Shoppers flocked to gasoline stations and Internet retailers last month as retail sales rose for the first time since January, the government said early Friday. Sales rose overall, but not as much as expected, and stocks came under pressure in pre-market trading.

The 0.4% climb in April retail sales came as a relief after sluggish results in February and March, but the number wasn’t quite as robust as the 0.6% consensus Wall Street estimate. Gasoline sales rose by 14%, and “nonstore retail” sales climbed nearly 11%, the government said. The nonstore retail category covers electronic shopping, so the lesson seems to be that Internet retailers continue to outpace so-called “brick-and-mortar stores.”

General merchandise stores (which include department stores), sporting goods stores, and clothing stores all saw sales fall in April. The report comes right after a bunch of big department stores reported disappointing Q1 earnings results.

In other economic news this morning, the consumer price index (CPI) rose 0.2% in April, in line with analysts’ expectations. Producer prices announced yesterday topped estimates, but CPI didn’t indicate signs of any really worrisome inflation.

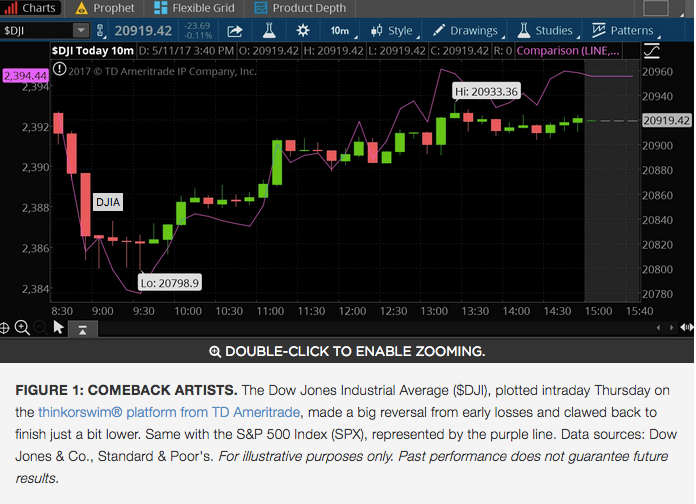

If you had to choose a single word to describe Thursday’s market action, it might be “resilient.” After the Dow Jones Industrial Average ($DJI) fell triple-digits early on after weak earnings results from Macy’s M, it clawed back the rest of the day to close just a little lower. The S&P 500 Index (SPX) also recovered from sharp early losses, bouncing back from an area near 2384 where some analysts had noted technical support.

However, weak results from J C Penney Company Inc JCP early Friday might pose a new threat to the markets. JCP missed Wall Street analysts’ top- and bottom-line expectations, and same-store sales fell 3.5%. JCP was just the latest department store chain to report soft earnings. After the close yesterday, Nordstrom JWN reported earnings and revenue that topped analyst’s estimates but lower-than-expected same-store sales. The same-store performance could be the reason for the stock’s weakness in pre-market trading. However, sales at the company’s lower-priced Nordstrom Rack climbed appreciably and comparable sales rose.

The consumer discretionary sector sank Thursday, finishing with a 0.6% loss to be the worst performing sector. With JCP down about 5% in pre-market trading Friday, it looks like consumer discretionary might come under more pressure today.

The financial sector has also had a downturn over the last week and performed rather poorly Thursday, in part due to worries about a flattening of the yield curve. A flatter yield curve tends to put pressure on bank stocks, which can make more money when they loan funds at higher long-term rates.

Meanwhile, the U.S. dollar has had a good week and traded near three-week highs early Friday. Signs of a strengthening U.S. economy and rising interest rates seem to be giving the dollar a lift, and expectations have grown for a Fed rate hike in June, which would likely be supportive for the currency.

Volatility swung up early Thursday, with the VIX rising above 11 for a time, but fell back below 10.8 early Friday. There’ve been a lot of attempts to explain why VIX continues to be so low, including plain old complacency. But the real reason could be that the market just hasn’t had a big catalyst lately to make any huge moves one way or the other.

Pleasant Employment Tidings Continue

Last week’s April employment report showed job creation bouncing back from a disappointing March reading, and the positive jobs news continued Thursday with weekly jobless claims falling to 236,000. From an overall standpoint, continuing claims stood at 1.918 million, the lowest since President Reagan was still in office in early November 1988. Combined with the Job Openings and Labor Turnover Survey (JOLTS) report earlier this week and the April employment report, the news from the labor market all looks quite strong, a potential sign that the economy continues to steam along.

Gunning for 2400

The S&P 500 (SPX) ran into resistance this week at the psychological level of 2400. Big numbers like that might not mean much in the great scheme of things, but it’s arguable that they do represent a challenge for the indices to go through, and we’ve seen that again and again over the last year. Recall how many attempts it took for the Dow Jones Industrial Average ($DJI) to push through 20,000. Sometimes when an index does finally break through and close above a big round number, buyers come to town.

Checking Valuations

Some pundits say the stock market is over-valued, and it’s true that the SPX’s price-to-earnings ratio (P/E) was at a relatively high 18.4 as of mid-week vs. projected 2017 earnings. That’s about where P/E has been for some time, with strong Q1 earnings helping prevent it from rising further. Those same strong earnings might be driving more investor interest in the stock market, which could keep valuations high. Additionally, interest rates remain relatively low, meaning investors who want to grow their money don’t have great options in the bond market. That also might be drawing them toward equities, with the result that valuations stay up. Should investors worry about the high P/E ratio? It’s good to keep it in mind, but with earnings so strong and the economy sending positive signals, it might not be a major concern as of yet.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.