Stag Week

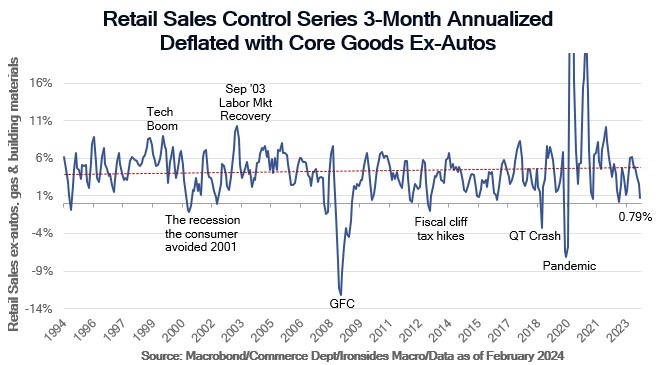

The Fed cutting ‘cause they can, immaculate disinflation, best case scenario, took a significant hit this week due to a hotter than expected CPI, led by non-housing services, and PPI heating back up. The components that feed into the Fed’s benchmark inflation measure, the PCED, from both CPI and PPI, suggest that series will also be hot. Uncooperative inflation data came as no surprise to us, and while we are increasingly convinced demand for labor, particularly from small businesses, is weak, the February retail sales report missed expectations and was revised sharply lower in December. The 3-month annualized rate, both nominal and deflated using CPI core goods ex-autos, decelerated from 6% in 3Q23 to 0.8% in the 3-months through February. Following February retail sales, the Atlanta Fed GDP Now tracking model dropped from 3.18% to 2.34% and the PCE model estimate slowed to 2.24% from 3.36%. If March proves to be similarly soft, 1Q24 GDP tracking models will likely be close to the FOMC’s December Summary of Economic Projections 1.4% median ‘24 GDP forecast. Slowing consumption, combined with the BLS aggregate hours index flat in January and February, implies the economy is off to a slow start in ‘24. The narrative hasn’t yet shifted from robust growth to a growth scare, however through the first two months of ‘24, inflation is running hotter than the FOMC’s December Summary of Economic Projections PCED median forecast of 2.4%, close to their expected growth of 1.4% and while the Fed won’t be convinced by the uptick in unemployment to 3.9%, another uptick in March and the Committee will find themselves missing on both the inflation and employment mandate.

While the S&P 500 was shrugging off hotter than expected inflation and softer consumption data due to ongoing strength in the technology and communication services, as well as a strong performance for energy and materials as crude and copper went on a tear, 10-year nominal and inflation protected Treasuries sold off to ‘24 lows, leaving the 10 & 30-year auctions deeply in the red. Unsurprisingly, small caps and regional banks moved sharply lower. In this week’s note we will review the inflation data and preview what is likely to be a hawkish FOMC meeting. The preview will focus on our outlook for QT, which we think most market participants are viewing as a potential positive, and while we expect a reduction in the contraction cap by June, we also expect a form of a reverse operation twist that shortens duration and adds, albeit slowly, to pressure on longer maturity real rates and term premium.

Figure 1: Core retail sales slowed sharply in recent months; some may have missed the sharp revision to December. Turns out it wasn’t such a strong holiday season.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.