Many believe that ATMs are one of the largest, technically driven innovations in retail banking in recent decades.

I see more Internetbanks, which have developed since 1995 and are now firmly established in the market.

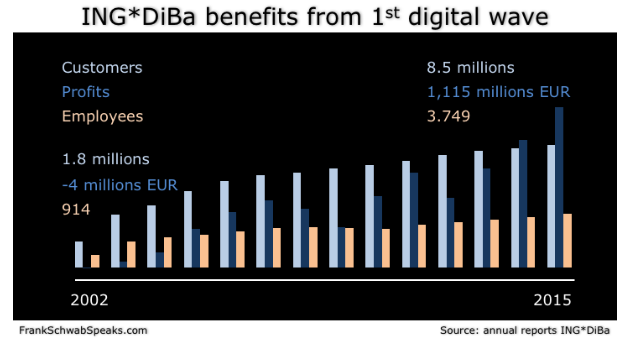

ING*DiBa alone has been able to attract around seven million new bank customers since 2002, to increase its own credit volume from EUR 4.6 billion to EUR 98 billion and to achieve a profit of more than EUR 1 billion in 2015. ING*DiBa has won the business of traditional banks and savings banks so far in the branch business. Successful drivers were among other things the concentration on few products, the highest possible process automation and outstandingly perceived customer service. Team! Bank, DKB, GLS Bank and ComDirect are further success stories of the first Internet wave in retail banking in Germany, as are the "Autobanks" of BWM, Mercedes and VW.

But, not all Internet-based retail banking business models of the first wave were successful. Online brokers such as ConSors, maxblue and DABbank could not establish a sustainably successful business model. Reasons for this are, in my view, a substantial failure in pricing. The online brokers had primarily driven price dumping, rather than differentiating themselves through customer service and user-friendliness compared to the traditional providers.

Today, we can experience the second wave of the Internet. We receive daily reports on FinTech start-ups, FinTech investments and FinTech cooperations. More than 400 FinTechs have established themselves in Germany over the past four years and offer superior products with superior user-friendliness and significantly better cost structures compared to traditional banks and savings banks.

For example, the crowdfinance company kapilendo was able to successfully carry out a 1 million euro financing in nine minutes and 23 seconds on a Saturday afternoon for the Berlin football first division Hertha BSC. The crypto currency Bitcoin has settled at a price of more than 800 euros and was the currency with the world's largest value growth in 2016. Hufsy.com offers a seamless user experience beyond banking for freelancers and small businesses. With N26 and O2/Fidor Bank, at least two pure-breed mobile banking providers are setting new standards in user-friendliness. At the same time, the robo advisory FinTechs cashboard and niiio promise highest transparency, simplicity and low prices in financial investment. And so far hardly noticed, the highly specialized FinTech's Mambu, Solaris Bank and Fidor with Cloud, API and platform offerings revolutionize the basics of the modern banking business.

is interesting because in this very special segment, Germany has now taken over the global leadership in innovation. In no other country, and no other financial center, is there such a wide range of applications that is already widely used.

FinTech - everything just hype? No, alone in 2016, more than $ 36 billion was invested worldwide in FinTech. The banking industry is now in the massive transformation that has been expected for many years, as the basic conditions have changed fundamentally. New technologies are mature, customer behavior has changed, and the growing regulatory requirements, as well as the interest rate trend, are going to be at a new level for the foreseeable future.

The FinTechs have already adjusted to this compared to the established banking service providers. This can be seen, for example, in the following KPIs. Some FinTechs achieve IT costs per user of less than 10 Euro per year and new customer acquisition costs of 8 to 25 Euro. This means that some FinTechs are soon on the way to the big social media and eCommerce players like Facebook and eBay. On the other hand, many traditional banks and savings banks still have IT costs per user per year and new customer acquisition costs of more than € 100 each. Such cost structures are now no longer competitive.

That is why traditional banks and savings banks are at a crossroads.

Either they adapt themselves very quickly to the new reality and radically renew their products, processes, IT and cost structures, or they will evolve into niche providers, pure infrastructure providers, such as the telecommunications providers, or disappear completely from the market. Successful in retail banking will be the financial services provider offering new products with a high degree of user-friendliness and additional customer value with new, highly efficient IT and process structures.

References:

https://www.linkedin.com/pulse/german-banking-crossroads-frank-schwab

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Your update on what’s going on in the Fintech space. Keep up-to-date with news, valuations, mergers, funding, and events. Sign up today!