On May 8, 2013, Alexza Pharmaceuticals, Inc (NASDAQ:ALXA) and Teva Pharmaceuticals USA, Inc (NYSE:TEVA) announced that the two companies have entered into an exclusive U.S. license and supply agreement for ADASUVE (loxapine) inhalation powder 10 mg for the acute treatment of agitation associated with schizophrenia or bipolar I disorder in adults. Teva will be responsible for all U.S. commercial and clinical activities for ADASUVE, including U.S. post-approval clinical studies, and has gained rights to conduct additional clinical trials of ADASUVE for potential new indications in neurological disorders. Alexza will be responsible for manufacturing and supplying ADASUVE to Teva for commercial sales and clinical trials.

Under the terms of the license and supply agreement, Alexza will receive an upfront cash payment of $40 million and is eligible to receive up to $195 million in additional milestone payments, based upon successful completion of the ADASUVE post-approval studies in the U.S. and achieving net sales targets. In addition, Teva will make tiered, royalty payments based on net commercial sales of ADASUVE in the US.

Via a five-year convertible note and agreement to lend, Teva will make available up to $25.0 million which Alexza may access to support its ADASUVE activities. Alexza may prepay up to 50 percent of the outstanding amount at any time prior to maturity. Teva may convert, at maturity, all or a portion of the then outstanding amount under the note into equity of Alexza.

Most investors believe that the Teva deal is a very good deal for Alexza because Teva brings an established commercial presence in hospital and psychiatric markets, and because Teva has extensive experience marketing and selling hospital-based drugs, and drugs that have an FDA Risk Evaluation and Mitigation Strategy (REMS) requirement. In addition, Teva is a top 10 global pharmaceutical company with a direct presence in over 60 countries worldwide, with over 46,000 employees worldwide, and generated sales of over $20.3 billion during 2012. In the U.S. alone, Teva has locations in 13 states, and over 9,000 employees. Teva is planning to commercially launch ADASUVE in the U.S. during the 2nd half of 2013. Teva will decide and announce exactly when ADASUVE will be launched in the U.S.

Grupo Ferrer Internacional, S.A. is Alexza's commercial partner for ADASUVE in Europe (the E.U.), Latin America, Russia and the Commonwealth of Independent States. Grupo Ferrer is planning to launch ADASUVE in the E.U. during the 3rd quarter of 2013, starting in the countries of Germany and Austria.

My valuation analysis of Alexza is based on discounted cash flow projections resulting solely from the sale of ADASUVE in the U.S. and the E.U. for the next 10 years. My valuation analysis indicates that Alexza stock should be valued at approximately $16.28 per share after the Teva deal. In this article, I am going to share my analysis of valuing Alexza after the Teva deal for commercializing ADASUVE in the U.S. was announced. The major key assumptions for Alexza and ADASUVE that I used in my analysis cover the following areas: potential U.S. market size, estimated U.S. market share, estimated market share in the Grupo Ferrer territory, transfer price per ADASUVE inhaler, revenue per ADASUVE inhaler, tiered royalty percentages, milestone payments, general & administrative expenses, research & development expenses, federal income taxes, payments to Symphony Allegro, long-term debt, weighted average cost of capital (WACC), and growth rate at terminal. I will detail each of my key assumptions below.

ADASUVE Potential Market Size & Projected Sales

According to the National Institute of Mental Health (NIMH), schizophrenia occurs in the U.S. general population at the rate of about 1.10%, and bipolar disorder occurs at the rate of 2.60%. Of those individuals who are diagnosed with schizophrenia or bipolar disorder, about 90.0% of those will suffer from acute agitation, and about half of those will seek treatment. In the past, Alexza has provided investors with the following financial guidance related to ADASUVE:

- The average patient will experience 11 to 12 acute agitation episodes per year.

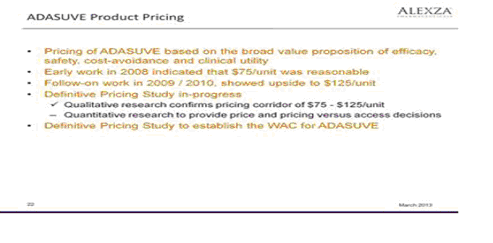

- The price of ADASUVE will be about $75 per inhaler, but there is some upside room to raise the price of ADASUVE up to $125 per inhaler.

- Alexza will break even in 2015 with gross ADASUVE top-line sales in the US of at least $85.0 million.

- The peak annual revenue for ADASUVE in the U.S. market alone is estimated to be in excess of $225.0 million based upon an average cost of $75 for each ADASUVE unit sold. The peak annual revenue is based on adult patients in the U.S., who are treated in a hospital setting only, and does not include ADASUVE sales from a possible expanded label to include self-administered ADASUVE in the patient's home by the patient or by their caregiver, nor does it include a possible expanded label to include adolescent patients (age 13 to 17).

You can see this Alexza provided ADASUVE guidance on the two Alexza slides below:

(click to enlarge)

(click to enlarge)

In my Alexza valuation,I projected ADASUVE revenue for the next 10 years by using the Alexza provided guidance, but I used more conservative assumptions than the guidance provided by Alexza, including the following assumptions:

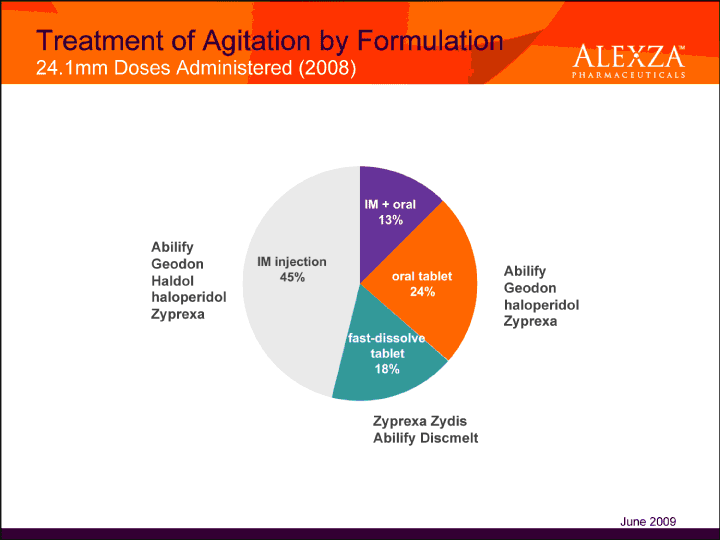

- My valuation assumes that ADASUVE will only capture less than 1.00% market share in Year 1, to about 6.25% of the acute agitation market during the next 10 years. The current market for the treatment of acute agitation is dominated by oral tablets and intramuscular injections (IM Injections). Currently, oral tablets account for about 55.0% of the acute agitation treatment market, and IM injections account for about 45.0% of the treatment market. You can see this on Slide 3 below:

(click to enlarge)

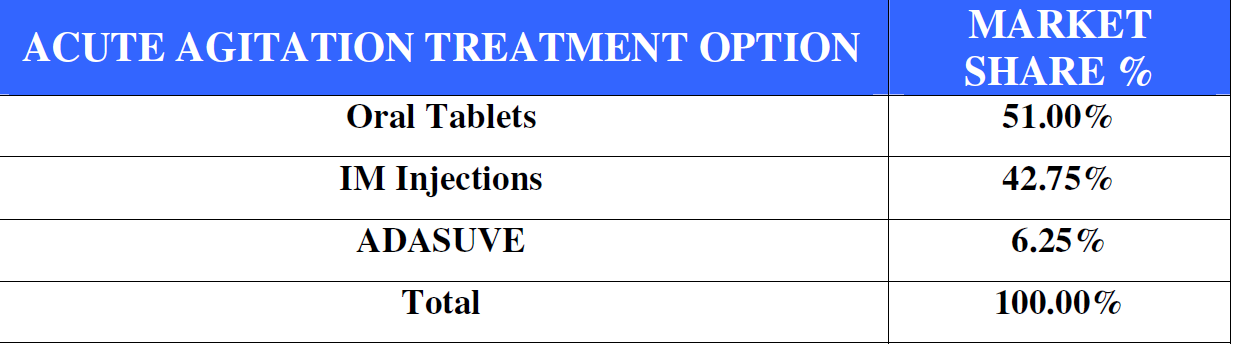

My valuation assumes that the market share for each treatment option for acute agitation after ADASUVE is launched, and after ADASUVE reaches peak sales levels will be as follows:

(click to enlarge)

- At peak sales in Years 8 to 10, I am conservatively estimating that Alexza will only capture about 4.00% of the acute agitation treatment market share from oral tablets, and only about 2.25% of the market share from IM injections.

- My valuation conservatively projects that each ADASUVE patient will only experience about 10 acute episodes per year, even though most patients actually experience 11 to 12 episodes per year as indicated on Alexza's Slide 1 above.

- My valuation conservatively projects that each ADASUVE inhaler will be priced at $75 per unit for the first 2 years, and then the average price will increase to $77 to $82 during years 3 to 10. This is a conservative assumption because Alexza has stated that their market research shows that the price of ADASUVE could be increased to as high as $125 per unit. You can see this on Alexza's Slide 2 above.

- My valuation conservatively projects that ADASUVE sales in the Grupo Ferrer territory (Europe, Latin America, Russia, and the Commonwealth of Independent States) will only be about 25% of the U.S. sales for the first two years, then it will increase to 30% during the next two years, and then it will increase to 35% during years 5 to 10. My valuation assumption is conservative because Alexza has guided that they believe that the E.U. market opportunity for ADASUVE will be 40% to 50% of the size of the U.S. market opportunity. In addition, on page 2 of the ADASUVE label approved by the EMA, the EMA allows for up to two (2) doses of ADASUVE per day, compared to only one (1) dose per day for the FDA approved label. As a result, there could be a lot more upside for ADASUVE in the E.U. than most observers anticipate.

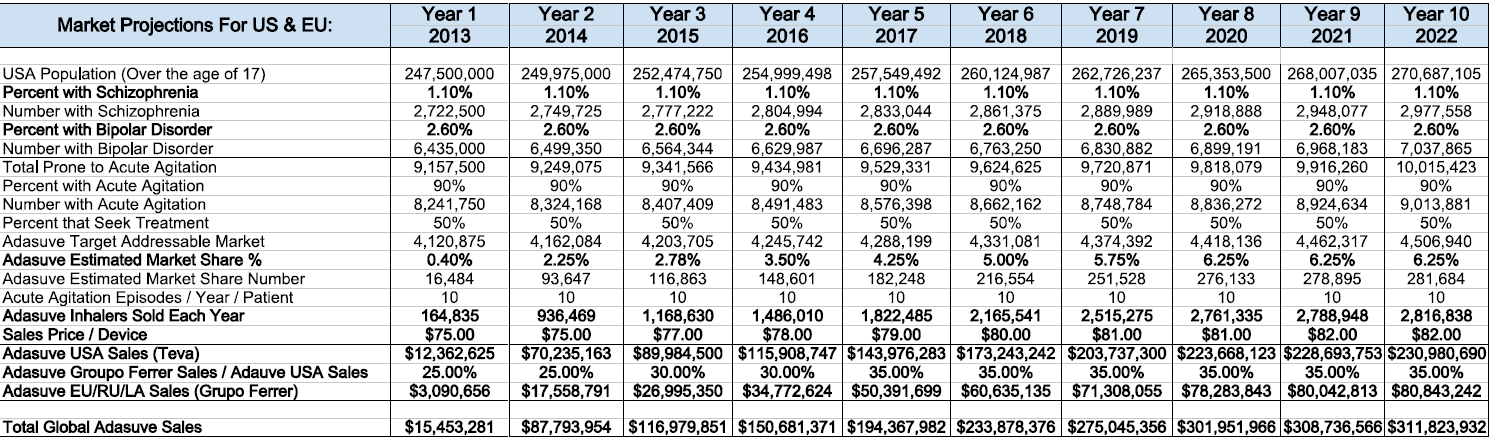

Here is a copy of my Alexza valuation spreadsheet that details all of the key assumptions I used to determine the size of the potential market for ADASUVE in the U.S. and the E.U. In addition, this spreadsheet also shows the total ADASUVE sales for Teva and Grupo Ferrer in the U.S. and E.U., respectively.

(click to enlarge)

ADASUVE Revenue Projections for The U.S. & E.U.

As a result of its partnerships with Teva and Grupo Ferrer, Alexza will earn revenues from three different sources: (1) ADASUVE tiered royalty payments, (2) ADASUVE manufacturing profits, and (3) ADASUVE milestone payments. Alexza has not disclosed exactly what the tiered ADASUVE royalty percentages are that Teva will pay to Alexza. But, Alexza did provide the following guidance related to the Teva royalty rates: "the royalty rates are competitive rates and are standard for products of this size and for this category". Some analysts estimate that the royalty percentages will range from 20.0% to 25.0% of ADASUVE sales. However, for my valuation analysis, I used a more conservative range for royalty percentages. In connection with the Teva ADASUVE deal, I used a royalty percentage range starting at 18.0% in Year 1 and scaling up to 25.0% in Years 8 through 10, based upon increased sales levels through Year 10. In connection with the Grupo Ferrer deal, I used a royalty percentage range starting at 15.0% in Year 1 and scaling up to 20.0% through Year 10. I will update my valuation after Alexza and/or Teva releases more information about the royalty percentages and sales levels tiering.

The next source of revenue that Alexza will earn will be a manufacturing profit on each ADASUVE unit that is produced by Alexza and sold to Teva and Grupo Ferrer. Alexza has not provided specific numbers to tell us how much this manufacturing profit will be, but they did provide the following guidance:

- Alexza will manufacture and supply all ADASUVE for both Teva and Grupo Ferrer.

- Alexza will charge Teva and Grupo Ferrer a transfer price that will include the fully-burdened manufacturing cost plus a small embedded profit for each ADASUVE unit.

In an agreement between Dendreon and Kirin Brewing Company, fully-burdened manufacturing cost was defined as follows: "Fully-Burdened Manufacturing Costs' means the actual fully burdened costs and expenses of manufacturing a particular Component, including without limitation the costs of all raw materials and labor (including all allocable benefits) used or consumed in such manufacture, Third Party contract manufacturing costs, packaging costs and expenses, all quality assurance and quality control related expenses, all overhead amounts allocable to such manufacturing (including without limitation appropriately amortized capital equipment costs), all royalty amounts payable by Supplier to any Third Party based upon the manufacture of such Component, and all amounts related to failed production units or yield losses, all the foregoing as calculated in accordance with (I) U.S. generally accepted accounting principles consistently applied for manufacture of Components by Dendreon and (ii) Japan's generally accepted accounting principles consistently applied for manufacture of Components by Kirin".

In order to estimate what the Alexza manufacturing profit will be for each ADASUVE unit, I decided to use the transfer price as an approximation of the cost of goods sold and the cost of goods manufactured that Teva would incur for ADASUVE. On page 7 of the Q1 2013 10-Q, Teva reported an average gross profit margin of 84.7% for its branded specialty drug products. The formula to calculate the gross profit margin is the following:

Gross Sales: 100.0%

Less: Cost of Goods Sold: 15.3%

Gross Profit Margin: 84.7%

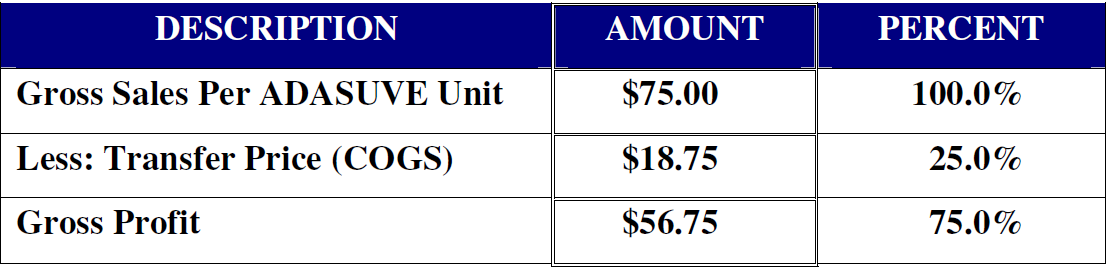

I assumed that the Teva gross profit margin for ADASUVE will be a little less than the average for Teva's branded specialty drugs because: (1) Alexza will be able to include the fully-burdened manufacturing costs in the ADASUVE transfer price. As a result, some of the costs that are normally below the Alexza gross profit line, including some R&D expenses, and some G&A expenses can be allocated to and included in the transfer price, and (2) Alexza is able to include a small embedded profit for each ADASUVE unit produced in the transfer price. As a result, I decreased Teva's ADASUVE gross profit margin to 75.0% from 84.7%. Then, I was able to plug-in the $75 sale price for each ADASUVE unit that Teva will sell , and take the gross profit margin of 75.0% to derive the Alexza transfer price (COGS) of 25.0% for each ADASUVE unit as follows:

(click to enlarge)

I maintained the same transfer price per unit to sales price per unit ratio of 25.0% throughout my 10-year projection. Once I calculated the transfer price (COGS) for ADASUVE, I conservatively assumed that Alexza will make a gross profit margin or manufacturing profit of about 5.0% of the transfer price for each ADASUVE unit produced for Teva. For Year 1 that manufacturing profit per unit was $0.94, and it increased to $1.03 per unit by Year 10. I will update my analysis once Alexza provides more details about the Teva transfer price and manufacturing profit for each ADASUVE unit.

To determine manufacturing profits for the Grupo Ferrer territory, I kept the same relationship between the Grupo Ferrer E.U. sales versus the Teva U.S. sales. As a result, I calculated the ADASUVE E.U. manufacturing profits to be 25.0% of the U.S. manufacturing profits during Years 1 and 2, and then it was scaled up to 35.0% for Years 5 to 10.

In connection with the Teva milestone payments for ADASUVE, Alexza gave the following guidance: (1) the total potential milestone payments is up to $195.0 million, (2) the milestone payments would be earned based on Alexza achieving both clinical milestones and sales milestones, (3) in connection with the clinical milestones, Alexza has three post-approval clinical studies that are required to be completed by the FDA. One of the studies is a 10,000 patient observational study, which will take 2 to 3 years to complete, and the other two studies are pediatric studies. I assumed that the ADASUVE sales based milestones were all achievable, and the threshold levels or triggers at which these milestones would be earned were all based upon achieving the peak sales guidance that Alexza has already projected for ADASUVE sales in the U.S., and were based upon the current indication and label approved by the FDA. In addition, I assumed that because Teva will be paying for and completing all of the FDA required post-approval clinical studies for ADASUVE in the U.S., all of the clinical milestones in the Teva deal are also achievable and will be earned by Alexza.

The total of all of the Teva milestone payments over the 10-year horizon that I included in my valuation analysis was $235.0 million. I show the upfront cash payment of $40.0 million in Year 1. In Year 2, I only show a milestone payment of $10.0 million because I assumed that it will take more time for the sales uptake of ADASUVE to scale sufficiently to trigger a larger sales-based milestone payment, and it will take more time for Alexza to run the clinical studies and earn the clinical-based milestone payments. During Years 3 to 5, I project annual milestone payments of $20.0 million per year, and from Years 6 to 10, I show annual milestone payments of $25.0 million. You can see all of my Alexza revenue projections for ADASUVE on the spreadsheet below:

(click to enlarge)

Projection of Alexza's Expenses

The first expense that I projected was Alexza's required payment to Symphony-Allegro. Alexza has already paid Symphony-Allegro $10.0 million out of the $40.0 million upfront cash payment that Alexza received from Teva. Going-forward, Alexza will have to pay Symphony-Allegro 25.0% of the next $10.0 million ($2.5 million) in ADASUVE revenues (milestone payments and/or royalty payments) that Alexza receives, then after Alexza pays this $2.5 million payment to Symphony-Allegro, Alexza will only have to pay Symphony-Allegro 10.0% of all future royalty and milestone payments related to ADASUVE. Alexza does not have to pay Symphony-Allegro a percentage of any of the ADASUVE transfer price or manufacturing profits it receives, only the royalty and milestone payments. On the spreadsheet above, you can see that I have projected the Symphony-Allegro milestone payments for Years 1 through 10 based upon a rate of 25.0% of the next $10.0 million in ADASUVE milestone revenue during Year 1, then 10.0% for Years 2 through 10.

Based upon the guidance that Alexza gave related to research & development expense (R&D) and general & administrative expense (G&A) during the Q1 2013 earnings release conference call, I have projected R&D and G&A expenses for the next 10 years. Although, Teva will be conducting and paying for the ADASUVE post-approval clinical studies going-forward, I maintained R&D and G&A expense stable for Year 1, and I even grew both of these expenses through Year 10 because Alexza will be re-activating its new drug pipeline beginning with Staccato Alprazolam (AZ-002) and other potential new drugs in the near future.

For the interest expense projection, I assumed that Alexza will draw-down the $25.0 million promissory note from Teva that they signed as a part of the ADASUVE deal. Alexza has up to 24 months to draw down the $25.0 million, and the note bears simple interest of 4.0% per year. I assumed that Alexza will not start drawing down the Teva note until next year because they have already received the $40.0 million upfront cash payment from Teva, and on May 24, 2013, Alexza also received another $6.3 million from the Azimuth Opportunity LP common stock purchase agreement. I assumed that Alexza will draw down half of the note, $12.5 million, during Year 2 and the other half during Year 3.

For federal income expenses, I assumed that Alexza will not pay any federal income taxes because according to its Form 10-K for the year ended December 31, 2012, Alexza had a total of $286.4 million in federal net operating loss (NOLs) carryforwards. During the 10-Year projection period, I projected that Alexza will realize additional cumulative losses during Years 1 and 2 of about $19.6 million, so that would make the total NOLs of about $306.0 million. The total accumulated net profits for Alexza during Years 8 to 10 will be about $250.0 million, which is less than the NOLs.

Alexza DCF Valuation Analysis

I took all of Alexza's free-cash-flows for the next 10 years from the spreadsheet above and derived a value per share of common stock of $16.28 for Alexza. You can see this on the table below:

(click to enlarge)

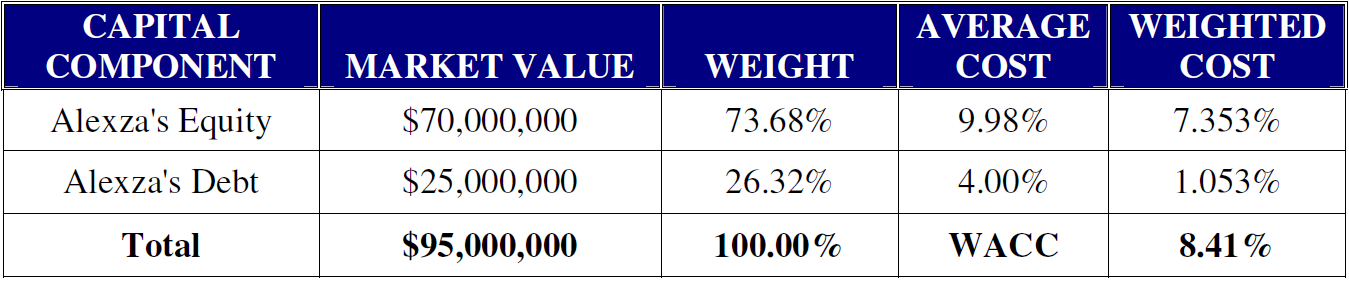

Two of my key assumptions in the valuation of Alexza was the discount rate and weighted average cost of capital (WACC) rate. If I use the capital asset pricing model (CAPM) to calculate the discount rate, I would use the following formula:

Re = Rf + B(Rm - Rf)

Re is the expected rate of return on equity, Rf is the risk-free rate, B is Alexza's beta, and (Rm - Rf) is the equity risk premium. I would use the current 30-year treasury bond rate of 3.23% as the risk-free rate (Rf). According to NASDAQ, the beta for Alexza is 1.25, and the current equity risk premium (Rm-Rf) is about 5.4%. Using these numbers in the above-referenced formula, I would get the following:

Re = 3.23% + 1.25(5.4%)

Re = 9.98%

I would use the following formula to determine the WACC:

WACC = Weight of Equity X Cost of Equity

+ Weight of Debt X Cost of Debt

I would substitute the market value of Alexza's outstanding shares of common stock (about $70.0 million) for Alexza's equity, and I would use the CAPM derived expected rate of return on Alexza's equity (9.98%). For the debt component, I would use the $25.0 million, 5-year Teva note, which bears simple interest at the rate of 4.0% per year to be Alexza's debt weight and cost of debt. All of these inputs would equate to a WACC of 8.41% for Alexza, as shown on the table below.

(click to enlarge)

A WACC of 8.41% for Alexza is also consistent with consistent with the WACC calculated by Wikiwealth. However, I wanted my valuation analysis to be more conservative, so instead of using a discount rate or WACC of 8.41% or 8.00%, I used a WACC of 10.00%. The higher the WACC or discount rate is, the lower the valuation will be.

Next, I projected a growth rate of 2.0% at terminal, after my 10-year time horizon. Then I calculated fully-diluted outstanding shares of Alexza's common stock by adding the following number of shares together:

- The total number of shares that Alexza reported as outstanding as of May 6, 2013 in their Q1 2013 10-Q, was 15,796,355 shares.

- I added 1,437,481 shares that were sold to Azimuth Partnership LP on May 24, 2013.

- I added 4,400,000 shares for warrants that were issued on February 23, 2012. The warrants were exercisable beginning February 24, 2013 at an exercise price of $5.00 per share, and these warrants do not expire until February 23, 2017.

Adding all of these amounts together, I calculated a total of 21,633,836 fully-diluted shares outstanding.

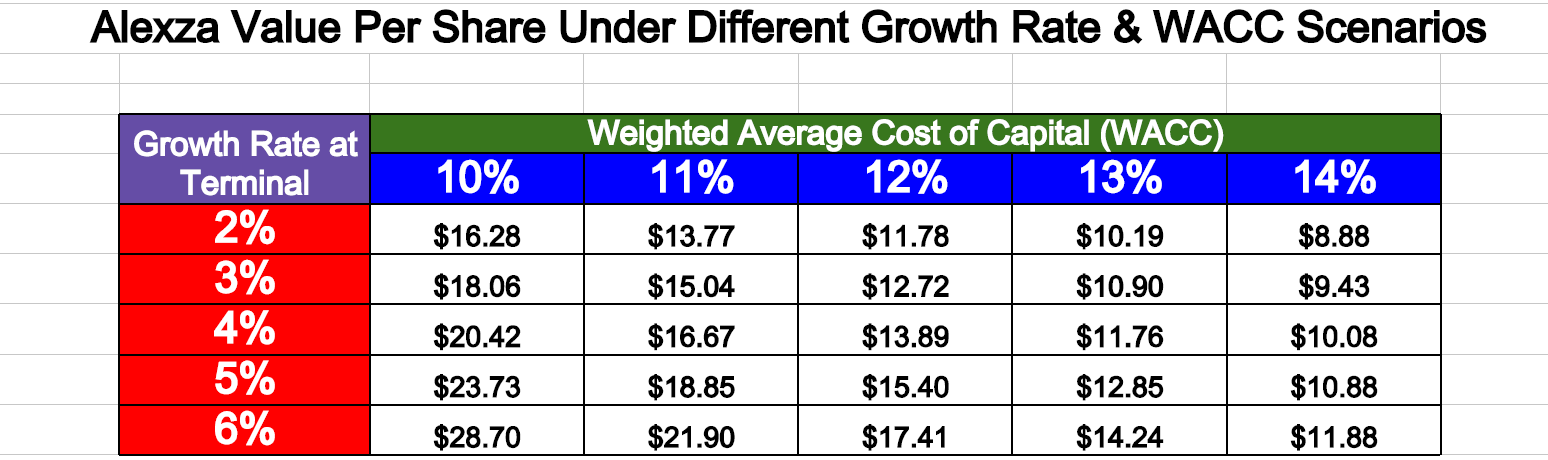

Sensitivity Analysis

I wanted to see what Alexza's valuation would look like if I changed the WACC and the growth rate at terminal. I was able to calculate the following values for Alexza by changing the WACC and the growth rate:

(click to enlarge)

As you can see, by varying the WACC and the perpetual growth rate after Year 10, and using the exact same free cash-flows, Alexza's implied stock value per share ranges from $8.88 per share up to $28.70 per share. However, I believe that Alexza's WACC should be 10.0.% or lower, and the values in the 10.0% column are more representative of Alexza's true value. That suggests a low value of $16.28 per share to a high value of $28.70 per share.

What Could Make My Valuation Too Low?

- Alexza and Teva are conducting post-approval clinical trials which could lead to an expansion of the ADASUVE label in the U.S. to include adolescent patients between the age of 13 to 17. If the ADASUVE label is expanded to include adolescent patients, this will significantly increase ADASUVE peak sales potential in the U.S.

- Alexza and Teva are conducting post-approval clinical trials which could lead to an expansion of the ADASUVE label in the U.S to include self-administered ADASUVE in the patient's home by the patient or by their caregiver. Currently, ADASUVE can only be administered in a hospital setting by a health care provider. If the ADASUVE label is expanded to allow patients to take ADASUVE at-home, this will significantly increase ADASUVE peak sales potential in the U.S.

- Teva has the right to conduct additional post-approval clinical trials of ADASUVE for potential new indications in neurological disorders. If the ADASUVE label is expanded to allow it to be used to treat new indications, this will significantly increase ADASUVE peak sales potential in the U.S., and it could also extend the patent life of ADASUVE beyond 2022.

- Alexza could finalize deals with additional partners to commercialize ADASUVE in other territories that are not included in the Grupo Ferrer territories and the Teva territory (U.S.). These potential territories could include: Canada, China, Korea, Japan, India, Australia, and Africa. If Alexza were to reach agreements with potential partners to commercialize ADASUVE in non-Grupo Ferrer and non-Teva territories, this will significantly increase ADASUVE potential milestone, royalty and manufacturing profit revenue.

- The Staccato delivery platform has been tested and proven to work with over 200 different drugs. Alexza is re-activating its pipeline, and it is possible that Alexza could submit new NDAs to the FDA, and Alexza could have other new drugs using the Staccato system approved by the FDA within the 10-Year time horizon covered by my valuation. If Alexza were to have additional new drugs using the Staccato delivery system approved by the FDA, this will significantly increase Alexza's potential milestone, royalty and manufacturing profit revenue.

- Teva has a new strategy that emphasizes New Therapeutic Entities (hereafter NTEs). NTEs are known molecules that are formulated, delivered or used in a novel way to address specific patient needs. ADASUVE is considered to be an NTE because it has a known molecule (loxapine) that is delivered in a novel way (inhalation) using the Staccato delivery system. The Staccato delivery system is a perfect NTE delivery system because it has been tested to work with over 200 different drugs. If Alexza and Teva were to agree to partner and/or collaborate on other new NTEs using the Staccato delivery system, this could significantly increase Alexza's potential milestone, royalty and manufacturing profit revenue.

What Could Make My Valuation Too High?

- The commercial launch of ADASUVE is poorly executed by Teva in the U.S., and/or by Grupo Ferrer in the E.U.

- The sales uptake of ADASUVE is significantly slower than projected.

- Alexza and Teva fail to complete some of the required post-approval studies.

Conclusion

Based upon my valuation analysis of Alexza, the implied value for Alexza's stock based solely on the value of ADASUVE is $16.28 per share. I used conservative key assumptions to derive this value. This value only considers the value of the ADASUVE cash-flows, and it does not add any value for: the Staccato delivery system, Alexza's new drug pipeline, potential ADASUVE sales beyond the current Grupo Ferrer and Teva territories, an expanded label to include adolescents, and an expanded label to include new indications.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.