This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

(Thursday Market Open) Equity index futures were pointing to a lower open as Wednesday’s rally appears to be lacking the legs to follow through into Thursday. Commodities are bouncing back after large selloffs yesterday, and that appears to be weighing on investors. However, today’s Consumer Price Index (CPI) report will attract much of investors’ attention.

The CPI report measured a 0.8% increase month-over-month and a 7.9% increase year-over-year, which means inflation grew as expected. However, these are still very high numbers not seen since the early 1980s. Core inflation that excludes food and energy was up 6.4% year-over-year, which was higher than the forecasted 5.9%. Equity index futures rallied on the report but soon after gave back the gains. All-in-all, there isn’t much here that is likely to push the Fed off the course that Chairman Jerome Powell described to Congress last week.

Investors are probably feeling whiplash from the swings in the market, especially with 2% ranges. While there’s not really anything signaling an end is in sight, we can hope the ranges will at least tighten.

The U.S. markets don’t appear to be getting a boost from a good trading day in Asia. The Japanese Nikkei 225 rose nearly 4% on falling oil prices. The Hang Seng index in Hong Kong rose 1.27%, while the Shanghai composite traded 1.22% higher. However, oil futures are trading higher again this morning, rising 5.25% before the opening bell.

While the Fed is moving slowly to raise rates, some companies are looking to raise capital while interest rates are still low. AT&T T and Discovery DISCA have raised $30 billion by selling 40-year corporate bonds for their joint-venture. The long maturity allowed the group to offer a yield above 3%, which appeared to attract plenty of attention.

After the market closed Wednesday, Amazon AMZN rallied more than 8% on the news that the company had approved a 20-for-1 stock split in February. Splitting the stock allows smaller investors to buy shares without putting a portfolio’s diversification at risk. AMZN also announced plans to buy back $10 billion worth of its shares.

Reviewing the Market Minutes

Stocks bounced back on Wednesday with the S&P 500 (SPX) rising 2.57% and testing the 4,300 level. We’ve been watching that key level as support over the last nine months, but now it’s acting as resistance. This level will be key for some traders. If the bulls are able to surge past resistance, many traders may expect the rally to continue. However, if resistance holds, the bears could push the benchmark index to lower levels.

The bounce was prompted by the Russian foreign ministry spokesperson that said Moscow doesn’t want to overthrow the Kyiv government. Hopefully, this is a good sign for tomorrow’s talks between Russia and Ukraine. However, Ukrainian President Zelensky said that Ukraine wouldn’t yield a “single inch” to Russia. Yesterday, President Zelensky did say that Ukraine would no longer seek membership in NATO (North Atlantic Treaty Organization), which has been a main point of contention for Russia.

The news resulted in a sell-off in commodities, which have been on a tear the last seven trading days. Crude oil futures fell 11.33% on Wednesday, closing below $110 per barrel. Likewise, RBOB gasoline futures dropped more than 10%, and heating oil futures fell a staggering 20% on the day.

Sector Strength Switch

If peace talks are successful, there could be a switch in sector strength. Depending on how oil prices react, energy will likely pull back a bit as crude oil goes through a price discovery phase where investors try to focus on supply and demand instead of speculating what might happen with Russian and Ukraine. However, even before Russia invaded Ukraine, oil prices were still rising, and analysts were projecting prices anywhere from $65 per barrel to $150 in 2022. This means energy stocks could pull back in the short-term but rise over the long term. If this is the case, energy could still be a strong sector.

Wednesday’s sector performance may be a bit of microcosm of what’s to come in the near future if peace prevails. The energy sector was the worst performer with the Energy Select Sector Index falling 3.11%. Financials and technology were the strongest, followed by materials and consumer discretionary. The Financial Select Sector Index rose 3.93% as the 10-year Treasury yield (TNX) jumped more than 4% on the day and appears to be shooting back toward a 2% yield.

If the threat of war lessens, the Federal Reserve is freer to be more aggressive in raising interest rates to combat inflation. Rising rates tends to benefit financials because the spread the between savings and lending widens. In fact, the PHLX KBW Bank Index (BKX) rose 4.19% as a reaction to rising yields.

If resistance on the S&P 500 (SPX) holds, then it’s difficult to say how sectors will react. Wednesday’s rally could simply be a relief rally because the war between Russia and Ukraine is far from over. Therefore, there could still be plenty of anxiety that could keep stocks from following through today. However, war anxiety will make it hard on the Fed to be aggressive against inflation so the inflationary sectors like energy, materials, and financials could still benefit.

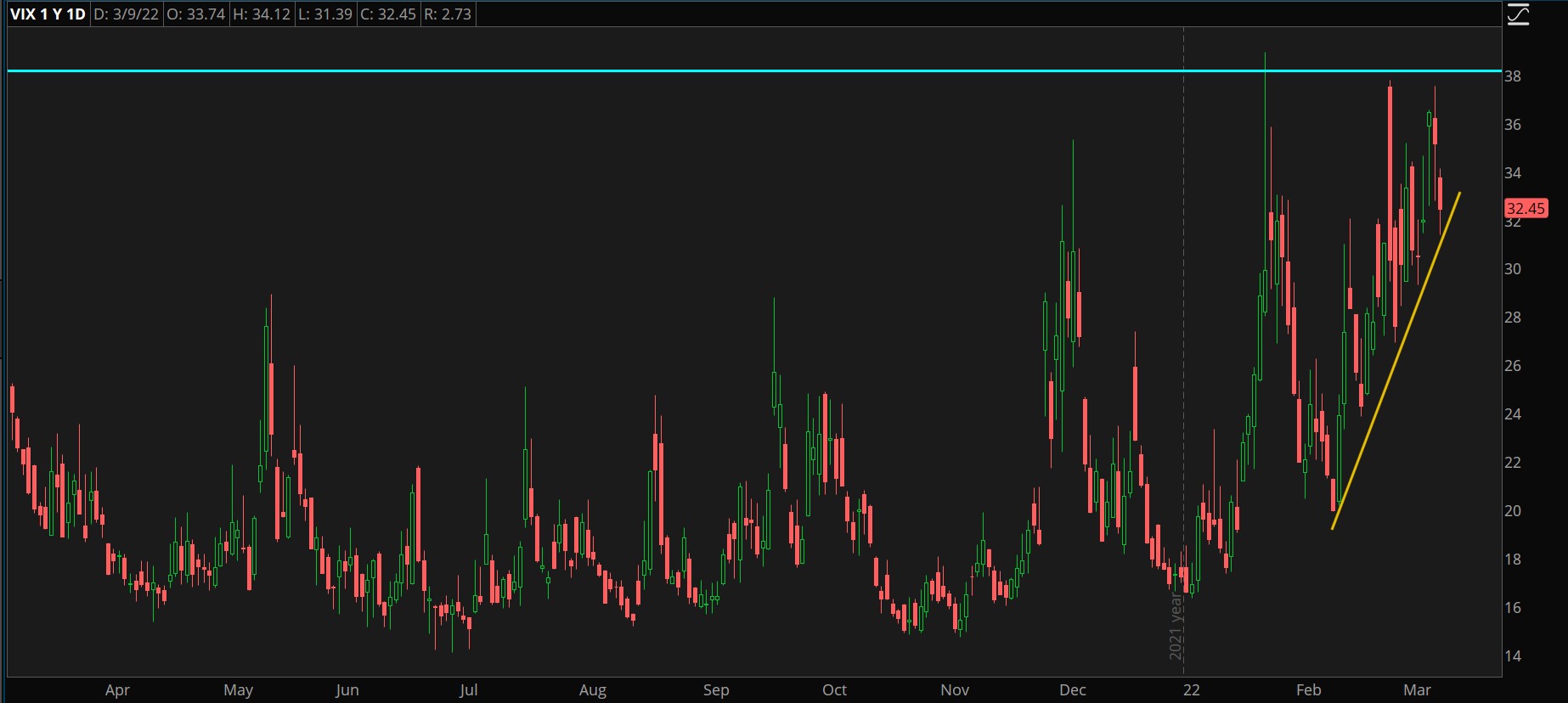

CHART OF THE DAY: FEAR GAUGE. The Cboe Market Volatility Index (VIX—candlesticks) pulled back on Wednesday but stayed above its trendline as it approached the 40 level. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Measuring Fear: Speaking of anxiety, the Cboe Market Volatility Index (VIX), aka fear gauge, dropped 7.63% and is now trading just above 32. There are various levels on the VIX that can help investors measure the degree of fear and complacency. It’s important to remember that these levels are not exact because of the enormous volatility in the index. These levels have also shifted over time.

Gauging Fear: Investor complacency tends to be highest when the VIX is trading below 15. This tends to happen during mature bull markets. Much of 2021 found the VIX at or below 15. However, in 2018, the VIX was as low as 10. When the VIX is around 20, investor anxiety tends to be heightened. This level often coincides with normal market pullbacks. At 30, anxiety is turning to fear. In the early 2000s, this level tended to signal that fear was near a capitulation point. When the VIX hits 40, investors are usually hitting peak fear. The VIX was around 40 when the dot-com bubble popped.

However, there have been times when the VIX has moved much higher. When COVID-19 started coming to the United States and breaking out, the VIX was as high as 90. Similar levels were reached during the credit crisis of 2008. The largest spike ever was Black Monday in 1987 where the VIX topped out above 170.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Pixabay

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.