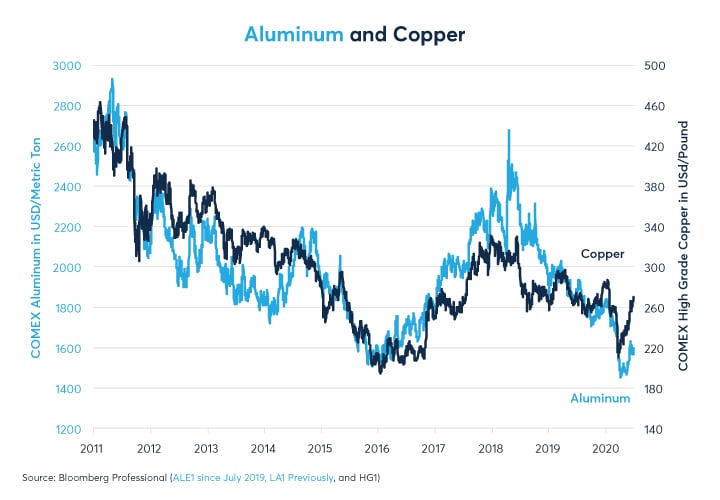

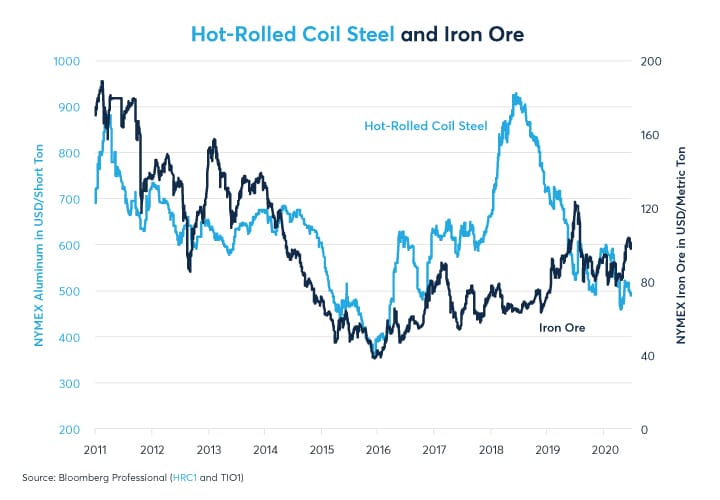

In the face of a deep, global economic contraction in the first half of 2020, prices of industrial metals have been remarkably resilient. Copper has rebounded to pre-pandemic levels at the start of the year, and while aluminium prices are lower than at the start of 2020, they are well off their recent lows (Figure 1). Iron ore prices, too, are higher so far this year but steel has fallen significantly (Figure 2).

Figure 1: Copper Prices Have Rebounded To Early 2020 Prices While Aluminium Is Off Its Lows

Figure 2: Iron Ore Prices Are Higher So Far In 2020, While Steel Prices Have Fallen

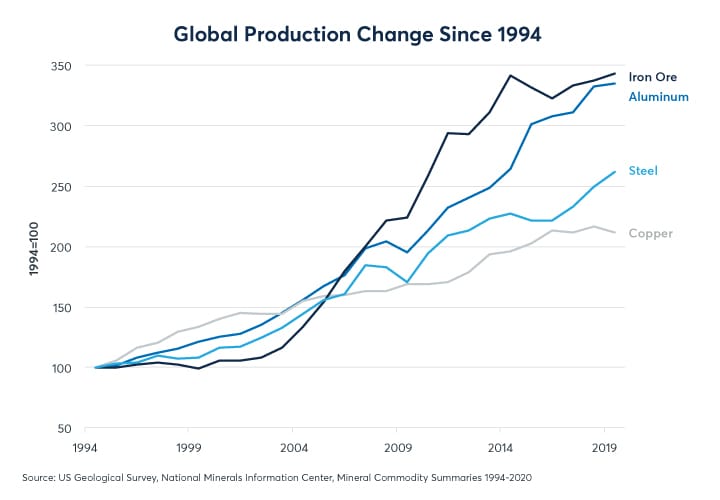

The resilience of most industrial metals is somewhat surprising considering how supply has grown in recent decades. Compared to the 1990s, the world is awash in industrial metals. Over the past quarter-century, the annual output from copper mines has increased by 112%. Steel production is up 162%. Aluminium and iron ore mining supply have increased by 235% and 243%, respectively since 1994 (Figure 3). Given the sharp decline in economic activity, one might have expected industrial metals prices to fall substantially as a result of the pandemic. So, what has been supporting prices?

Figure 3: A World Awash In Metals

The impact of reduced global demand is being partially offset by a coronavirus-related supply shock across the metals sector. In South Africa, the world’s deepest gold mine was shut in March after 170 workers tested positive for COVID-19. Similarly, copper mines were shut in Peru and Zambia in March and April for the same reason. A large Chilean copper mine at Chuquicamata halted production in June when Brazil’s largest iron ore miner suspended 10% of its production amid a coronavirus outbreak at one of its mines. Moreover, mining companies are putting off investment in new mining operations as global travel is dramatically curtailed, amid fears of fresh coronavirus outbreaks and a potentially slow recovery in global demand.

In essence, copper and other industrial metals are caught in a tug of war: coronavirus outbreaks threaten both demand and supply. If and when the pandemic fades, both demand and supply could rebound.

Demand Outlook

Industrial metals may also be vulnerable to developments in the building sector. If office construction slows significantly as a result of post-pandemic changes to work habits, that could put a bearish tilt on demand.

China is the single most important source of demand for industrial metals. It buys between 40% and 50% of the world’s raw aluminium, copper and steel while using nearly two-thirds of the world’s iron ore. These figures, however, exaggerate somewhat China’s role in these markets. While China buys a large share of raw materials, about one-third to half of its purchases are re-exported as components in intermediate or finished goods.

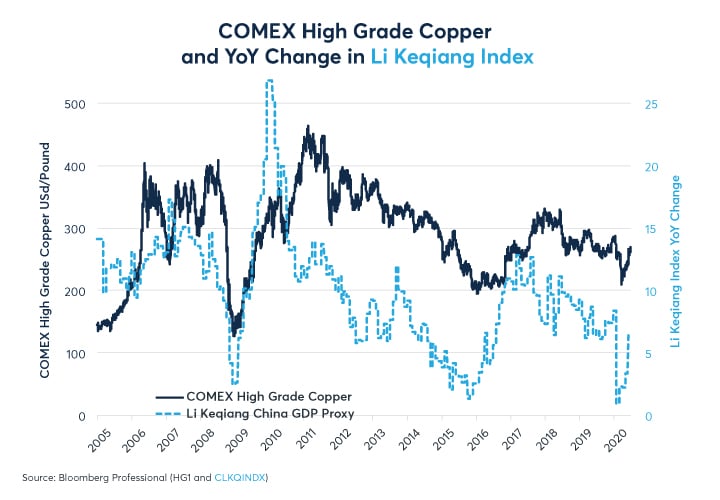

China reports its second-quarter GDP data on July 16. After the first quarter’s 6.8% contraction, the Q2 number is expected to be positive. Nearly all Chinese indicators show a rebound in activity during the second quarter, including a narrow gauge of economic activity that correlates highly with commodity markets called the Li Keqiang index. The index is composed of three factors: bank loans (40%), electricity production (40%) and rail freight (20%).

Unlike China’s official GDP, the Li Keqiang index has not shown negative growth during China’s pandemic shutdown, merely a slowing of growth from 8.9% YoY in December to 0.9% in January. Since then, growth improved to 2.3% YoY in February, 2.2% in March, 3.3% in April and 6.6% in May (Figure 4). By this measure, the slowdown in China’s industrial growth has actually been less severe and less prolonged than that in 2014 and 2015. While the rebound in the Li Keqiang index and the probable return to positive GDP growth in Q2 are positives for industrial metals, demand beyond China’s borders probably remains quite weak and this will likely impair China’s export growth for months to com

Figure 4: Le Keqiang Index Showed A Rebound In Growth In May

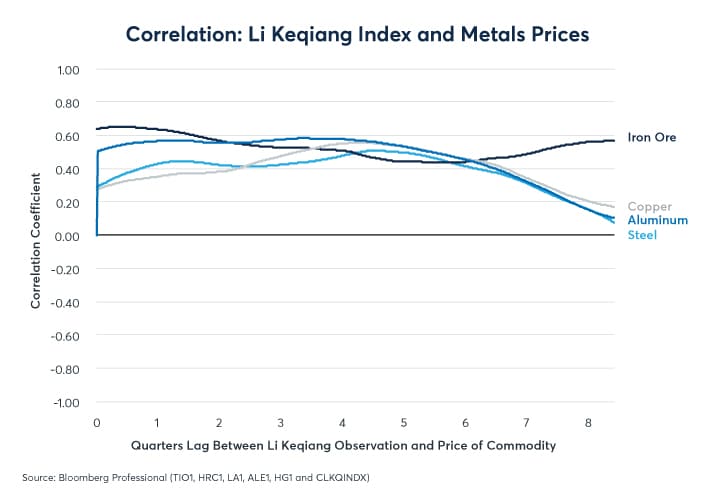

Over the past 15 years, industrial metals have shown a high correlation with Chinese growth – but often with a significant lag of up to 18 months (six quarters) (Figures 5 and 6). If experience is any guide, the true impact of the coronavirus on metals demand may not become fully apparent for six months to a year, or more. As such, the dip in Chinese and global demand in Q1 and Q2 2020 could impact prices well into 2021.

Figure 5: Over The Past 15 Years Copper Has Often Followed Li Keqiang Index With A Lag

Figure 6: All Industrial Metals Show A Strong Response To Changes In The Li Keqiang Index

Bottom Line

- Supply shocks have supported metals prices despite weak demand

- Mine shutdowns due to coronavirus have curbed output

- Chinese demand plays a central role in metals markets

- China’s economy likely rebounded in Q2 but the effects of pandemic could reverberate for years

To learn more about futures and options, go to Benzinga’s futures and options education resource.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.