The Viridian Cannabis Deal Tracker provides the deal data/terms/valuations/structures and market intelligence that cannabis companies, investors, and acquirers utilize to make informed decisions regarding capital and M&A strategy. This information service monitors capital raise and M&A activity in the legal cannabis industry. Each week the Tracker analyzes/aggregates all closed deals and allocates each transaction to one of twelve 12 key industry sectors in which the deal occurred (from Cultivation to Brands), the region in which the deal occurred (country or U.S. state), the status of the company announcing the transaction (public vs. private) and th type of deal structure (equity vs. debt).

Since its inception in 2015, the Viridian Cannabis Deal Tracker has tracked and analyzed more than 2,500 capital raises and 1,000 M&A transactions totaling over $45 billion in aggregate value. Find it exclusively on Benzinga Cannabis every week!

Note: this week, the tracker includes information for two weeks.

INVESTMENT AND M&A ACTIVITY IN THE CANNABIS INDUSTRY

01/13/2020 - 01/17/2020

CAPITAL RAISES

- The number of capital raises in week 3 was on par with the same period last year, but the aggregate dollars raised was significantly higher, mainly due to Curaleaf’s $300 million debt raise. This is likely to finance the very large acquisitions announced last year of Select brands and Grass Roots. These transactions are expected to close by February 2020.

- Terrascend raised capital in order to finance operations. This is a trend we are seeing where investors are deploying capital in order to keep businesses running after a very challenging 2019. This contributes to the overall feeling of capital drying up in the sector as the buy side doubles down on its existing portfolio companies as opposed to looking for new companies to finance.

- We continue to see a challenging private placement market as operators recalibrate to a new normal in regards to dilution. Most capital being deployed now is for previously announced deals or to finance operating costs for struggling businesses. We expect this trend to continue through at least the first quarter of 2020.

MERGERS & ACQUISITIONS

- We saw an uptick in M&A compared to recent months but still down year over year from 7 deals in the 3rd week of 2019 to 4 for the same period in 2020.

- The deals that were announced were relatively small. Consolidation is still necessary to drive value to consumers. The largest competitor to legal cannabis businesses is the illicit market. Legal companies will continue to seek out synergistic acquisitions that can help to lower prices while maintaining margins in order to compete with the black market.

- We expect to see more mergers of companies who find synergies within their supply chain. Acquisitions are smaller as a result of the perceived punishing dilution for buyers utilizing depressed stock for consideration.

WEEKLY SUMMARY

CAPITAL RAISES

MERGERS & ACQUISITIONS

01/17/2020 - 01/24/2020

CAPITAL RAISES

- Capital raise activity remains down compared to the same time last year as we tracked only 6 deals in this period vs 11 in the same period of last year.

- The average raise is down significantly to $6.4 million from $40.9 a year earlier. This statistic truly reflects the capital shortage in today’s market and the difference in investor sentiment from the beginning of 2019 to the beginning of this year.

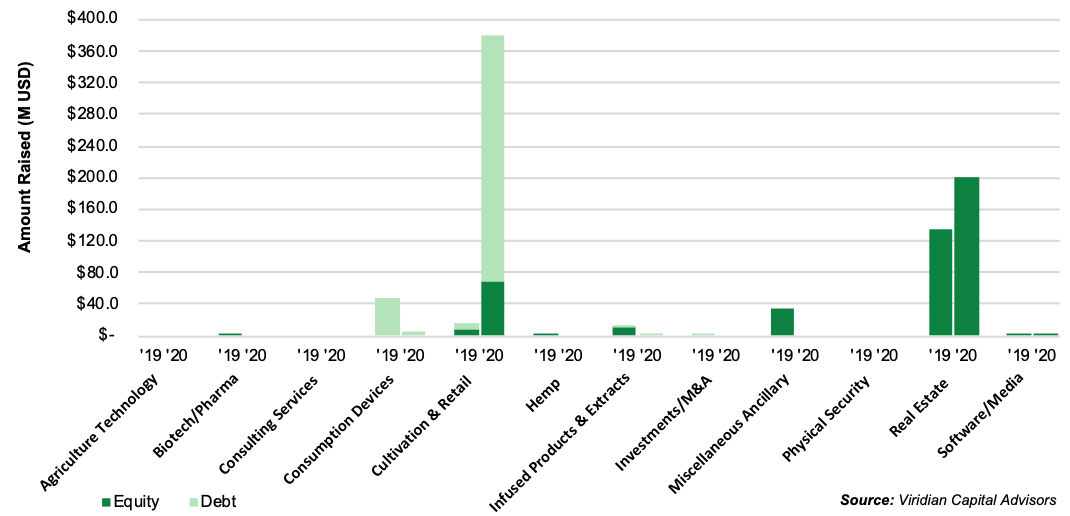

- The Cultivation & Retail sector accounted for 4 of the 6 raises, continuing its dominance over every other industry sector.

- We continue to see the majority of capital raising activity coming from publicly traded companies, even in a depressed valuation environment. This ability to raise capital even in down markets is a key advantage for public companies in this cash starved sector.

MERGERS & ACQUISITIONS

- M&A activity remains low as we saw only 3 deals in Week 4 vs 11 for the same period in 2019.

- Consolidation is still occurring but at a slower pace than we saw at this time last year. The entire marketplace of buyers and sellers is adjusting to the “new realities” of valuations and deal structures.

- It’s a buyer’s market today, particularly for publicly-traded companies pursuing privately-owned targets.

- Fyllo, a cannabis marketing and advertising firm based out of Chicago, acquired CannaRegs for $10 million after raising an $18 million Series A less than 6 months ago. We expect to continue to see M&A activity out of the growing Chicago cannabis community with the transition from medical to an adult use market.

WEEKLY SUMMARY

CAPITAL RAISES

MERGERS & ACQUISITIONS

YEAR-TO-DATE SUMMARY

CAPITAL RAISES

Capital Raises by Week

Capital Raises by Sector

MERGERS & ACQUISITIONS

M&A Activity by Week

M&A Activity by Sector

Photo by Javier Hasse.

The preceding article is from one of our external contributors. It does not represent the opinion of Benzinga and has not been edited.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Cannabis is evolving—don’t get left behind!

Curious about what’s next for the industry and how to stay ahead in today’s competitive market?

Join top executives, investors, and industry leaders at the Benzinga Cannabis Capital Conference in Chicago on June 9-10. Dive deep into market-shaping strategies, investment trends, and brand-building insights that will define the future of cannabis.

Secure your spot now before prices go up—this is where the biggest deals and connections happen!