AT-A-GLANCE

- Fed hikes in 2022 the highest since 1981

- U.S. debt levels have doubled relative to GDP since the early 1980s

- Higher debt levels may make the U.S. economy more sensitive to rate changes

- The U.S. yield curve is strongly inverted, suggesting risk of a downturn

- Real rates are still negative using trailing measures of inflation, but not when using anticipated inflation

In 2022, the U.S. Federal Reserve (Fed) delivered the third biggest single year increase in interest rates of the past century, topped only by the rate tightening cycles of 1979 and 1981. In the years following the 1979 and 1981 tightening cycles, the U.S. economy was beset with deep economic downturns. In 1980, unemployment soared from 5.5% to 7.7% before a recovery took hold late in 1980 and early 1981. In late 1981 and through 1982, unemployment surged again, from 7.1% to 10.8%, the highest level since the Great Depression of the 1930s.

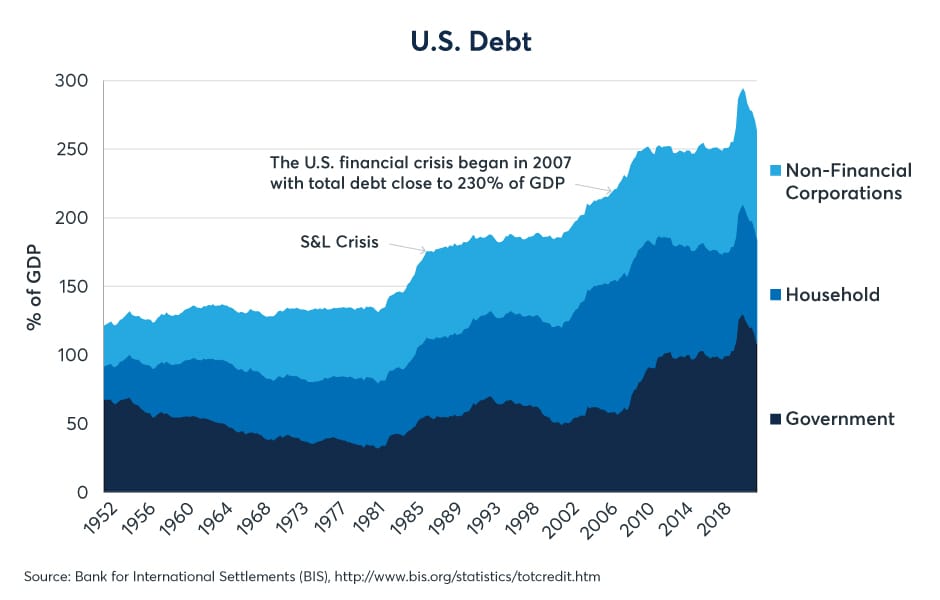

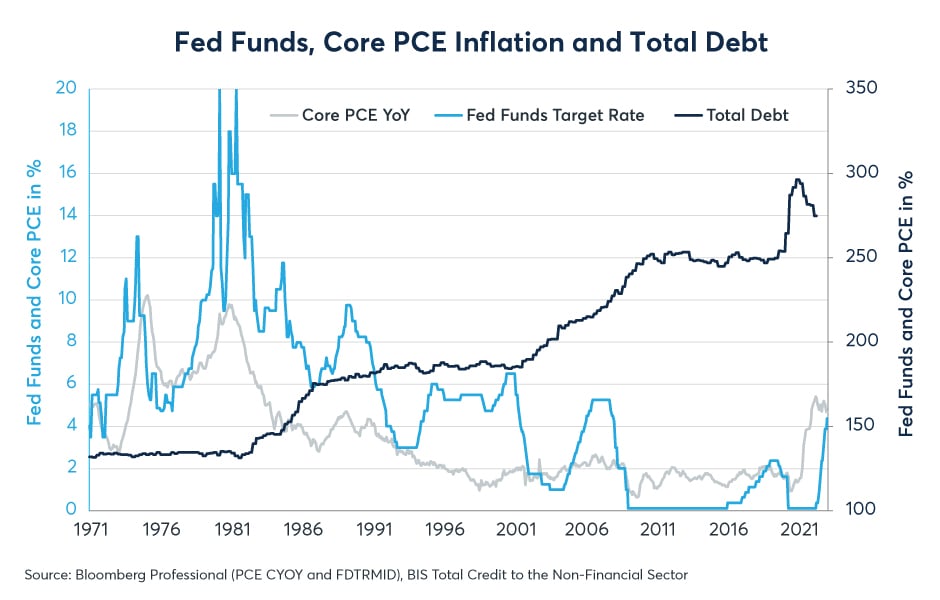

Any assessment of the likelihood of a downturn following the Fed’s most recent policy tightening cycle is complicated by two major differences between now and the early 1980s. They are, 1) the level of debt and leverage in the economy, and 2) the level of real interest rates. When the Fed sent rates soaring in the late 1970s and early 1980s, debt levels in the economy were roughly half of today’s levels. Between 1980 and today, the public debt to GDP ratio has risen from 33% to 108%, while household debt rose from 49% to 76%. Corporate debt rose from 51% to 80% (Figure 1). As such, the economy’s sensitivity to rate hikes could likely be much greater today than it was in the late 1970s and early 1980s when debt levels were much lower.

Scan the above QR code for more expert analysis of market events and trends driving opportunities today!

Figure 1: Overall debt to U.S. GDP ratio rose from 133% to 263% since the early 1980s.

In particular, the combination of rising interest rates and a very large public sector debt to GDP ratio might lead to significant pressure on the U.S. budget deficit as the federal government’s borrowing costs rise. This could force difficult choices between curtailing public spending, raising taxes or running larger deficits, which could cause the debt ratio to rise further. Moreover, private sector borrowing costs are also on the rise. Those with adjustable-rate mortgages could feel the pain quickly as their monthly mortgage payments increase. Meanwhile, corporate borrowing costs have also increased, which could force difficult choices regarding investments and hiring.

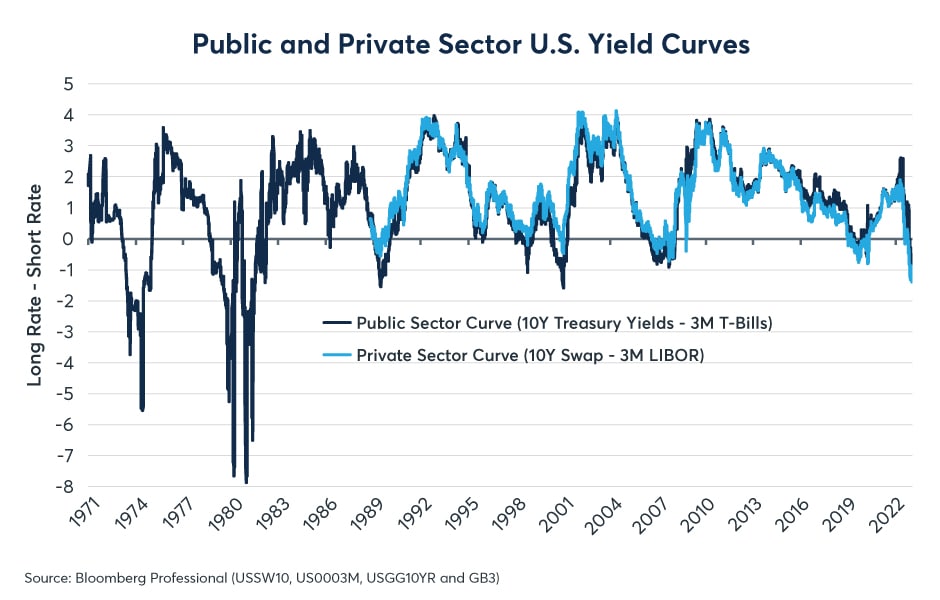

So, how concerned should we be about the possibility of an economic downturn in 2023 following the Fed’s 425 basis points of rate hikes (and counting) since March 2022? Interest rate traders are clearly worried, and their concerns are evident in the shape of the U.S. Treasury yield curve, which is now sharply inverted (Figure 2). The U.S. Treasury yield curve is now at its most inverted since 2007, the eve of the global financial crisis. That said, it is nowhere nearly as inverted as it was in the late 1970s and early 1980s when interest rates were much higher than they are today. Meanwhile, the private sector yield curve, which measures 10Y swap rates versus 3M LIBOR, is at its most inverted since records began in 1989.

Figure 2: The U.S. has among the sharpest yield curve inversions since the early 1980s

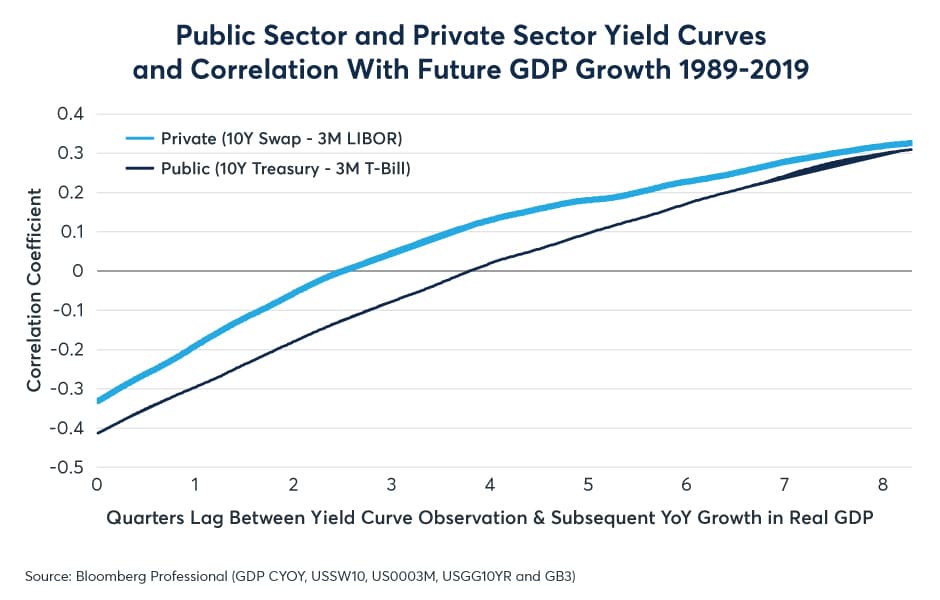

The record-breaking inversion of the private sector yield curve is of particular concern since it has a stronger historical correlation with future U.S. GDP growth than does the public sector curve. The correlation between the shape of the yield curve and subsequent economic performance is strongest one to two years in advance (Figure 3). As such, from this perspective, it is possible and even likely, that the U.S. economy continues to grow at a decent pace in the first half of 2023, but as we get into the second half of this year and 2024, the likelihood of a downturn might begin to grow.

Figure 3: The private sector yield curve is an especially strong forward indicator of GDP growth

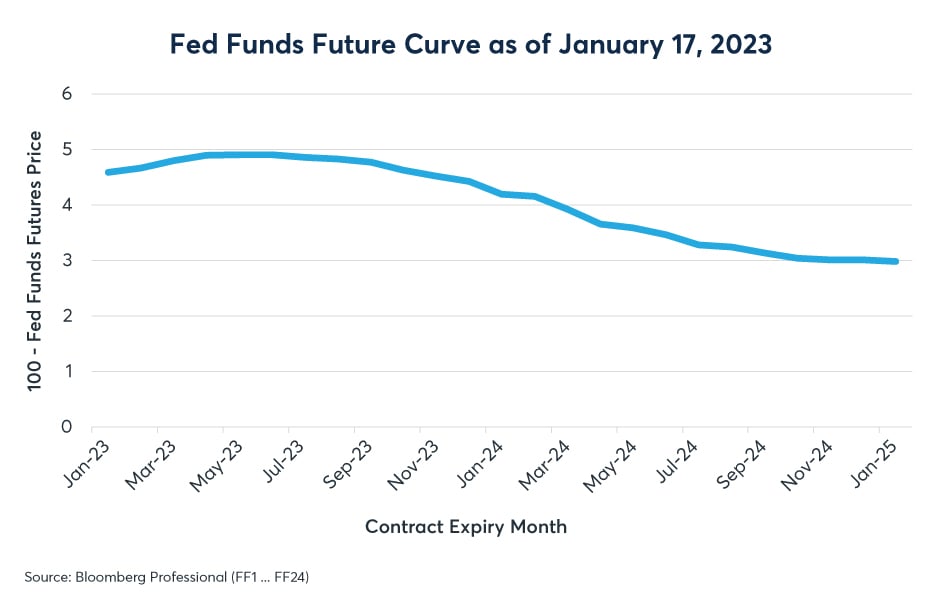

The shape of the Fed funds curve is also extraordinary. As of early January, traders priced that the Fed might hike one or two more times in Q1 2023 before putting rates on hold until the fourth quarter. Starting in Q4, traders are pricing that the Fed could begin slashing interest rates by 150-200 basis points (Figure 4). The shape of the forward curve for Fed policy rates highlights concerns that the Fed might have to rapidly reverse its recent policy tightening later this year.

Figure 4: Fed Funds Futures anticipate Fed hikes towards 5% rates, followed by sharp cuts

There are, however, a number of complicating factors. Among them is the fact that the Fed has not yet raised interest rates up to the level of core inflation. Prior to previous downturns, Fed rates typically exceeded the rate of inflation by a significant amount. The Fed funds rate was close to +3.0% in real terms (Fed funds rate – core PCE, or personal consumption expenditures) before the 2001 and 2008 recessions. It was close to +5% prior to the downturn in 1990-91. Back in 1979 and 1981, the Fed pushed rates to 7-8% above core PCE (Figure 5).

Figure 5: Using trailing inflation as a measure, real rates are still negative

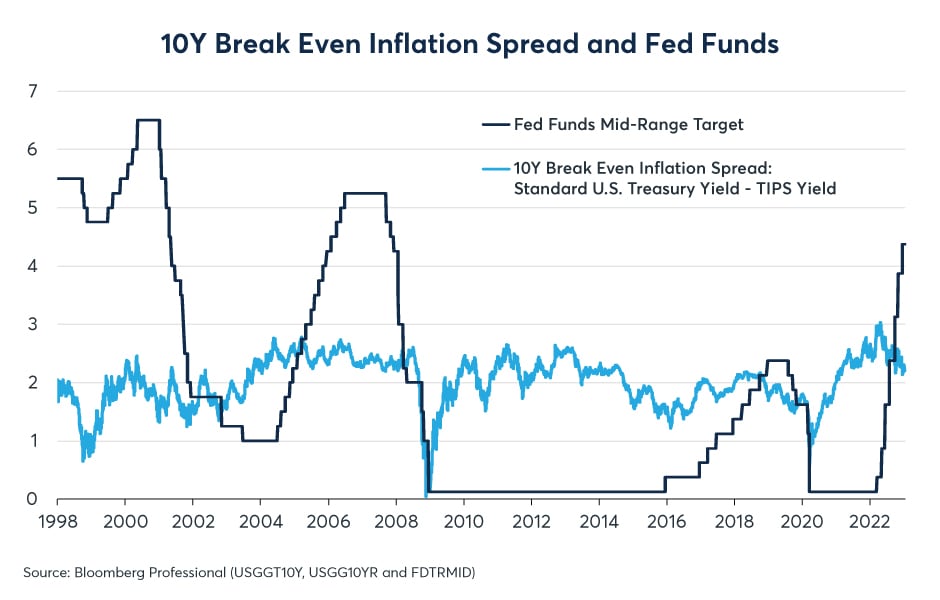

This time around, the Fed funds rate is at 4.375%, a full percentage point below core PCE. This begs the question: Is monetary policy even tight at all, or is it still loose? Herein lies yet another complication. Real rates are only negative if one looks at trailing inflation based on the various inflation indexes that measure what inflation has been recently. However, if one looks at anticipated inflation based on the break-even spread between standard U.S. Treasuries and Treasury Inflation-Protected Securities (TIPS), real rates are just as positive today as they were back in 2000 or 2007 on the eve of the two previous endogenous recessions (not counting the exogenous hit to the economy from the COVID lockdowns in 2020) (Figure 6).

Figure 6: Real rates are positive when looking at anticipated inflation implied with TIPS

One thing is clear, as debt levels have risen across the economy over the past 40 years, the level of real interest rates has tended to fall. If the Fed puts real rates at +7% today like it did in the late 1970s and early 1980s, that would mean rates of 9.5% using the break-even inflation spread or 12.5% using core PCE. Rates at that level are scarcely imaginable today in no small part because the highly leveraged nature of today’s economy would make such rates unsustainable.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.