Zinger Key Points

- The dollar and U.S. Treasury yields reach one-month highs, buoyed by robust U.S. economic data.

- Unemployment benefit claims drop significantly, hitting their lowest since 2022, signifying a tight labor market.

- Get 5 ‘Hidden Gem’ stock picks and daily rankings—now 60% off for Memorial Day.

The dollar and U.S. Treasury yields have reached highs not seen in over a month, driven by the ongoing resilience of the American economy, as evidenced by the release of generally better-than-expected data.

The U.S. Dollar Index (DXY), which measures the greenback’s performance against a basket of major currencies, edged slightly higher to approach 103.52 on Thursday. The yield on a 10-year Treasury Note, whose performance is tracked by the U.S. Treasury Note ETF UTEN, briefly reached 4.13%, hitting its highest levels since Dec. 13.

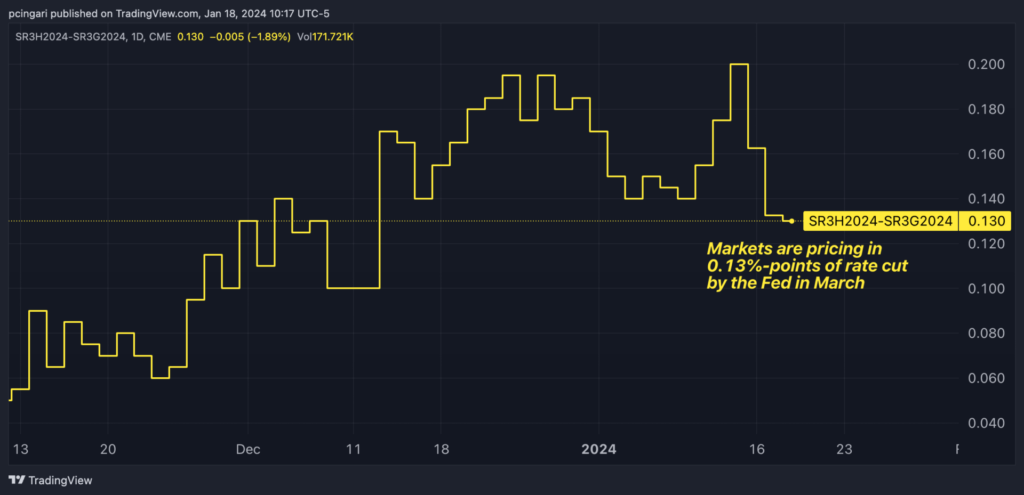

Market-implied probabilities of a rate cut by the Federal Reserve in March hovered at around 55%, according to CME Group’s FedWatch Tool, equalling to 13 basis points priced in. Market rate cut expectations are slightly up from Wednesday’s 50%, but significantly lower than the 73% seen a week ago.

Here are the key economic data points moving the markets on Thursday:

Jobless Claims Fall More Than Expected

During the week ending Jan. 18, the number of Americans applying for unemployment benefits saw a substantial decrease of 16,000, reaching 187,000. This figure represents the lowest level since September 2022, and it significantly came below market expectations of 207,000, as per data reported by the Labor Department.

Furthermore, continuing claims experienced a decline of 26,000 in the previous week, falling to 1,806,000, marking the lowest point since September 2022. This trend suggests that individuals who are unemployed are encountering relatively fewer difficulties in securing new job opportunities.

Why It Matters: These lower-than-anticipated jobless claims shed light on the persistently tight labor market in the United States. This development has raised concerns that the Federal Reserve might consider maintaining its current high-interest rate stance into the second quarter, if necessary, in order to address inflationary pressures.

According to Chris Zaccarelli, chief investment officer for Independent Advisor Alliance, a strong job market is positive for the stock market, dispelling the common belief that bad economic news is good for markets.

He noted that “the economy will continue to expand, and a recession will be averted this year as well,” adding that “pervasive pessimism and doubt about the stock market and the economy are contrarian signals and one of the best reasons to go against the crowd and remain fully invested.”

Building Permits, House Starts Surpass Estimates

In December 2023, building permits exhibited a 1.9% increase, reaching a seasonally adjusted annual rate of 1.495 million. This surge came after November’s figure of 1.467 million and exceeded market forecasts, which had estimated 1.48 million permits, according to preliminary estimates.

In contrast, housing starts fell by 4.3% on a month-over-month basis, reaching an annualized figure of 1.46 million in December 2023. Although this represents a decline, it still surpassed market predictions of 1.426 million. This decrease marks the first drop in four months, following a downward revision of a 10.8% surge in November, which had resulted in a figure of 1.525 million.

Why It Matters: Despite the monthly drop in housing starts, Jeffrey Roach, chief economist for LPL Financial, stated that falling mortgage rates are poised to stimulate demand for housing in the coming months. It is noteworthy that construction activity remains near pre-pandemic levels.

However, the limited supply of existing homes available for purchase may potentially drive buyers toward new construction. Consequently, investors may expect opportunities within the homebuilder sector throughout the year.

Philly Fed Manufacturing Activity Remains In Contraction

In January 2024, the Philadelphia Fed Manufacturing Index in the United States registered a positive change, increasing by 2.2 points to -10.6. While this marks an improvement compared to the previous month’s reading of -12.8, it fell short of market estimates, which had anticipated a reading of -7. It is important to note that this reading represents the 18th negative reading out of the last 20 months for this index.

Why It Matters: Not all sectors of the U.S. economy are firing on all cylinders, as manufacturing-related industries continue to grapple with a prolonged contraction. This situation is affecting stock performances, with sectors such as consumer staples, materials, and industrials, which are less reliant on services, consistently underperforming the broader market.

Photo: Shutterstock

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.