HMOs, PPOs, and EPOs, oh my! Overwhelmed by insurance and its myriad rules, regulations, plan choices and acronyms? That’s natural. That leads many people to ask, How does health insurance work?

You probably already know that you need to get health insurance to cover yourself and your family in the event of an emergency. The vast array of options can make it a challenge to find the plan that’s right for you.

We’ve created a quick and simple guide to help you understand how health insurance works and the most common terms you’ll need to know before you choose a plan.

Know the Lingo

When you shop for health insurance, it’s impossible to choose a plan if you don’t understand the common lingo. Health insurance companies use specific terms to describe how much you’ll pay for your plan and what benefits you’re entitled to, so keep this list of the most common terms open on your desktop while you shop.

Premium

Your premium is the amount of money you pay each month for health insurance coverage. You can pay your premium every month or you may have the option to pay a year’s worth of your premium at once through your health insurer.

Out-of-Pocket Costs

Out-of-pocket costs involve your expenses for medical care that aren't reimbursed by insurance. These include deductibles, coinsurance and copayments for covered services plus all costs for services that aren't covered.

Deductible

Your deductible is the amount of money you’re responsible for paying toward your health insurance costs before your insurance kicks in and starts footing the bills. Most deductibles renew annually, depending on when you sign onto your plan. You must pay your deductible in addition to your monthly premium.

For example, let’s say that you have a plan with a $2,000 deductible that renews annually. This means that in one calendar year, you must pay $2,000 of your health insurance out-of-pocket before your health insurance company pays anything out for care. You can lower your premium by choosing a plan with a higher deductible and vice-versa.

Copayment

A copayment (copay) is the amount you pay when you visit a doctor, specialist or the emergency room. You may pay a copay every time you see a doctor or only until you reach a certain amount in health care spending or you may still have to pay your copay after you meet your deductible. It all depends on your plan.

Affordable Care Act

The Affordable Care Act (ACA) is a federal statute instituted in 2010 that changed the way health insurance companies operate. The ACA introduced a number of new healthcare regulations, most of which are still in place today.

Under the ACA, health insurance providers cannot deny you coverage due to a preexisting condition. They also cannot drop you from coverage if you get sick or sell you a plan that doesn’t include essential benefits like maternity care, mental health care and coverage for emergency services. The term “ACA-compliant” means that a health insurance plan meets the bare minimum standards under the ACA. Plans that are not ACA-compliant are usually Medicare supplemental insurance plans or “gap plans” that aren’t intended for use as a long-term coverage option.

Coinsurance

A coinsurance percentage is the percentage of your total medical costs that you pay after you meet your deductible.

For example, if you have a $1,000 bill and your plan has a 20% coinsurance percentage, your insurance will cover 80% of your bill ($800) and you’ll pay the remaining 20% ($200). You may still have to pay a copay after you pay your coinsurance percentage.

Primary Care Provider

Your primary care provider is the doctor you see for scheduled, non-emergency care. Your primary care provider may handle your annual checkups, order blood work or other diagnostic tests and make sure you and your children are on schedule with vaccines and boosters.

Specialist

In health care terminology, a specialist is a doctor or medical professional who deals with a particular set of illnesses or parts of the body. Some examples of specialists you might see include dermatologists, psychiatrists and cardiologists.

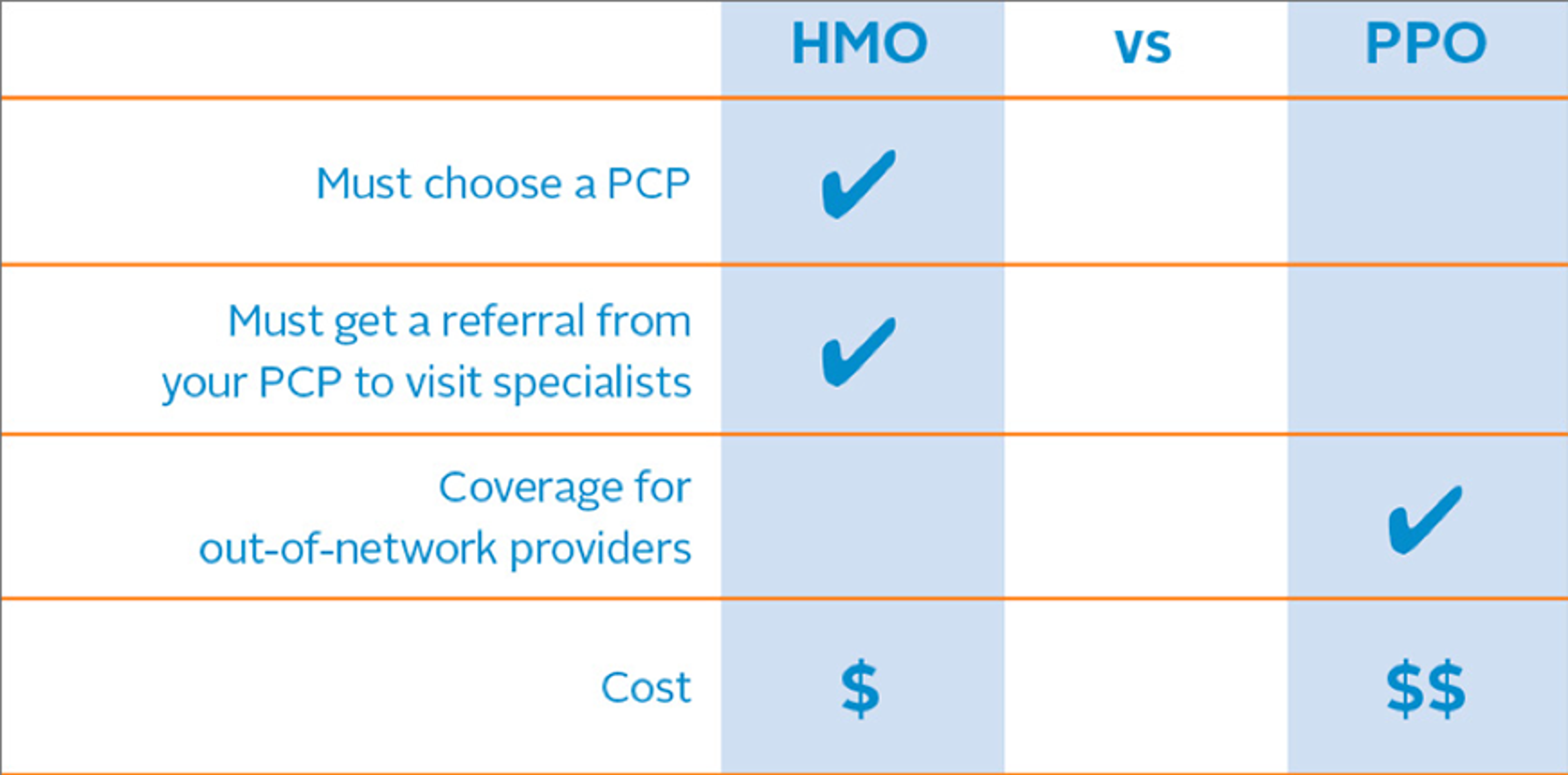

Health Maintenance Organization (HMO) Plan

HMO plans are a common health insurance plan structure. You must see doctors and specialists within the HMO’s predetermined network and you must get a referral from your primary care provider before you see a specialist. HMOs are usually the most affordable type of health insurance plan.

Preferred Provider Organization (PPO) Plan

A PPO is a type of insurance plan that grants you more flexibility when it comes to choosing which medical professionals you visit. You may choose any primary care physician in a PPO whether he or she is in your health insurance network. You may also see a specialist without a referral from a doctor with a PPO plan.

Medicare

Medicare is a federal insurance program for men and women over the age of 65 that pays for certain health care expenses.

Medicaid

Medicaid is a joint federal and state program that helps low-income individuals pay for doctor visits, hospital stays and long-term medical expenses. Unlike Medicare, Medicaid recipients may be any age.

Going Through the Health Insurance Process

Now that you’re familiar with some of the most common health insurance terms, it’s time to learn about how you can choose a plan and get covered.

Signing Up for Coverage

If you don’t already have health insurance coverage, you can get coverage through the ACA Marketplace during Open Enrollment. Open Enrollment is an annual period in which you can sign up for an individual health insurance plan. For 2023, Open Enrollment is scheduled to begin on November 1 and close on January 15, 2023. Plans sold during Open Enrollment go into effect on January 1, 2023.

If Open Enrollment isn’t currently available but you need coverage now, check to see if you qualify for a Special Enrollment period. Some events that trigger a Special Enrollment period include:

- Losing your health insurance because you lost a job

- Have a new baby

- Get married

- Turn 26 and are removed from your parent’s health insurance

If you think you might qualify for a Special Enrollment period, you can check out the complete list of qualifying events through Healthcare.gov.

If you do qualify for a Special Enrollment period or if Open Enrollment is open, you can sign up for a plan through your state’s ACA Marketplace. Start by creating an account through Healthcare.gov, enter information about your residence and family and browsing plans that will accept new policyholders.

If Open Enrollment isn’t open and you don’t qualify for a Special Enrollment period, you may want to consider signing up for a short term health insurance plan from a health insurer to protect yourself and your family from major financial hardship in the event of an emergency.

Short term health insurance plans provide only bare necessities to bridge the gap in coverage while you wait for Open Enrollment to begin. Keep in mind that short term health insurance plans do not have to provide the essential benefits outlined in the ACA and most short term plans don’t include coverage for mental health issues and maternity care. You may be denied due to a preexisting medical condition. You should only use short term health insurance plans as a last resort, and you should transition to an ACA-compliant plan as soon as possible.

Getting Care

After you’ve signed onto your policy, begin using your insurance benefits. Check your policy limits and make sure that you understand your deductible, coinsurance and copayment requirements before you make an appointment.

Most health insurance plans have a waiting period before benefits kick in, usually ranging from 15 to 30 days. Use this time to contact your primary care provider and ensure that he or she is within your network (if you have an HMO) or how much extra you’ll pay for using his or her services (if you have a PPO or other type of insurance with out-of-network benefits). If your primary care provider is not in your network, contact your health insurer or insurance agent for a list of local providers who accept your insurance.

Paying for Health Care

Understanding what costs you must pay for your insurance can help you choose a plan that fits within your family’s budget. Some of the payments you’ll need to consider when you choose a plan include:

Monthly Premiums

Your monthly premium is a set amount that you’ll pay every month to maintain your insurance coverage. Your health insurance provider uses a number of factors to calculate how much you’ll pay in premiums each month, including whether or not you smoke, how many people are on your plan and your age. When you compare health insurance plans, keep in mind that the plan with the lowest premium isn’t always the best one. Plans with low premiums usually also have much higher deductibles.

Most health insurance plans do not include dental insurance or vision insurance except for any children under the age of 18 who are on your plan. If you want dental and vision coverage, you’ll usually need to choose and pay for a separate plan.

Deductibles and Copays

You’ll also have to pay a deductible and copay for your plan.

A deductible is a set amount that you pay for your health insurance coverage before your insurance kicks in. A deductible usually doesn’t include costs you pay for your copay or your premium, though some plans may factor these costs in. After you reach your deductible, you’re only responsible for paying your coinsurance percentage and your copay.

Your copay is a fixed amount you pay before you receive a medical service. Copays are usually paid every time you use a specific service or health care provider. If you have a $20 copay per doctor’s visit and you visit your doctor three times in a year, you’ll pay $60 in copay charges.

Copays usually don’t count toward your deductible, though this policy varies by plan. Your insurance company will usually issue you a health insurance card. Your health insurance card lists how much you’ll pay in copays each time you visit your primary care provider, a specialist or the emergency room.

Your insurance plan also includes an out-of-pocket maximum. This is the highest possible annual dollar amount you’ll pay for your insurance. After you reach your out-of-pocket maximum, your insurance provider will cover 100% of your healthcare costs.

Getting The Coverage You Need

Getting health insurance coverage is important — but so is choosing the right provider and plan. If you’re currently waiting for Open Enrollment to begin, use this time to research healthcare providers in your state and your state’s minimum essential benefits beyond what’s required by the ACA.

Take a look at your finances to determine how much you can afford to pay as a premium and an annual deductible while working toward other financial goals

Want to learn more about health insurance? Check out Benzinga's guides to the best affordable health insurance companies, the best cancer insurance companies and the best health insurance for the self-employed.

Frequently Asked Questions

Is health insurance required?

The federal mandate that required health insurance has been lifted but some states have enacted state-level mandates that require residents to have health insurance. Even where not required, health insurance can protect your family against catastrophic healthcare costs and help make routine medical expenses more predictable. Get your most affordable quote through our top providers today.

What does health insurance cover?

Most health insurance plans provide the 10 essential health benefits that were part of Obamacare requirements. Coverages include preventive and wellness services, prescription drug coverage, emergency services, ambulatory services, lab services, pediatric services, and more. Many plans cover a wider range of healthcare expenses but may cost more than basic plans or may have higher out-of-pocket costs for some services.Get a custom health insurance quote to cover you and your family today.

How can I save money on health insurance?

For healthcare plans that comply with the Affordable Care Act, only a handful of rating factors affect your premium. These include age and location, at least one of which can’t be changed. Smokers will pay more in most cases and your choice of plan level can affect premiums as well. Choosing a high deductible health insurance plan can reduce the cost of premiums. These plans can be combined with a health savings account to take advantage of tax-free savings for healthcare expenses. Get the cheapest health insurance premium from top providers.

Related content:

About Sarah Horvath

Sarah Horvath is a highly respected freelance senior copywriter specializing in insurance content. With a wealth of experience, she is recognized as one of the top insurance copywriters in the industry. Sarah’s expertise encompasses various aspects of insurance, including home warranties, life insurance, health insurance, and more. Her insightful articles and guides are regularly featured on major finance sites, providing invaluable information to readers seeking to navigate the complexities of insurance policies. Known for her clear, concise writing style and comprehensive understanding of insurance products, Sarah is dedicated to empowering individuals with the knowledge they need to make informed decisions about their insurance coverage.