The Non-Correlated Issue

The stock market is falling with the S&P 500 now down more than 10% from its 2023 high. Investors are starting to realize that “higher for longer” now includes inflation and government spending. Bond yields are rising despite the Fed signaling they’re done hiking for now. GDP is high, but misleading. Investors are flocking to alternatives like gold and Bitcoin BTC/USD. If you want to have a better understanding of what’s going on right now, keep reading.

This week, we’ll address the following topics:

-

Despite financial issues in China, Macau visitation is now back at 2019 levels.

-

Are we about to see more bank failures? Bank ETFs think we will.

-

How are gold and Bitcoin rising while Treasuries are falling?

-

3Q GDP up 4.9%. Do you believe that? We’re skeptical.

-

Coursera is still sandbagging guidance.

For those of you who want much more detail on the macro environment, here are links to two interviews from last week:

Lead Lag Report: https://www.youtube.com/watch?v=mV01sg6aB2k&t=1s

Complete Intelligence: https://www.youtube.com/watch?v=5oA_JWuM2-8&t=5s

Ready for a new week of shifting risk assets? Let’s dive in:

-

Macau is Back:

After three years of the most stringent lockdowns in the world, the Chinese government relaxed restrictions at the beginning of this year. That included slowly re-opening Macau, the gaming capital of the world, to greater visitation levels. This week, Inside Asian Gaming reports that visitation on some weekends in October are now back to 2019 levels.

Macau is back. Photo from Inside Asian Gaming.

DKI Takeaway: Visitation is now around pre-pandemic levels, but after years of not being able to gamble, the Chinese public has “pent up bankroll” meaning they have excess funds to wager. We’re seeing that at the tables as the average bet size is increasing. Combine that with a shift towards the higher-margin mass and premium mass market, and we like the implications for Las Vegas Sands ($LVS).

-

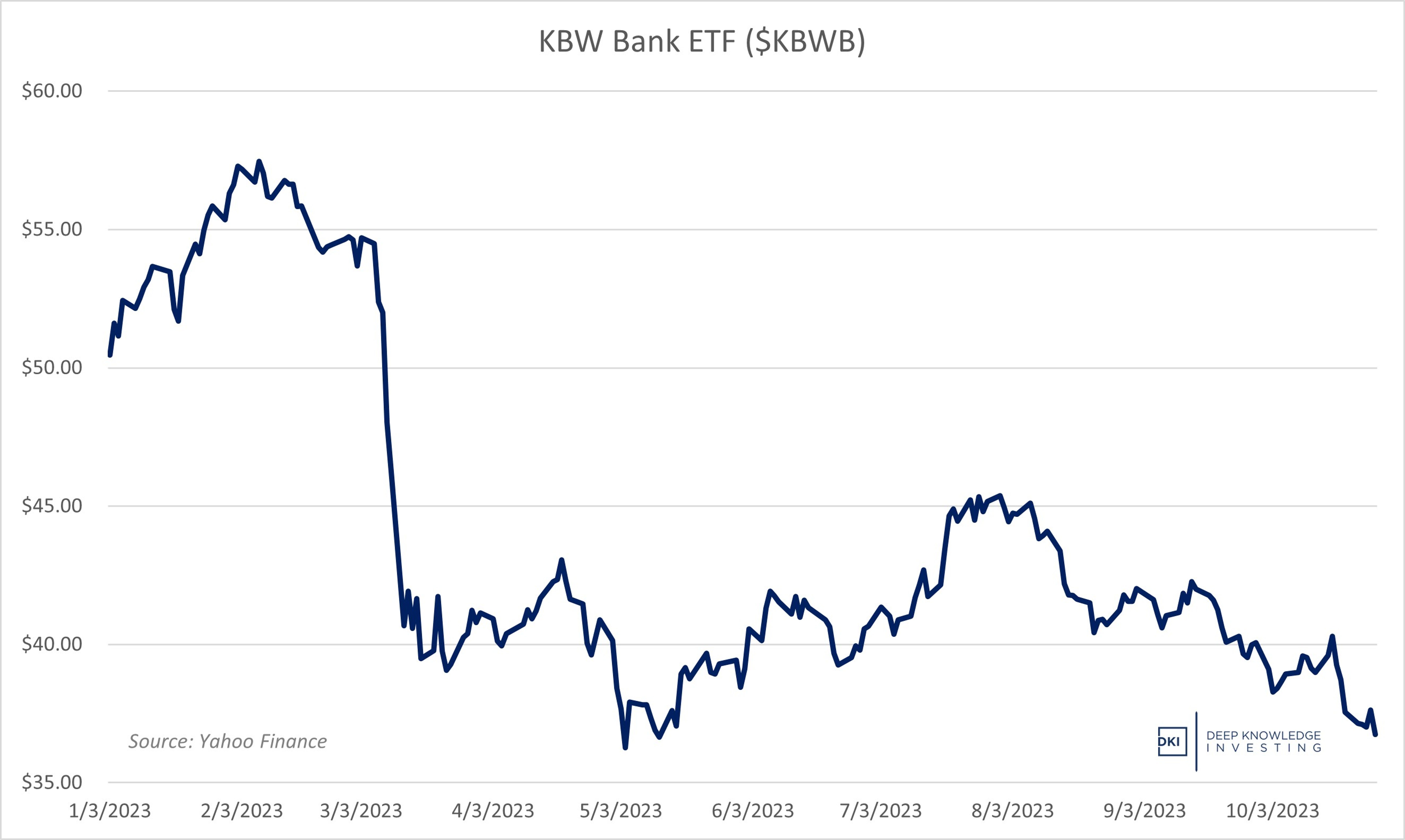

Banks Carrying Losses – Stocks Hammered:

Accounting regulations allow banks to avoid recognizing losses in their bond portfolios by designating the bonds as intended to be held to maturity. While it’s true that a bond held to maturity won’t cause a loss, this is misleading when a bank has demand deposits. Bank customers can request a withdrawal at any time forcing the bank to have to sell bonds trading at a discount to carrying value and causing the bank to recognize the loss then. When too much of this happens at once (a bank run), the bank’s losses can exceed its equity and cause a failure. This is what we saw at Silicon Valley Bancorp and First Republic earlier this year.

Multiple large drawdowns this year alone.

DKI Takeaway: Investors are starting to realize that many banks have the same problems as Silicon Valley and First Republic and are hiding the losses by mis-marking their balance sheets. In addition, depositors are moving funds away from banks and towards higher yielding alternatives. The KBW Bank ETF ($KBWB) has fallen from $46 to $36 in the last few months, the second large drawdown of the year. HT to Jack Farley for covering the issue in detail.

-

What’s Happening to the Flight to Safety Trade?:

I got an interesting question this week about the flight to safety trade. In October, we’ve seen higher prices for gold and Bitcoin while Treasury prices fell. Under more normal conditions, we might expect the risk-off trade to include all three of these assets. Seeing Treasuries decline while other wealth-storage alternatives rise is unusual.

Gold, Bitcoin, and $GBTC up from 9% to 30% in Oct. while the $TLT is down 5%.

DKI Takeaway: I think the gold, Bitcoin, and Treasury markets are all watching Congress. The spending deal agreed to earlier this year ensured we’ll see another $4T of debt between July and the next election. Add to that an extra few hundred billion of incremental interest expense and best case is we add another $4T - $5T in currency over approximately 18 months. That will lead to more inflation which is another way of saying a weaker future dollar. Investors are buying gold and Bitcoin to hedge against that. Bond investors are demanding higher interest rates to compensate.

-

GDP Growth is BIG – and Misleading:

3Q GDP was announced at 4.9%. That’s a huge number and well above expectations. As usual, DKI notes that government statistics do not represent reality; but rather, support a preferred narrative. For starters, inventory stocking of 1.3% in the quarter nets to zero over time and would take the GDP number down to 3.6%. The price index was only 3.0% which I believe is understated (unless someone wants to tell me their health insurance costs are down and their food inflation is under 4%). An accurate index number would lower GDP further. But it gets worse from there…

It was a great quarter as long as we don’t examine the details.

DKI Takeaway: Remember the massive spending agreement referenced earlier in this version of the 5 Things? The US government is on pace to overspend by $2 trillion this year despite having a growing economy and low unemployment. That spending adds to GDP even if there’s no value creation. The government is pulling future consumption forward and pretending that it’s adding economic value while ignoring the future obligations placed on the US taxpayer.

-

Coursera Has a Great Quarter – Guidance Still Conservative:

Coursera COUR stock has gotten hammered twice this year on terrible guidance. Each quarter, management provides revenue and EBITDA guidance for the following quarter and the full year. They’ve had a habit of warning about a cratering growth rate, but when pressed, admit that they’re just being conservative. Revenue growth each quarter this year has been above 21% and management has taken up full-year guidance each quarter.

Investors are starting to watch results instead of guidance.

DKI Takeaway: Let’s ignore guidance and look at platform growth. Registered learners grew by 6.5MM to 136MM in the quarter extending Coursera’s lead as the largest platform in online learning. Enterprise customers grew 21% to 1,315. Two years ago, that figure was 711. Even the previously-underperforming Degrees division grew students 15% at a time when college enrollment has been weak. $COUR has held on to pandemic learn-from-home gains from 2020/2021 and continued to grow. Despite beating 3Q revenue guidance and analyst estimates by a substantial margin, the company only raised 4Q revenue guidance by $2MM. We’ll take the “over”.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.