

- Energy stocks

- Precious metals

Interested in opening an account? Here are some of Benzinga's favorite IRA brokers.

3. SEP IRA

If you are self-employed or you own a small business, you have the option of opening a simplified employee pension (SEP) IRA. A SEP IRA functions almost identically to traditional IRA with increased contribution limits. You can contribute either 25% of your annual income or $55,000 in 2018—whichever amount is lower.

These accounts are easier to set up than solo 401(k) accounts, so most self-employed individuals use a SEP IRA as their primary retirement savings vehicle.

4. Health Savings Account (HSA)

If you have a health insurance plan with a high deductible, you may be eligible to invest in a health savings account (HSA). You can save up to $6,850 in an HSA if you’re under the age of 55, and the money that you contribute is tax-exempt. You can also withdraw money from your HSA to pay for almost any medical expense that you could incur, including everything from co-pays to prescription medication to emergency room visits.

If you don’t spend the money that you’ve contributed, it rolls over indefinitely. Once you turn 65, you are free to withdraw the money you’ve saved for any reason but be aware that you’ll be subject to a hefty 20% fee if you withdraw money for anything besides medical expenses. You will also have to pay income taxes when you withdraw, even if you’re over the age of 65. But, this could be a good idea for you if you wish to continue working or carry the account long into the future.

Final Thoughts

Saving for retirement may seem impossible, but the truth is that all it takes to see massive returns is regular small contributions. A monthly contribution of just over $450 a month (less than what most people pay in rent) is enough to max out a traditional or Roth IRA. You can maximize the value of your retirement account by placing your money into a diverse array of stocks and bonds.

Frequently Asked Questions

Do you need $1 million to retire?

The amount of money everyone needs to retire differs based on their earnings, obligations and financial situation, along with their retirement plans.

Should you open a business in retirement?

Managing a business in retirement can be exciting for many people, but you should plan carefully for succession and management of the business so that you can enjoy your retirement.

About Sarah Horvath

Sarah is an expert in the insurance, investing for retirement and cryptocurrency space.