Logan Mohtashami, Benzinga Contributor

Logan Mohtashami, Benzinga Contributor

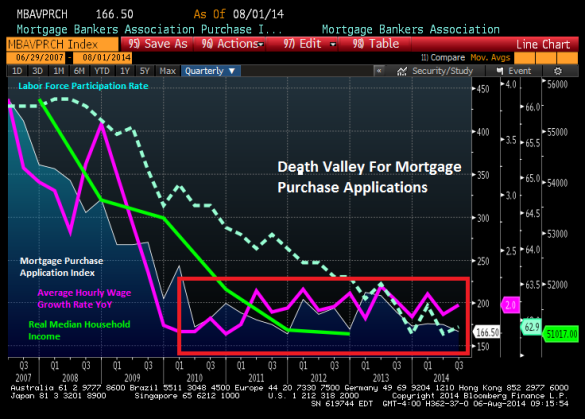

Simply put, the lack of recovery in housing demand is directly related to the a lack of recovery in real median income and growth in year over year average hourly wages. Yet many have failed to recognize how important wages and liquid assets are to creating real demand in the housing market. This, in spite of the preponderates of evidence presented to us from the likes of the distinguished and insightful Professor Anthony Sanders who has provided pictorial analyses of this issue, such as the chart below.

Three other important indicators, which typically drive an increase in home purchases, rising rents, rising housing inventory and lower mortgage rates, in this climate seem to have no effect – signaling a fundamental softness in the housing market in 2014.

- Rising rents: Even with rents consistently rising in most markets demand for housing from the mortgage buyer remains soft. The buying a home is cheaper than renting thesis sounds good, but didn’t work out too well in this cycle. Mortgage buyers have been below historical norms through out this housing cycle.

- Rising Inventory: Even with more homes on the market this year than last year, demand for housing from the mortgage buyer & the cash buyer has been less year over year. On a positive note we are seeing a cooling off on price gains and this is a good factor for the housing market, not a bad one.

- Lower Mortgage Rates: Even with mortgage interest rates falling from Jan 1, 2014, demand for housing from the mortgage buyer has been negative year over year all year long. The 10 year is yielding a whopping 2.34% as of the close of August 15, 2014. We have taken back the Taper Tantrum of 2013, but with home prices still rising the total cost of a home is still higher even with mortgage rates being the same.

When three economic factors that have historically driven buyers into the market are having little to no effect, one must suspect a significant change in the economic fundamentals. Low wages, a buildup of household debt and a lack of liquid assets combined with increasing purchase prices for homes means many if not most Americans cannot afford to buy. Until wages grow, liquid assets get built up and home price gains cool down, it’s going to be a long slow climb for the housing market.

As I discussed in the recent article published in Origination News, lending standards cannot be blamed for the soft housing. We simply do not have enough qualified home buyers – ie those with sufficient income for both the down payment and the monthly mortgage expense plus tax and insurance.

In a recent television interview with CNBC, I reiterated this point, emphasizing that the weakness in housing is due to a lack of income – not lack of credit availability. Starts at 8:55 into the show

http://nbr.com/2014/08/14/nightly-business-report-august-14-2014/

If you want a strong housing market you need Main Street America to have the capacity to own the debt of housing. The housing market must be less reliant on cash buyers and the wealthy. It needs a big dose of Main Street America participation to see year over year growth in existing home sales again. For that to happen, it will require more income & liquid assets and not easing of lending standards.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.