Monthly Depth Report – July 2023

Mid-Year Review Of Key Issues

We’re taking advantage of the summer lull to bring you more detail on some of the key issues that will affect the investment landscape in the next few months. That means a macro focus right now, and next month, we’ll be able to address earnings from most companies we find interesting. Plus, what’s wrong with young people these days? I’ll report on a day with the DKI Interns.

Big Institutional Firms File For Bitcoin ETF

When DKI recommended buying Bitcoin (CRYPTO: BTC) a couple of years ago at half the current price in dollars, part of our thesis was the coming institutional acceptance of the asset. We hypothesized that even small percentage allocations from firms managing trillions of dollars would overwhelm Bitcoin trading where the current issuance is about 900 coins a day. With fixed supply and a deflationary issuance schedule, the only way the market can adjust to greater demand is higher prices.

Within the past month, BlackRock, Bitwise, Invesco, Deutsche Bank, WisdomTree, and Fidelity all filed for spot Bitcoin exchange traded funds (ETFs). The SEC is asking questions, but doing so in a way that’s providing these companies a road map to address regulatory concerns. While many of these firms had made negative comments on Bitcoin in prior years, the lure of more fees changed their minds. Many investors want to hold Bitcoin in a brokerage account and don’t want to have to buy it off of an exchange and figure out how to self-custody. An ETF is perfect for their needs.

It is our belief that the SEC will approve some or all of these applications which will have interesting implications for the Grayscale Bitcoin Trust (OTC:GBTC). This is a closed-end fund that enables investors to buy an asset linked to Bitcoin’s spot price in their brokerage account. The issue with $GBTC is it is a closed-end fund. This means that shares can’t be destroyed and there is no way to match the number of Trust shares with current demand. As a result, GBTC has been trading at a large discount to net asset value (NAV). That means you can effectively buy Bitcoin at a discount right now.

The fund was trading at a discount of between 40% and 50% last month. When I saw the big institutions applying for their own Bitcoin ETF, I thought it was likely that Grayscale would win approval, and that this would enable the Trust to buy back shares and retire them. This would cause $GBTC to trade at NAV again.

DKI was quick to respond to this and re-recommended GBTC in the low/mid teens. The discount to NAV has collapsed to just over 25%. As of this writing, each share of the trust is trading at $19.99. That’s a return of just under 40% in a month for DKI subscribers. For those of you considering joining us as premium subscribers, I can’t promise you that we find these opportunities every week, but you don’t need a lot of them to make the cost of a subscription worthwhile.

Still a big discount but it’s been cut almost in half. Chart from YCharts.

Finally, for those of you who prefer to self-custody and take control of your own Bitcoin, you can use our step-by-step self-custody guide.

Mixed Economic Data – Still More Rate Hikes

Last month, we wrote this:

DKI has been highlighting inconsistent economic data since last November. However, recent news has put that trend on steroids. The ISM Manufacturing Index and the Purchasing Managers’ Index are both showing contraction/recessionary indicators. Demand for goods is weak.

Lumber pricing is down, but housing prices haven’t crashed yet despite higher financing costs. However, services inflation and employment data are indicating huge demand. There are more than 10MM unfilled jobs in the US. The unemployment rate is still well below 4%. Wage growth continues although at a pace that falls short of inflation. These are all issues we’ve been exploring most weeks in our 5 Things to Know in Investing piece and add additional detail in posts for paid subscribers. While the investing environment is complicated, there are some stocks that we think will benefit from existing conditions.

July provided more of the same confusion. Manufacturing indexes tended to be weak. The consumer continued to spend. Services spending and inflation remained high, but now there are indications of increasing demand for goods. Finally, the employment situation remains strong.

Look at the graph below:

The most recent reading was an increase of just under half a million jobs which was about double the estimate. Some of that is people getting second or third part-time jobs, but either way, the country is definitely back to work.

The second graph also shows a strong labor market with an increase of over 200k jobs. The unemployment rate has fallen back down to 3.6%. Even though this second data set indicated job growth was below expectations, there is enough economic strength here to ensure the Federal Reserve follows through on its plan to raise rates again soon.

Right now, the data everyone is seeing indicates we haven’t hit the expected recession yet. If Powell can manage a soft landing here, it would be a remarkable achievement. We still think the Federal Reserve should be disbanded and that the market can and should set the price of interest. Despite those feelings, it would still be a great outcome so while we remain team #EndTheFed, we’re still cheering for Powell to get it right.

Higher For Longer

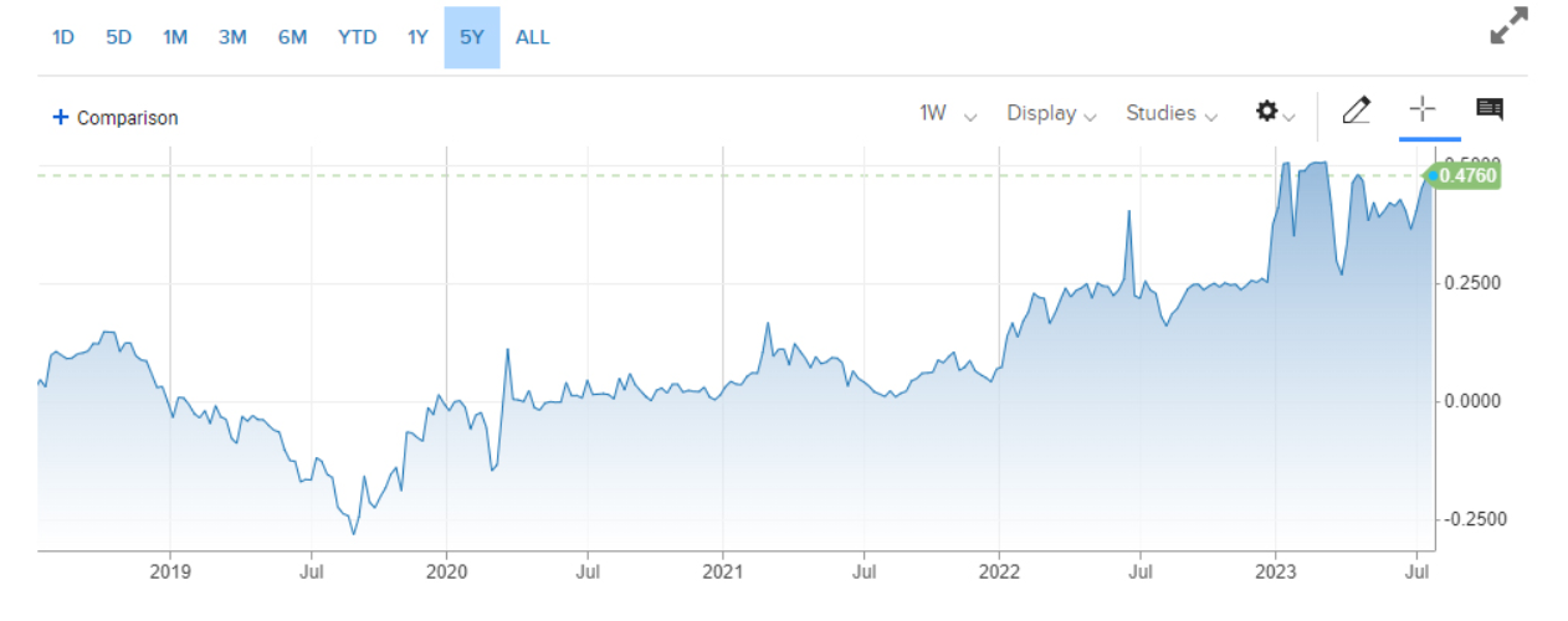

Over a year ago, the “pivot people” started calling for the Fed to pivot to lower rates. At the time and for the past year, DKI has said that we were nowhere near a pivot and that we expect the Fed to continue raising. Shortly afterwards, Fed Chairman, Jerome Powell, started telling people that rates would be “higher for longer”. Despite that, people continue to call for lower interest rates. There are many ways to address this, but the best is this chart:

Real interest rates (the fed funds rate less the rate of inflation) has finally gone back above zero. Most savers are still falling behind inflation and the ones with the highest interest rates are still returning about 1% after inflation.

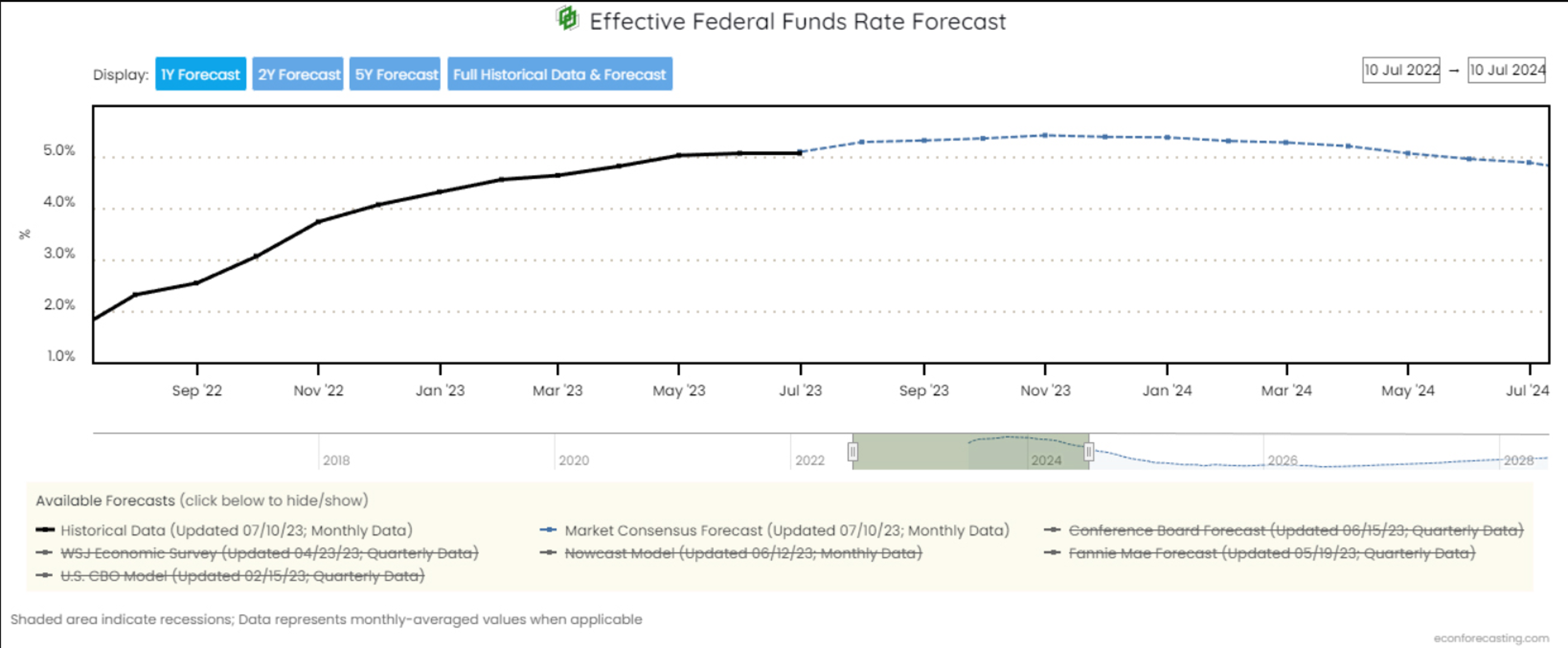

What’s been interesting to us has been the way the market has started to match DKI’s expectations, but without a corresponding move in the equity markets. Let’s look at this chart of expectations for the fed funds rate:

I grabbed this chart from Econforecasting in April. At the time, it showed expectations for over 1.5% (150bp) of Federal Reserve easing over the next year. DKI said that wasn’t going to happen. Here’s the new version:

Notice how much more flat that line has gotten and how there’s no expectation of rate cuts in the next year. The market expects the fed funds rate to increase and then to come back to current levels in the next year. This is a more reasonable approach, but it brings up an interesting question. If part of the market is starting to believe Powell’s higher for longer speech, then why are the equity markets continuing to rise?

There are also reasons to believe that inflation hasn’t bottomed. While the market was encouraged by the much lower 3% June CPI, we’ve now passed the highest CPI readings from last year meaning that comparisons going forward will be more challenging. In addition, there’s a huge adjustment to health insurance inflation that’s making the CPI look lower than the inflation Americans are actually experiencing. That adjustment ends in September and will likely go from a tailwind to a headwind. Finally, the main reason June inflation was much lower was a decrease in energy costs from the highs of a year ago. It’s unlikely we’ll see continued decreases of this magnitude going forward. We wouldn’t be surprised to see the CPI tick up later this year. Much of that prediction will depend on future housing prices which have held up much better than most people (including us) expected given the increase in mortgage rates.

Is The VIX Lying To Us?

The VIX is an index that measures market expectations for volatility in the S&P 500 over the next 30 days. The index tends to have a skew in it because investors are much more concerned about downwards volatility than upwards volatility. As a result, we’ll typically see the VIX rise when the stock market falls and fall when the market rises. This is why it’s often referred to as the “fear gauge”.

As I write this, the VIX has fallen below 14. That’s a low reading by historical standards. There was a period during the last decade when the VIX traded around or below 10. Let’s examine what’s happening now:

Inflation is coming down but is still well above the Fed’s 2% target. Core inflation is just below 5% and services inflation is above 6%. The Fed believes they have more work to do and I’m in agreement with the market consensus that they’re going to keep raising rates.

Recession is a real fear. While the economy and corporate earnings have held up better than many including DKI expected, the yield curve remains negative which has been an accurate predictor of recessions.

Japan is facing a potential sovereign debt default. The world’s third largest economy has entered Ponzi scheme territory. In order to pay the interest on the debt, they’ll need to print more yen. It’s a negative when countries like Greece or Argentina default. A default from a major economy would move markets. More on Japan later in this letter.

Ukraine is still at war with Russia. After more than a year of fighting, Russia is unable to fully occupy the country and Ukraine is unable to fully repel the invasion. The US and some European countries are providing Ukraine with money and weapons. Several countries are still trying to admit Ukraine to NATO which would then obligate all treaty countries including the US to enter a hot war with Russia. Even the most dedicated Ukraine supporters should be concerned about the possibility of uncontrollable consequences of war with one of the world’s great nuclear powers.

China is speaking more openly and aggressively about retaking Taiwan. While most Taiwanese prefer to remain an independent democracy, it is unlikely that there is any argument to be made that would persuade the CCP (Chinese Communist Party) that Taiwan will not eventually be brought under Chinese control. The US has implied it would support Taiwan in the event of a Chinese invasion, and a Joe Biden live-microphone gaffe indicated the US has committed to defending Taiwan. The latter is not accurate. Taiwan is the largest supplier of the world’s best computer chips and the US gets most of its pharmaceuticals from China. Until the US re-shores those supply lines and a few others as well, any open conflict with China would have significant unintended consequences.

Market breadth is historically low. Despite large first half gains by the S&P 500 this year, almost all index gains came from 7 mega cap tech firms. The other 493 companies in the index have barely moved in aggregate this year. Low and falling breadth has historically tended to be a sign of an unhealthy market.

Valuations are unusually high. Despite low breadth, the forward price to earnings multiple on the S&P 500 has gone above 20x. That’s something we’d expect to see with the current low VIX, but is at a level where there’s risk. Typically, when valuations get this high, there’s reason to believe we’ll have low risk and high returns in the near future. The length of this list argues that future conditions may not be as positive as many hope.

Budget deficits remain huge. Despite months of public arguing between Congressional Republicans and the White House, both sides agreed to a spending plan that would increase the on-balance sheet debt of the US by $4 trillion over the next two years. That’s a huge number and will be financed by more currency printing. As we’ve seen over the last couple of years, this level of currency creation leads to more inflation.

This will be $35 trillion at the next Presidential inauguration – and ignores $200 trillion of off-balance sheet liabilities.

This year’s run up in the market indexes means most investors are ignoring the above list of potential issues. It’s highly unlikely that everything listed above becomes a problem for the market. However, if only one or two of these issues start gaining attention, it would make a VIX reading of under 14 look very low. As noted above, if the market gets more nervous or fearful, the VIX will rise and the S&P 500 will fall.

People Are Dismissing A Potential BRICS Currency Too Quickly

There’s a big argument happening in the financial community right now regarding the status of the dollar as the world’s reserve currency. The BRICS countries (Brazil, Russia, India, China, and South Africa) are expanding their coalition which now includes more than half the population of the planet. Those countries are actively looking to save and trade in a currency other than the US dollar. They are also openly talking about creating a new gold or commodity-backed currency to compete with the dollar.

Doomsayers are saying it’s “game over” for the dollar. Supporters are insisting that no one would trust a currency backed by Russia and China and trade in a non-dollar currency isn’t realistic. DKI thinks the most likely outcome is continued erosion of the dollar’s use as the world’s reserve currency as opposed to an event that results in a quick change in status. We also think people are too quick to dismiss the possibility for a BRICS competitor.

We’ve written extensively on the petrodollar before and it’s effectively dead now. The Saudis believe the White House has violated the agreement to provide military support and they have also expressed open distain for Joe Biden. As a result, Saudi Arabia has started to allow other countries to pay for oil in currencies other than the dollar.

In addition, the BRICS coalition includes the two most populus countries in the world (China and India), and two of the three largest oil and gas producers (Saudia Arabia and Russia). China, Russia, and India all have huge gold reserves, and China is the largest producer of many other rare commodity resources. It’s easy for Americans to say that no one will trust the Russians or the Chinese, but more than half the population of the world are actively looking to trade in something other than dollars.

When it comes to stewardship of the reserve currency, the US hasn’t always been a reliable trustworthy partner either. Rosevelt forced all US citizens to sell their gold for dollars and then immediately devalued the dollar. Over the following decades, the US printed paper dollars far in excess of its gold holdings forcing Nixon to close the gold window in 1971. Every country in the world that was holding dollars in 1971 had been told those dollars were exchangeable for gold. One day, that was no longer true.

Since then, Congress has continued to overspend and through every Presidential administration (Democrats and Republicans) debt continues to grow. The US has expanded the money supply debasing the currency. This was never sustainable:

As the US created dollars, the value of the dollars held by others decreased.

As the supply of dollars grew, the value of dollars held by others was debased. Other countries don’t like this dynamic, and to make things worse, these countries are affected by the actions of the Federal Reserve. When the Fed changes interest rates, it affects the relative value of the dollar and changes the price of oil in other countries’ local currency. This is not ideal if you want to import energy which every country on the planet does. Even friendly nations in our hemisphere like Argentina have started to conduct trade in currencies other than the dollar. The trend might have been started by China, Russia, and the Saudis, but other countries are joining.

This translates to manipulation of the currency. Some countries want to insulate themselves.

Finally, as part of the anti-Russian sanctions, the US confiscated the dollar reserves of Russia. On the surface, this seemed like a good way to prevent the Russians for using that money to conduct war against Ukraine. The problem is that it communicated to the rest of the world that the US could and would confiscate the dollars of a country not in the good graces of Washington DC. That’s a problem when control of the government changes hands every 2-6 years and our foreign policy is inconsistent from one administration to the next. It’s ok to be against the Russian invasion of Ukraine and to see that our response hurt the value of the dollar as a reliable reserve currency.

The trend we’re forecasting is consistent with the long-term trend as well. This graph from the IMF shows the dollar’s share of the market falling from 71% to 59% between 1999 and 2021.

The most recent data shows that the dollar’s share has fallen to 55% in the last two years. Whether BRICS succeeds in solving the significant problems inherent in creating a new currency or not, the dollar has been losing share for decades and the rate of decline is accelerating.

Is The Federal Reserve Going To Crash Japan?

DKI has written and spoken extensively about Japan’s financial problems. In a piece titled “Japanese Debt – We’re Taking a Victory Lap,” we provided links to our predictions that the Bank of Japan would eventually have to capitulate to market demands for higher rates.

10 Year Japanese government bond yield. Graph from CNBC.

Japan’s problem is straightforward. Its debt is more than 250% of GDP. The reason they’ve been able to do this is because Japan has had the yield on its debt of around zero for years and at times, have sold bonds with negative yields. One way they’ve done this is by buying their own debt. There were entire weeks last summer where all trading in Japanese bonds were done by the Bank of Japan. To say this is a manipulated market is an understatement.

Last year, when the US Federal Reserve raised interest rates, people sold Japanese yen and bought dollars to take advantage of the higher yield in the dollar. That selling pressure dropped the yen from 115 to the dollar down to 150. That’s a 30% devaluation in under a year which is an unheard of move in foreign currency markets, particularly when we’re talking about the world’s 3rd largest economy.

This currency decline is a problem when you need to import goods.

Japan is an island nation with few natural resources and very little energy. As the dollar strengthened against other currencies, the price of oil rose. The cost of oil in yen went up even more. The only thing the Bank of Japan can do to keep the yen from falling is to raise interest rates. The problem is that with debt levels so high, any significantly positive interest rate will cause a massive budget deficit. The only way the Japanese can pay the higher levels of interest is to print more yen. That leads to inflation and either a weaker yen, or the Bank of Japan will need to raise interest rates even more. Play that out for a few rounds and you can see why we call it a debt death spiral. Any fix to the problem causes more of the same problem.

Given that the Federal Reserve has indicated it plans to raise rates twice more this year and that it is not planning on lowering any time soon, that’s going to put more pressure on the yen and exacerbate financial problems in Japan. We don’t expect Powell to care about this as he’s focused on getting inflation in the US down. There’s an old unfortunate saying that the dollar is our currency, but it’s your problem. This is another reason more countries want less exposure to the dollar.

What’s Wrong With Young People These Days?

Last month, I had the opportunity to spend a day with most of DKI’s former and current interns here in Westport, CT. Over lunch, each took a turn talking about how they got their current jobs. Every single one of them has found great first jobs with big financial firms. They’re succeeding. This is both outstanding, and for anyone who’s had the opportunity to meet these young people, not at all surprising.

What makes their success even more satisfying is that only one of them went to an Ivy League school. They all had similar stories of how they networked aggressively and pushed persistently and creatively to get the attention of the large firms who don’t recruit at schools like Hofstra and Rutgers. Their stories reminded me of the great former Chairman of Bear Stearns, Ace Greenberg, who used to recruit people with “PSD degrees”. Ace wanted to hire people who were Poor, Smart, and had a Deep desire to become rich. This was a great example to current intern, Tristan Navarino, who comes to us from the excellent and under-rated finance program at the College of Charleston.

Later, over scotch and cigars, the conversation strayed into politics, finance, good scotch vs the bad vodka they drank in college, and proper business etiquette. People keep telling me this generation is fragile, but I see the DKI Interns eagerly accepting criticism because they want to improve. I’m constantly informed that young people today are lazy, but all of these Interns work long hours and are driven to succeed. I keep hearing about a sense of entitlement, but the most common question I’ve gotten from them is “what else can I be working on now”. Many say they’re self-absorbed, but every one of them has displayed polite etiquette in their interactions with me, with our clients and subscribers, and with the DKI Board of Advisors. Finally, even though it’s early in their careers, several of them have had setbacks related to conditions in finance right now (not their performance or conduct). They’ve demonstrated strength of character and resilience.

It's natural to worry, but the kids are alright. And regarding this particular group of young people, I’m proud of every one of them.

Time To Wrap It Up For This Month

We’d like to thank you for reading this letter and to welcome our new subscribers. The last couple of weeks has represented the largest premium subscriber growth in DKI history. Much of that is due to new member of the DKI Board of Advisors, Mish Shedlock, who was kind enough to highlight our research on his excellent blog, MishTalk. I’m grateful for your time and attention and that we’ve gained the trust of long-term subscribers. For those of you who see the value in our deep-dive analysis, we invite you to support us here.

DKI has a partnership with Tidal (@leadlagreport on Twitter). If you’re a financial advisor with more than $50MM under management, please reach out to us so we can arrange for you to get a premium subscription to Deep Knowledge Investing at no cost to you through Tidal. Michael Gayed runs the program, has been a great partner and friend, and is an expert on conditions-based investing. A chat with him and a subscription to DKI both provide great value.

If any of you have questions, concerns, or thoughts regarding issues we should address in a future depth report, please feel free to reach out to me at IR@DeepKnowledgeInvesting.com. If you think a friend, RIA, family office, or portfolio manager would be interested in this monthly commentary, please feel free to pass it on to them. Also, if you send this letter to more than 5 people, please get in touch and let me know.

Thanks for being part of Deep Knowledge Investing,

Gary Brode

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.