Microsoft MSFT recently released its 2014 10-K, and as I promised the StockTwits community, here’s an in-depth analysis of what our analysts found digging through the footnotes. MSFT currently earns our Neutral rating, but if new CEO Satya Nadella can halt the company’s declining return on invested capital (ROIC), the stock’s valuation is cheap enough to make it intriguing.

Declining ROIC: Apple 2.0

I am long-term bearish on Apple AAPL due to my expectation that its sky-high ROIC, which peaked at over 300% in 2011, will regress to the mean. My conviction in this bearish thesis is affirmed by the fact that MSFT is in the late stages of a similar regression that began in 2007.

MSFT’s ROIC peaked at 159% in 2006. Other than a brief bounce in 2010-2011, its ROIC has steadily declined since then, down to 56% in 2014. Given this data, it’s no surprise that MSFT lagged the S&P 500 between 2007 and 2013. However, so far in 2014 MSFT has gained 15%, nearly tripling the returns of the S&P 500.

There are two potential bull cases to support MSFT’s surge this year. One is based on short-term numbers and misleading, but the other is based on long-term strategic initiatives that support a much higher valuation.

The Flawed Bull Case: Earnings Growth in 2014

Some investors might be tempted to look at 2014’s numbers, which show 12% revenue growth and improving earnings per share, as a sign that MSFT is already turning its business around. However, these numbers are misleading.

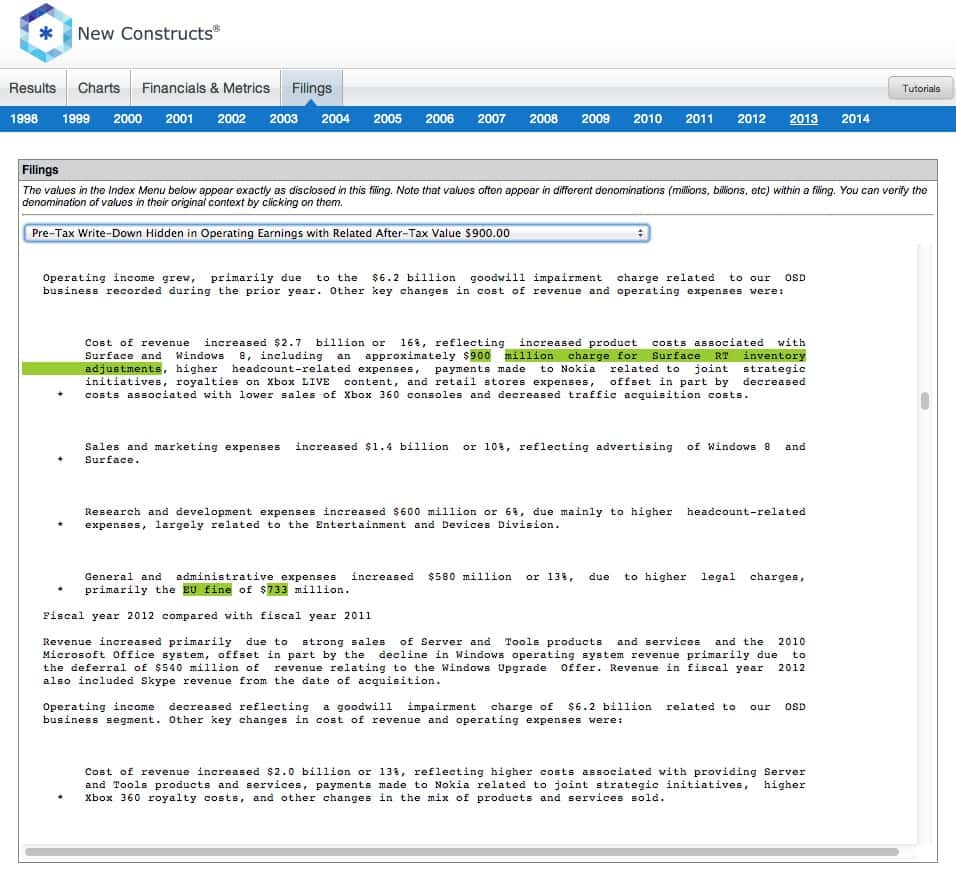

For one, two significant non-operating expenses artificially depressed MSFT’s accounting earnings in 2013. MSFT paid a $733 million fine to the EU for an antitrust violation and took a $900 million write-down on its Surface RT inventory in 2013, two non-recurring charges that made 2014 look better by comparison.

If we remove the impact of these unusual expenses, we see that MSFT earned an after-tax profit (NOPAT) of $22.9 billion in 2013, rather than the $21.8 billion it reported in GAAP net income. We also see that NOPAT actually declined by 3% in 2014, rather than the earnings growth that was reported.

Additionally, MSFT’s earnings tell investors nothing about the increase in invested capital, the denominator in our ROIC calculation. The Nokia acquisition added ~$8 billion to the firm’s capital base, but there was another big item that investors would not find unless they went digging through the footnotes.

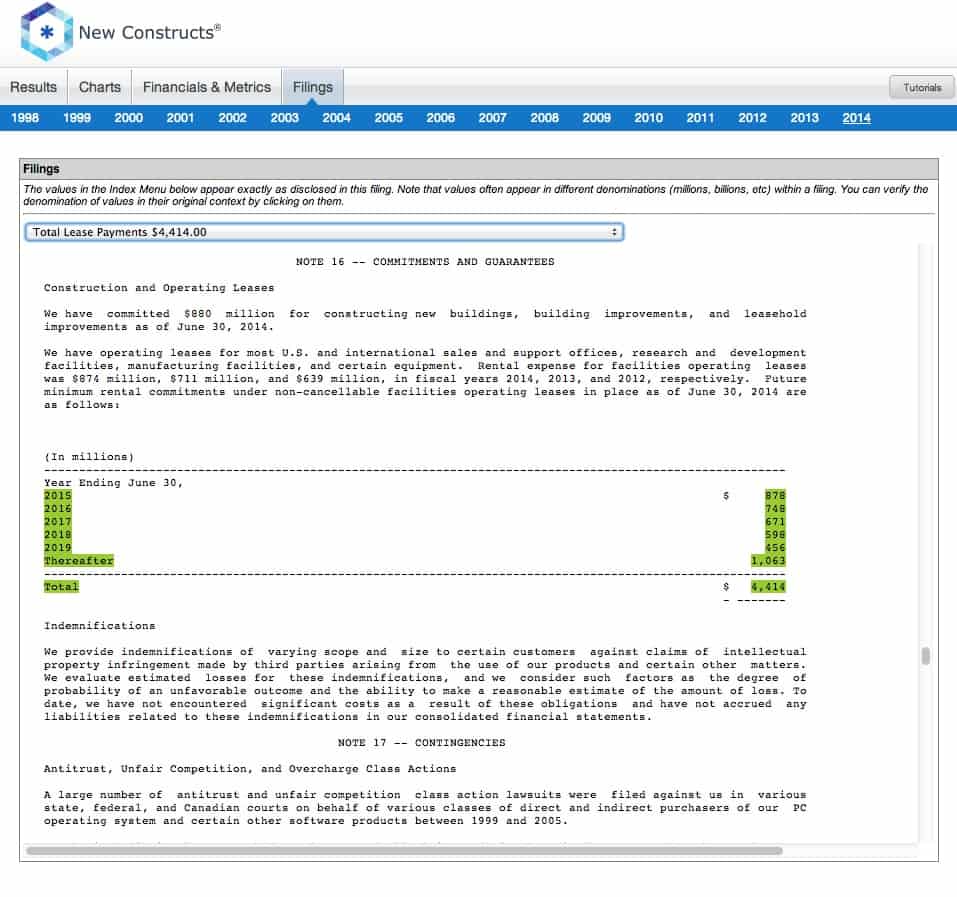

MSFT’s off-balance sheet debt increased to $3.8 billion in 2014, up from $2.2 billion a year ago. These leases can only be found on Page 87 of MSFT’s 2014 10-K.

When we make these adjustments, we find that MSFT’s average invested capital for 2014 (which accounts for the fact that the Nokia investment occurred near the end of the year) increased by $3.2 billion from $36.4 billion to $39.6 billion. Lower NOPAT and higher invested capital means a lower ROIC, 56%, vs. 63% a year ago.

Don’t be fooled by the growth you see on the income statement. MSFT’s economic profitability continued its long-term decline in 2014.

The Plausible Bull Case: ROIC Stabilizes Under Nadella

Nadella has only been CEO at MSFT for six months, but already he has made waves by announcing a major restructuring plan that will eliminate 18,000 jobs over the next year. In particular, Nadella plans to focus more attention on MSFT’s software services, especially its cloud products, while decreasing investment in devices. Roughly 12,500 of the layoffs will come from Nokia.

While I’ve been bearish on many cloud stocks, I like this strategic shift for MSFT. Unlike small cloud companies, MSFT has great name recognition already and can sell its cloud products to existing customers without spending an inordinate amount on marketing. MSFT was able to more than double its Commercial Cloud revenue in 2014, from $1.3 billion to $2.8 billion, while actually shrinking its advertising budget by 12%.

Nadella’s renewed focus on commercial software should spur growth opportunities without requiring the same level of investment that went into the company’s mostly underwhelming devices efforts. The layoffs over the next year should also help increase MSFT’s pre-tax profit margins, which declined to 32% in 2014, its lowest level in a decade.

MSFT’s days of earning triple digit ROIC’s are over, but its significant advantages in scale, brand recognition, and expertise in commercial software make it plausible that Nadella could halt the company’s declining fundamentals and stabilize ROIC at ~55% going forward.

Valuation Leads to Opportunity

Unsurprisingly, due to MSFT’s declining profitability, it has traded at a discount to its economic book value (EBV), or the no growth value of the business for the past six years. I’m always interested in companies that trade below their EBV, especially an industry leader such as MSFT.

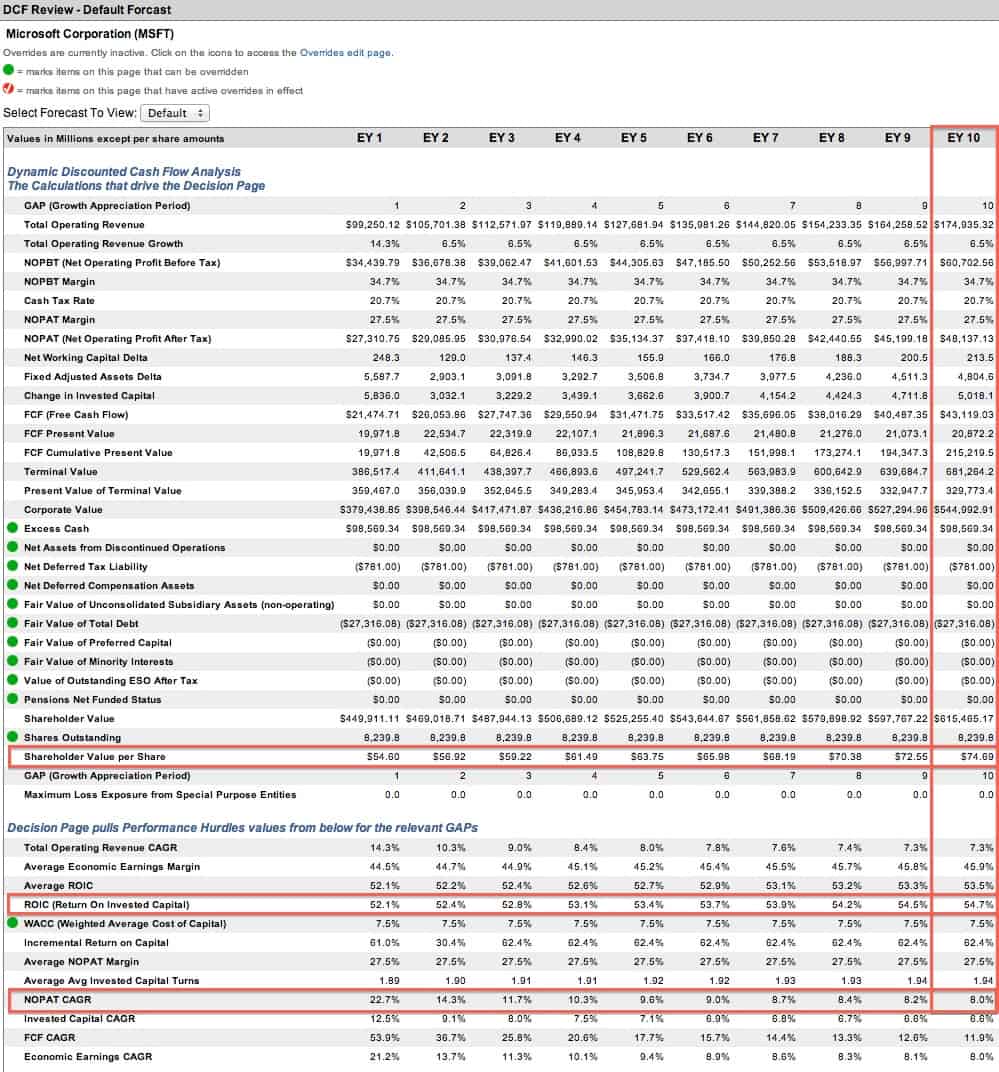

While ROIC continues to decline, I’m not going to be a buyer of MSFT, but if ROIC stabilizes the stock is a great value. If MSFT can maintain an ROIC of ~55% over the next 10 years while growing NOPAT at 8% compounded annually, the stock has a fair value of ~$75/share.

Due to its cheap valuation, MSFT has had my curiosity for a while. Now, with the dramatic moves Nadella is making to improve long-term profitability, it has my attention. If ROIC continues to decline, MSFT could be in trouble, but if it levels off at 55% or so, the stock is a great long-term value.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

{kind=link}

{kind=link}

{kind=link}