To Our Readers: This will be our last regularly scheduled Daily Market Update for 2022, unless there’s significant market volatility next week. Otherwise, we’ll be back Tuesday morning, January 3. We hope you have a wonderful holiday and thank you for reading!

(Friday Market Open) Stocks wavered early Friday ahead of the three-day holiday weekend as market participants digested a host of economic data that poured in just before the open.

Most prominently, the Federal Reserve’s favored inflation indicator, Personal Consumption Expenditure (PCE) prices, rose 0.1% month-over-month in November, a bit below the consensus of 0.2%, while core PCE, which strips out energy and food, rose 0.2%. Expectations had been 0.3%.

Durable Goods Orders fell a hefty 2.1% in November and Personal Spending rose just 0.1%, which could be a bullish sign in this “bad news is good news” environment where so many are sensitive to the Fed’s next move.

The durable goods number clearly shows things are slowing down, even as today’s November Personal Income data showed that spending on goods fell while spending on services rose. Higher interest rates appear to be hitting goods demand but not services, something to watch into the new year for its potential impact on inflation.

Overall, year-over-year core PCE prices rose 4.7%, in line with expectations—there’s nothing in these PCE numbers really earth shattering.

Digesting Data

Markets turned lower after the rush of data, despite PCE prices coming in below expectations. One reason might be the combination of personal income rising while durable orders fell. That could imply more margin-squeezing ahead for companies, with a corresponding impact on earnings potential.

We’re not done with data yet today. Soon after the opening bell, November New Home Sales arrive and we’ll get a final read on University of Michigan Consumer Sentiment. If those numbers are as expected (see below), the market might stay placid. Anything seriously out of line, however, could bring volatility.

Turning overseas, Japan’s inflation rate was 3.7% in November, the loftiest in four decades. Also, China estimates that more than 30 million people a day are getting infected with COVID-19, according to Bloomberg.

Back home, the number to watch today is 3,800 on the S&P 500® index (SPX). That’s the level that buying interest appears to show up at, and bulls successfully defended it again yesterday. One thing that might have been a factor in the late rebound from lows yesterday was some bargain hunting. We’ll see if that’s a factor again.

Some of the mega-caps inched higher this morning, and they’ll probably have a lot to do with whether the market can close the week on a positive note despite being headed for its third straight week of losses. Heavyweights like Apple AAPL, Amazon AMZN, and Tesla TSLA all are scraping near their lows for the year, and since their market capitalizations are so high and the SPX is a weighted index, this softness in mega-caps is a big reason for the recent market struggles. Another reason appears to be tax-loss harvesting ahead of the new year.

Morning Rush

- The 10-year Treasury yield (TNX) rose 4 basis points to 3.71%, its highest level this month.

- The U.S. Dollar Index ($DXY) remains roughly flat at 104.24.

- Cboe Volatility Index® (VIX) futures eased to 21.67.

- WTI Crude Oil (/CL) climbed more than 2% to $79.23.

The market has been trying to convince itself that the Fed will let up in the face of an economic slowdown, despite repeated hawkish statements from Fed Chairman Jerome Powell and other Fed officials. As we noted yesterday, the market continues to price in a terminal federal funds rate for 2023 below 5%, even though the Fed clearly said it plans to raise rates to 5%–5.25%. Thursday might’ve represented that some remaining optimists finally threw in the towel.

Up Next: More Data

November New Home Sales and final University of Michigan Consumer Sentiment for December both cross the wires at 10 a.m. ET today, and then we’re done with data for the week.

- Consensus for New Home Sales is a seasonally adjusted 600,000, down from 632,000 in October.

- Consumer Sentiment is expected to be 59.1, even with the initial December estimate, according to Briefing.com. Sentiment has been soft for months, implying that consumers may not be primed to spend.

- Another part of the report that could grab the market’s attention is one-year inflation expectations, which fell from 4.9% to 4.6% in the initial December report, the lowest in 15 months. It’ll be interesting to see if that number changed, especially with the Federal Reserve so concerned that inflation expectations could become entrenched, leading to a wage-price spiral.

Thinking Cap

Russian physiologist Ivan Pavlov demonstrated that dogs would salivate at the sound of a bell if they associated bell-ringing with the arrival of food. It’s called Pavlovian conditioning.

When it came to the Fed, Wall Street used to salivate during steep economic downturns, fully expecting that if shares fell far enough, the Fed would step in and lower rates or use its megaphone to make things better.

Things seem to be different now, given some of the most unusual market conditions in recent history. But somehow, the Fed can’t make the market unlearn that habit of expecting central bank help, which becomes quite apparent if you look at major stock index performance over the last six months.

The SPX rallied 17% from mid-June to late-August until Fed Chairman Jerome Powell popped the balloon with his hawkish remarks at the Fed’s Jackson Hole summit. Again, a smaller rally that began in mid-October got quashed by Powell’s tone at his press conference after the Fed’s November 2 rate decision. Then the market rallied another 8% from early November to mid-December, again with bulls convinced (in part by more bullish inflation data) that a more dovish Fed would show up at the December meeting. We know how that turned out.

These three rallies were predicated on ideas the Fed would indicate a light at the end of the tunnel on rate hikes. Every time these rallies occurred, the Fed basically told Wall Street that the light was coming from an approaching train. The market appeared to take heed for a while each time only to rally again.

It may reflect a simple human propensity to be optimistic. It may also be reflexive on investors’ part, acting on more than 20 years of accommodative Fed history enabling rallies even when the economic and corporate earnings picture didn’t justify them. It’s hard for many of us to get used to a Fed that operates in the exact opposite way, trying to take steam out of rallies instead of encouraging them.

Basically, the Fed’s jumped on the inflation-fighting wagon, and Wall Street hasn’t caught up. But perhaps seeing three rallies smashed to smithereens by Powell and company in the last six months could finally do the trick.

All this means that it’s probably a good idea to remain cautious heading into 2023. It doesn’t necessarily mean you need to take dramatic measures if you’re a long-term investor, but in no uncertain terms, the Fed is discouraging rallies. As for the SPX, it’s now down more than 20% year to date and is having its worst December in four years. Where will it be come late January as the next Fed meeting approaches?

Don’t fight the Fed, as the old saying goes.

Reviewing the Market Minutes

Major stock indexes skidded Thursday to their lowest intraday levels since early November, following more evidence that the Federal Reserve has work to do cooling off the economy. A sizzling Q3 Gross Domestic Product (GDP) report and lower-than-expected jobless claims sparked the sell-off—though the SPX did manage to claw back in the last hour from its worst levels of the day and close above what some see as technical support at 3,800.

While the upwardly revised GDP data was what started it all, hedge fund manager David Tepper told CNBC Thursday morning that everyone should believe the Fed when it says it’s committed to tightening—and that was the final blow. Once Tepper spoke his bearish words, they quickly ricocheted across Wall Street.

Risk-off came back into the mix Thursday as sectors like health care, utilities, and staples were among the leaders. Consumer discretionary and info tech rounded out the bottom of the daily sector numbers. The rate-sensitive semiconductor sector lost more than 4%, and info tech is having its worst December since 2002.

Here’s how the major indexes performed Thursday:

- The Dow Jones Industrial Average® ($DJI) fell 349 points, or 1.05%, to 33,027.

- The Nasdaq® ($COMP) slipped 2.18% to 10,476.

- The Russell 2000®(RUT) dropped 1.29% to 1,754.

- The SPX lost 56 points, or 1.45%, to close at 3,822.

Talking Technicals: There’s some resilience under the market as yesterday’s comeback in the last hour showed. Buyers surfaced after the SPX fell below 3,800 and managed to close well above that round number after its early afternoon slide to 3,764, the lowest intraday read since November 9. Also, it’s worth noting that Thursday’s 3,822 close marked yet another date in which the SPX managed to hold above a key Fibonacci retracement level of the March 2020 through January 2022 rally that stands near 3,819. That remains an interesting number on the charts.

Still, 3,800 may be even more important. Twice this week, the SPX dropped below that intraday, and each time, it found buyers. It shows when things really sell off, buyers come in, and that makes 3,800 a more important post-holiday level.

Did you know, by the way, that Charles Schwab delivers an end-of-day market update podcast each trading session after the close? Be sure to check it out.

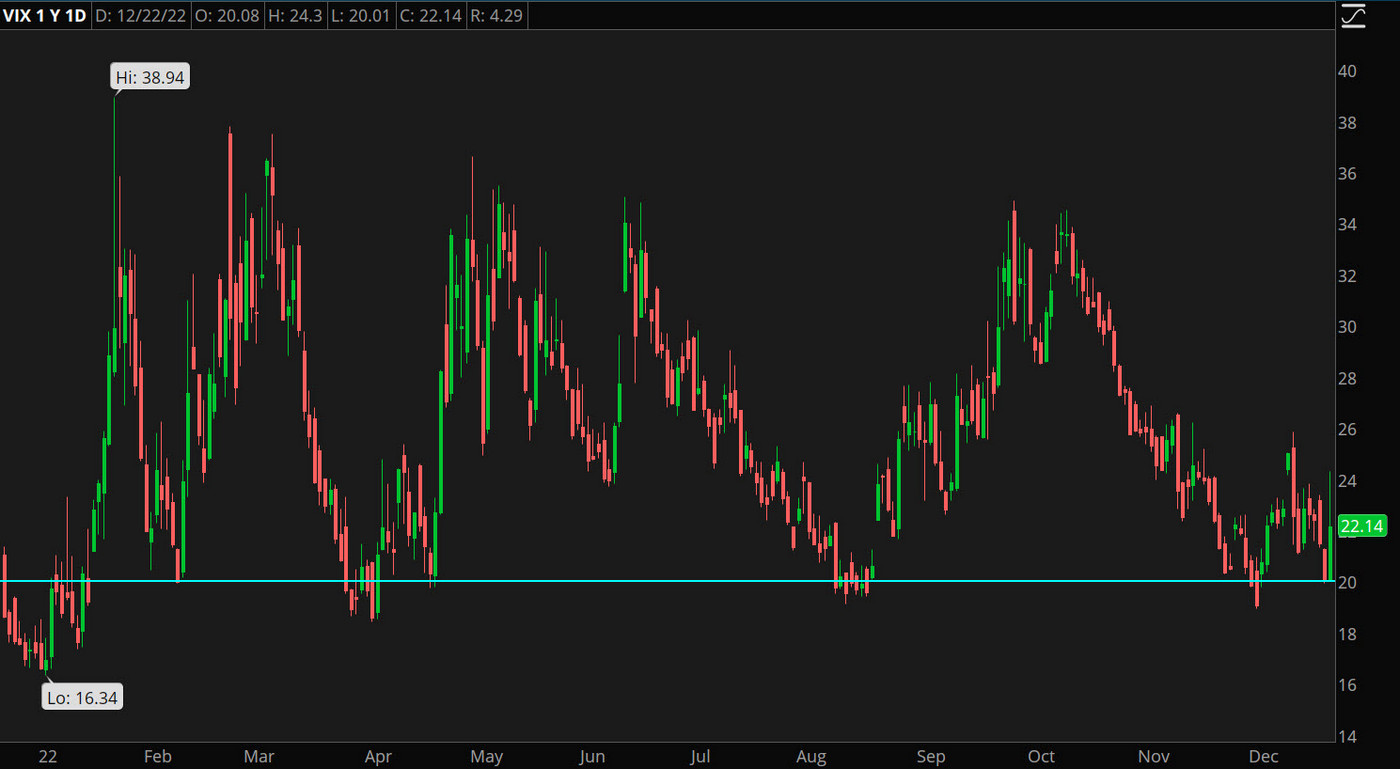

CHART OF THE DAY: A YEAR OF FEAR. The Cboe Volatility Index (VIX) dipped below 20 (blue line) earlier this week, but not by much, and not for very long, considering Thursday’s steep sell-off. But if you look at a chart of 2022, you’ll note that’s been the case all year. Just when you think the fears are in check, and VIX responds by dipping below 20 (broadly seen as the dividing line between normal vs elevated risk), another wave of volatility has come along. Data source: Cboe Global Markets. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

Data Takes a Holiday: If you’re heading out of town for the holidays and worried about missing key economic data next week, don’t be. The calendar next week is as bare as they come, with almost no major reports expected other than the usual weekly updates on initial jobless claims and crude oil inventories. The only exceptions are reports that normally have a low impact even when people are around trading, like the S&P Case-Shiller October Home Price Index due Tuesday and the December Chicago PMI on Friday. Chicago PMI was extremely weak in November with a much softer than expected headline number of 37.2, so we’ll see if it rebounded at all. If you want earnings, nothing’s on the calendar next week, but you’ll probably like the January schedule.

Java Watch: This may sound implausible if you recently paid $5 for a cup of it, but coffee futures prices recently dripped to levels last seen in mid-2021, falling under $1.60 a pound last month on the Intercontinental (ICE) Exchange. They’re still under $1.80, thanks in part to what Trading Economics called “ample” global supplies. Still, all eyes are on the Brazilian crop, which recently got downgraded by farmers and exporters there. If coffee remains relatively cheap, that could be a tailwind for certain companies, perhaps helping margins for firms like Starbucks (SBUX) and McDonald’s (MCD), which sell the stuff by the bucket. Lower coffee prices also can help manufacturers J.M. Smucker (SJM), which owns Folgers and Dunkin’, and Coffee Holding Co. (JVA), which includes Private Label and Wholesale Green coffee, or coffee roaster and distributor Farmer Brothers (FARM).

Anybody Home? Prospective homebuyers are continuing to see glimmers of hope on the mortgage rate front—but oh, if there was just more to buy. Freddie Mac said Thursday that the average 30-year mortgage was down for the sixth week in a row to 6.27%. However, sellers remain reluctant. According to Sam Khater, Freddie Mac’s chief economist, many homeowners are “carefully weighing their options as more than two-thirds of current homeowners have a fixed mortgage rate of below 4%.”

Notable Calendar Items

Dec. 26: Markets closed for official Christmas Day holiday. Enjoy if you celebrate! Reader’s note: Unless there is significant market volatility, Daily Market Update will return January 3.

Dec. 27: December Consumer Confidence

Dec. 28: November Pending Home Sales

Dec. 29: Weekly Initial Unemployment Claims

Dec. 30: December Chicago PMI

Jan. 2: Markets close in observance of New Year’s Day. Happy holidays!

Jan. 3: November Construction Spending.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.