Check out this week’s Danger Zone Interview with Chuck Jaffe of Money Life and MarketWatch.com.

MercadoLibre MELI is often described as “the eBay of Latin America”, but in recent years it has enjoyed margins and a return on invested capital (ROIC) far in excess of eBay EBAY. As EBAY and Amazon AMZN expand in Latin America, we expect MELI’s profitability to regress toward the EBAY and AMZN mean.

End of Market Dominance

MercadoLibre (literally “free market”) was founded in 1999 with a similar business model to eBay, and has enjoyed a dearth of competition since its inception. In 2001, eBay and MercadoLibre entered into a strategic arrangement whereby the American company agreed not to compete in Latin America for five years. EBay also turned over its Brazilian subsidiary to MercadoLibre in exchange for a 19.5% ownership interest in MELI.

Though the strategic agreement expired in 2006, eBay is only now making a concerted effort to grow its business in Latin America. Last month, it rolled out Spanish and Portuguese language websites aimed at shoppers in the region.

In the face of genuine competition, MELI should see a significant decrease in its ROIC and after-tax profit (NOPAT) margins.

The entry of EBAY into Latin America should push MELI’s ROIC and margins down significantly. MELI could be forced to lower fees to sellers and boost spending on items like customer support, advertising, and product development in order to stay competitive. Long-term, it is hard to argue for MELI having an ROIC much higher than EBAY’s, which stands at 17%.

The difference in profitability between MELI and EBAY is extraordinary when one considers how similar their businesses are. Fundamentally, both companies serve as platforms for third party transactions and charge fees to the sellers.

Other Risk Factors

In addition to the likely mean regression of its margins and returns, MELI faces several other significant risks to its stock price. EBay’s expansion into Latin America poses a significant question: Will it continue to hold a significant amount of stock in one of its competitors? EBay holds 8.1 million shares (18%) of MELI, and if it decided to sell part or all of that stake MELI shares could get hit hard.

Another risk factor comes from the unstable economies in some of the countries MELI operates in. Venezuela, whose currency fluctuations have impacted many companies, constitutes 18% of MELI’s revenue. The company has already announced that it will move to reporting its financials in Venezuela at the roughly 50:1 exchange rate, but there are serious concerns at this point about the company’s ability to get any money out of the country.

Similar problems manifest themselves in Argentina, whose currency has been devalued recently and could face further devaluation going forward. Latin American economies may have high growth potential, but they also face significant instability that could damage MELI’s future prospects.

Finally, Amazon (AMZN) could expand its presence in Latin America. The e-commerce giant has recently started selling its Kindle online in Brazil, and further expansion could follow. MELI has the advantage of greater familiarity with the region, but few companies can match AMZN’s logistical expertise and scalability.

Expensive Valuation

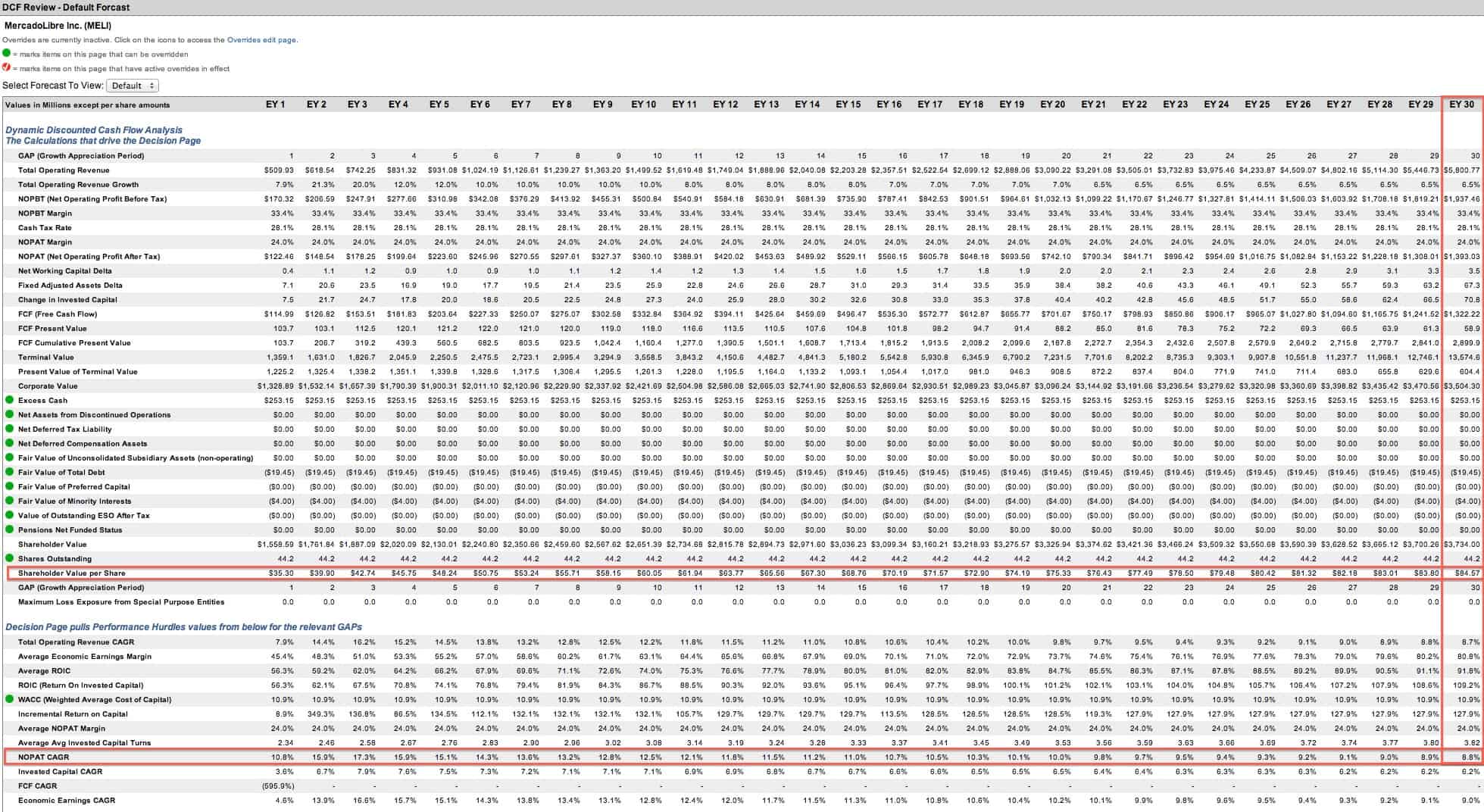

MELI has dropped 20% this year, primarily due to the issues in Venezuela and Argentina, but the stock remains significantly overvalued. Its current valuation of ~$87/share implies that the company will grow NOPAT by 9% compounded annually for 30 years, which is far too long of a growth appreciation period for a company like MELI.

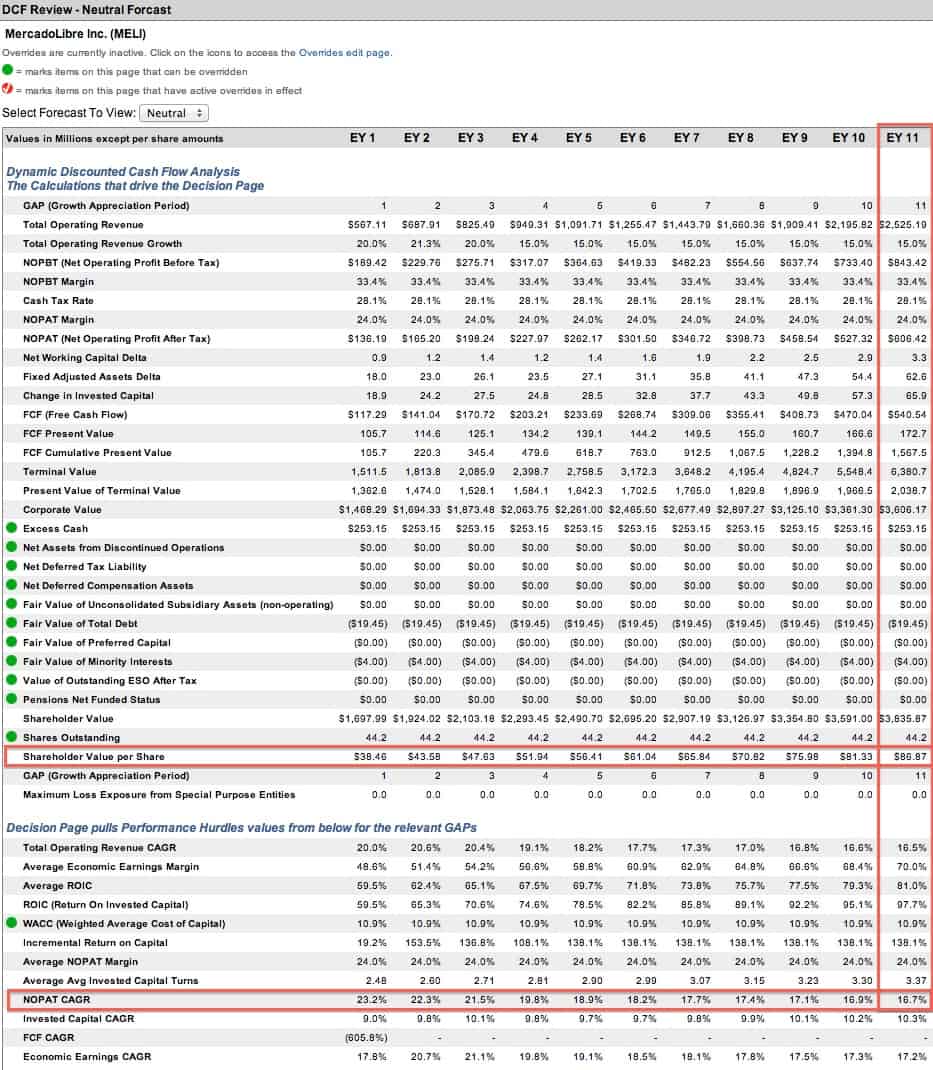

Alternatively, MELI could justify its valuation with 17% NOPAT growth compounded annually for 11 years. MELI grew NOPAT by 17% in 2013, and its NOPAT growth rate has been declining for the past five years, so 17% growth for a decade seems unlikely.

Even with optimistic growth expectations, MELI has significant downside. If the company can grow NOPAT by 10% compounded annually for 10 years, the stock has a fair value of just $50/share today, a 58% downside to the current share price. Even in this scenario, MELI would earn an average ROIC of 70%.

If MELI’s ROIC declines to 20% over the next decade, the stock has a fair value of under $35/share.

Conclusion

MELI did the hard work of establishing e-commerce in Latin America, but now that it’s laid the groundwork EBAY and AMZN look ready to come in and reap the rewards. MELI’s triple digit ROIC was unsustainable, and as competition picks up it should decline to a level similar to a mature company like EBAY.

Latin American e-commerce is a high growth area, but that does not make MELI a good investment. Even if it staves off the competition and keeps growing rapidly, the stock is already priced for significant growth. Given its expensive valuation, multiple potential catalysts, and negative momentum, MELI looks like a good potential short.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

{kind=link}

{kind=link}

{kind=link}

{kind=link}