If you’ve ever said to someone, “I owe you one,” you essentially already know what a bond is. A bond is an I.O.U. between a borrower and a lender.

Municipal bonds are debt securities issued by state and local governments sold in exchange for periodic interest payments and the eventual return of the investment funds or principal when the bond matures. The funds raised by the sale of these bonds generally get used for local infrastructure development, such as bridges or capital projects like public housing.

When you buy a municipal bond, you generally receive an interest payment twice a year with the principal or initial investment paid to you at the bond’s maturity date. Most municipal bonds mature from one to 10 years after their issue, depending on whether they’re long-term or short term bonds.

Before You Invest in Municipal Bonds

Municipal (or muni) bonds cater mostly to people in high tax brackets due to the fact that interest payments on muni bonds aren’t taxed by the federal government. In many places, they are exempt from state and local taxes as well. The tax exemption and inherent security of the bond, which generally has the backing of the municipality of origin, makes munis a safer investment than stocks or corporate bonds.

Municipal bonds do not trade without some risk. For example, if the governmental entity responsible for the bond’s issue defaults, you run the risk of losing your entire principal in addition to forgoing interest payments, if any. Familiarize yourself with the party responsible for the bond’s repayment and the financial condition of the issuing entity so you can assess the credit risk involved. You can then proceed to invest in the bond if you feel it’s sufficiently safe to do so.

Since default rates for municipal bonds have been extremely low for a long time, this makes municipal bonds attractive to investors looking for relatively low-risk, fixed interest income. Also, credit ratings on muni bonds tend to be higher than on corporate bonds.

You can buy municipal bonds in several different ways. Depending on the level of involvement you wish to have in your purchase, you can go through a broker-dealer or a bank that’s also a municipal securities dealer.

In addition to using a broker-dealer, you can hire an investment manager to locate and trade bonds on your behalf. Another way is to buy bonds directly online through a self-managed account, or you can buy shares in a mutual fund or exchange-traded fund (ETF) that specializes in municipal bonds.

If your goal is fixed income over a certain period of time and the full return of your principal with little trading activity, then your best bet is typically a broker-dealer that will charge a commission or markup. If you plan to trade bonds frequently, you might consider a broker that does not charge per transaction. Because municipal bonds generally have a minimum denomination of $5,000, an investor with limited funds might consider a mutual fund or ETF.

Buying Municipal Bonds Using a Broker

Using a broker gives you two basic options. You can either open an account with a full-service broker-dealer, which lets you consult with a bond professional or you can open an online account with a broker that offers municipal bonds to clients. Many large banks also allow their high net-worth clients to participate in municipal bond offerings as well.

Buying bonds is easy, especially if you read through the following steps, evaluate your needs and pick the right products for you.

- Open an Account with a Full-Service Broker-Dealer or Online Brokerage

You can either open an account with a full-service broker-dealer or an online brokerage to get access to the municipal bond market. The two differ considerably in costs and services, so make sure to choose the right type of broker for your situation.

- Place Your Order

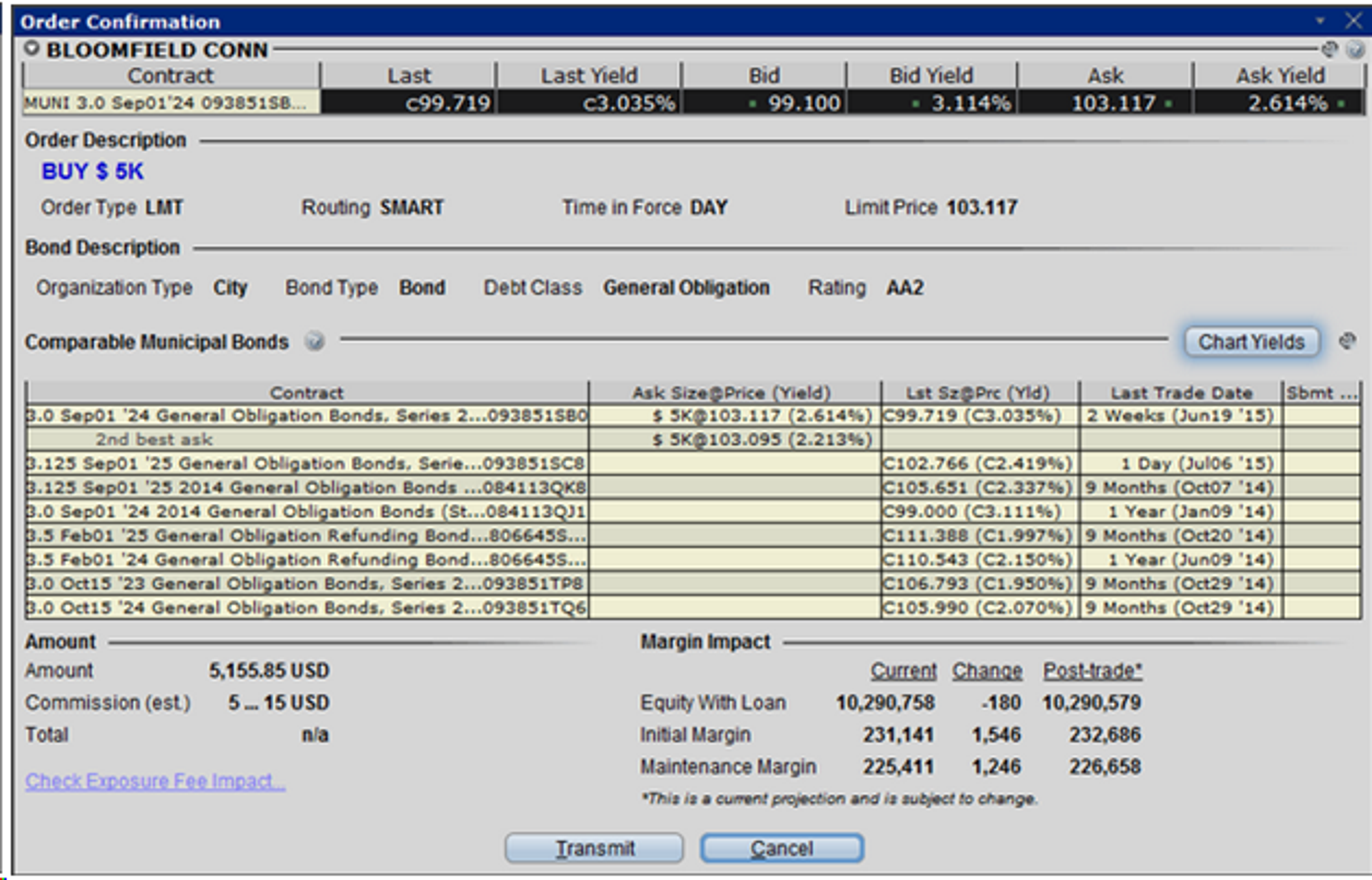

After you open your account either with a full-service broker or with an online broker, and talk with your financial advisor or research which bond to buy on your own, you can then place your order to purchase a municipal bond. Make sure you check the bond issue’s official statement, which is like a prospectus for a newly issued stock.

Remember to keep track of the financial condition of the issuer in the event that some delinquencies on payments of interest or principal occur. You can check on municipal bond issuers and their financial status at the Municipal Securities Rulemaking Board’s (MSRB’s) Electronic Municipal Market Access (EMMA) website.

- Best For:Most Available BondsVIEW PROS & CONS:Securely through Interactive Brokers’ website

Brokerage Types

Full-Service Broker-Dealer

Municipal bond purchases require an account with a full-service broker-dealer or an account at a bank with a department licensed as a municipal securities dealer. Since bonds trade in lot denominations of $1,000, $5,000 and $10,000, the minimum deposit for this type of account can be quite high for some investors.

Once you’ve opened your account with an authorized broker-dealer and have been assigned a private client broker, you disclose your risk parameters and other particulars about your goals. If you plan to use a bank’s municipal bond department, then you must have an account open at that bank and talk to the customer representative assigned to the bond department.

Before you make your purchase, the broker has an obligation to disclose all material information about any municipal security it sells to you and must offer a fair and equitable price on the bond. The broker also has the obligation of only offering securities within the your desired risk profile.

The broker-dealer charges a fee for buying or selling bonds for clients. If the broker-dealer acts “as principal,” then this means that the broker has the bond in inventory and sells it with a “mark-up” when the broker sells the bond and charges a “mark-down” when the broker buys the bond from a client.

If the broker-dealer acts as an “agent,” this means that they assist the client in locating and purchasing the bond in the marketplace. The broker-dealer then charges a commission for acting as agent. Fees and commissions can vary considerably depending on the broker-dealer. You can check on a broker’s qualifications through the Financial Industry Regulatory Authority (FINRA) that has an online research tool called BrokerCheck.

Full-service brokers can give you advice on investment strategy, taxes and retirement planning, although these services may cost extra. Keep in mind that once you have received all disclosures and recommendations from the broker-dealer, you have the ultimate responsibility when it comes to decisions to buy or sell. The broker-dealer has no further obligation at this point to meet fiduciary standards.

Online Brokerage

The other method of getting access to the municipal bond market involves opening an account with a large online brokerage like Charles Schwab or Interactive Brokers. Online brokers with a bond department generally have low fees and commissions and offer an online bond trading platform.

If you choose an online broker, you won’t get the service and professional research you would at a full-service broker-dealer, but you do get access to the broker’s research at a lower cost. Other online brokers with bond market access include E-Trade, Scottrade, Fidelity and TD Ameritrade.

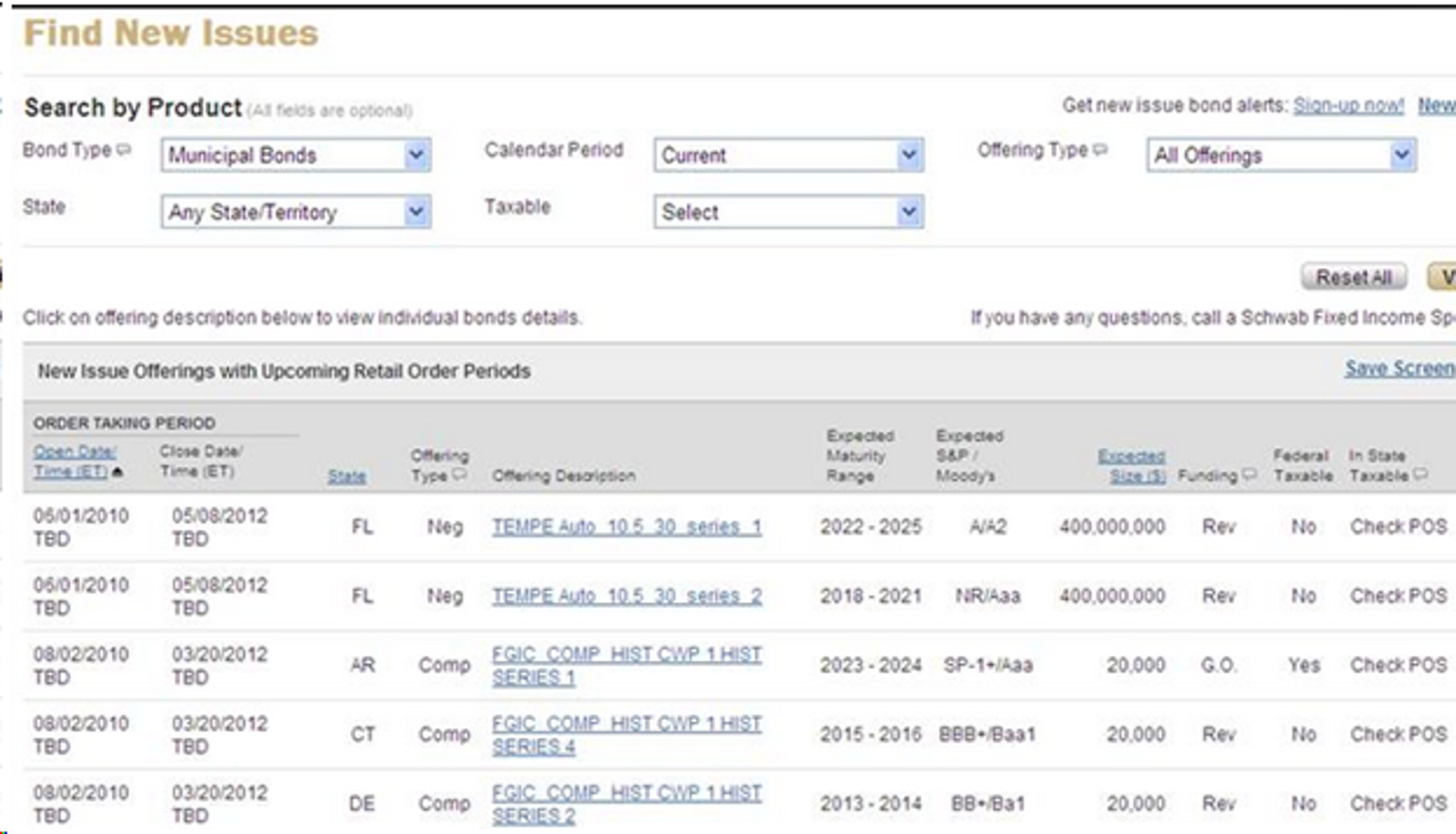

If you tend to be more self-directed and already have specific goals, then researching and buying the best municipal bonds you can find through an online broker would make sense for you. This would also probably save you money compared to using a full-service broker. You can also use a service like Charles Schwab’s, shown below, to find new bond issues.

Buying Municipal Bonds Directly

If you prefer to buy your municipal bonds directly from the governmental entity issuing the bond, then you would need access to the municipal bond primary market. Access to this market is generally reserved for banks, financial institutions,bond funds

Step #1: Open an Account

In order to get involved at this level, you compete with banks and other financial institutions, so you must have an account with substantial assets at one of the banks that syndicate the offer. You must ask to be alerted to municipal bond offerings and get put on a list. You would then be delivered the offering document and prospectus with the date of the issue and the amount to be raised.

Step #2: Place Your Order

Once you have received and read the prospectus or official document for the offering, contact your bank syndicating the bond issue and put in your request with the bank’s investment representative for your choice of bond coupon, maturity date and number of bonds you’re interested in purchasing. Each bond normally has a value of $1,000.

The bonds, which are offered on a schedule, have a two- to three-day time frame known as the retail order period before the syndicating banks distribute the offering and decide how much of the offering to allocate to financial institutions and retail investors.

Step #3: Receive the Bonds in Your Investment Account

After the transaction is complete, you receive the bonds in your account at the syndicating bank. You could either take physical possession or you could leave them in the account where you would receive your tax-free interest payments.

Final Thoughts

Municipal bonds are a great long-term investment and they don’t have to be difficult to purchase. In addition to receiving tax-free interest payments, you get a degree of security not available with corporate bonds or stocks.

If interest rates increase, the face value of your bond declines, which really doesn’t matter if you plan on holding the bond until it matures.

Note that holding bonds doesn’t help as an inflation hedge either and you do run the low risk that the issuing governmental entity becomes insolvent. Outside of that, municipal bonds make a solid addition to just about any investment portfolio.

Want to learn more? Check out our guides to the best online brokerages, free stock trading and the best bond funds.

About Jay and Julie Hawk

Jay and Julie Hawk are a married financial writing and authorship team who co-founded TheFXperts, a notable financial writing services provider. The Hawks each worked professionally in the financial markets and have more than 40 years of trading experience among them. Together, they write books, trade forex online for their own account and others, mentor traders, and have worked actively as professional freelance writers specializing in financial topics for over 15 years.