PetSmart Inc. PETM is a leading retailer of pet products and services in the United States. Recently, PETM missed on revenue in 1Q14, and lowered its sales forecasts for FY14. As a result, the stock fell nearly 8%. However, the specialty retailer has a strong history of profit growth and is now trading at its lowest valuation in years. PETM deserves a closer look after this rapid share price decline, and the stock now makes our Most Attractive Stocks list.

Long Track Record of Profitability

PETM currently earns a 15% return on invested capital (ROIC), which ranks in the top quintile of all companies I cover. PETM’s ROIC has also steadily risen from 9% in 2010. This positive trend is attributable to improvements in invested capital efficiency. Average Invested capital turns have improved from 1.52 in 2008 to 2.07 in 2014, a 36% improvement in capital efficiency.

In addition to improving capital efficiency, PetSmart has increased profits (NOPAT) by 11% compounded annually since 2009, and by 22% in 2013 on the back of both its service and retail merchandise growth. PetSmart's long-term track record of profit growth should reassure investors concerned over the recent disappointing guidance from the company.

More Than Just a Retailer

Over the past six years, PETM’s merchandise sales and services sales have grown at a 5% and 6.5% compounded annual growth rate, respectively. This growth showcases PETM’s moat, which comes from the variety of high quality products it carries and the value-added services it provides. PetSmart stocks premium dog and cat foods, many of which are not available at supermarkets, warehouse clubs, or mass merchandisers. PetSmart’s services include pet grooming, training, boarding and day camp, and are not usually provided in discount or unspecialized stores either.

These services also give PetSmart some protection against online competitors like Amazon’s AMZN Wag.com. Wag.com’s status as an Amazon subsidiary should give it some significant logistical and pricing benefits, but it can’t compete with the in-store services PetSmart provides. Additionally, when comparing PetSmart’s top 10 selling dog foods per the company’s own retail website, Wag.com is either priced higher, or does not carry the product all together.

The other major advantage PetSmart has over online-only retailers in taking advantage of growing pet spending comes in the form of “pet parents”, owners who treat their pets like children. These increasingly committed pet owners are more likely to pay a premium for personalized service and utilize PetSmart’s grooming, boarding, and other in-store services. PetSmart is positioning itself as less of a simple retailer, and more as a comprehensive pet care resource for many owners.

Cheap Valuation

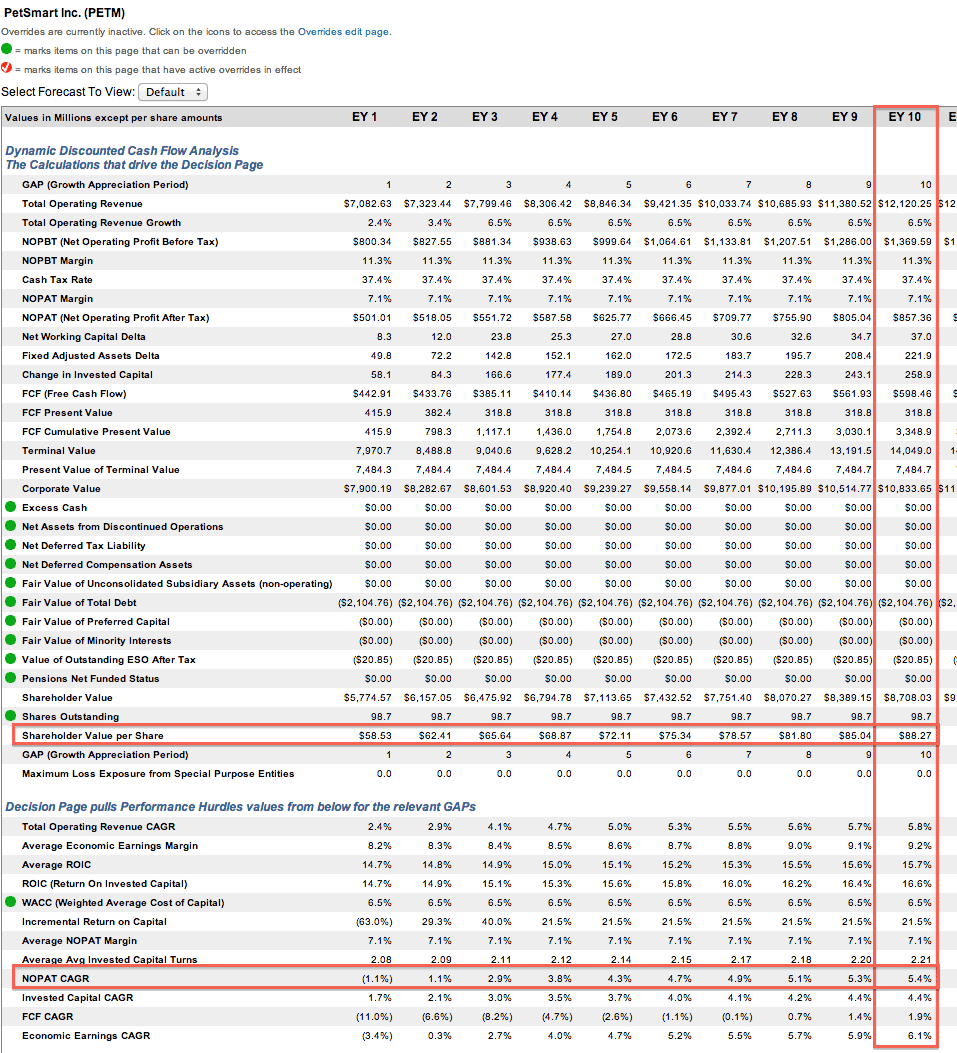

The recent decline in PETM’s stock price creates a great opportunity for investors. At its current valuation of ~$57/share, PetSmart earns a price to economic book value (PEBV) ratio of 1.0. This ratio implies the market expects PETM to never grow NOPAT by any meaningful amount for the remainder of its corporate life. Even in its disappointing quarterly numbers, PETM grew revenue and gross profit by ~1%, and has guided to low single-digit growth in revenues and earnings for the year.

If PETM can continue to grow NOPAT in the low single digits, ~3%, for 10 years, the stock has a fair value of over $70/share. Given that pet spending is expected to grow by about 5% annually in the coming years, this forecast even allows for some market share loss to online competitors.

If we give PETM credit for 5.5% NOPAT growth for the next 10 years, in-line with the expected growth of the industry, the stock has a fair value of over $88/share today. This represents a 55% upside from the current price. Investors should look to PETM for a company with a proven track record of continuing growth, and one that should overcome these short-term issues due to its expansive product selection, value-added services, and intelligent management decisions.

With its lowered earnings and revenue estimates for 2014, PetSmart has set a low bar for itself and minimized the downside risk while improving the chances of an earnings beat. Investors have an opportunity now to buy this solid company at a cheap price.

Funds That Allocate to PETM

Mutual fund investors looking for exposure to PETM should take a look at Wasatch Funds Trust: Wasatch Strategic Income Fund (WASIX), which has a 4.1% allocation to PETM and earns our Attractive rating.

Kyle Guske II contributed to this report.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, sector or theme.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

{kind=link}

{kind=link}