Source: CME Group

Over the prior weeks the markets have priced in hikes in several regions; volatility and options volumes on Eurodollar futures have jumped higher; and regulators are continuing to guide markets to shift from LIBOR to SOFR futures and options.

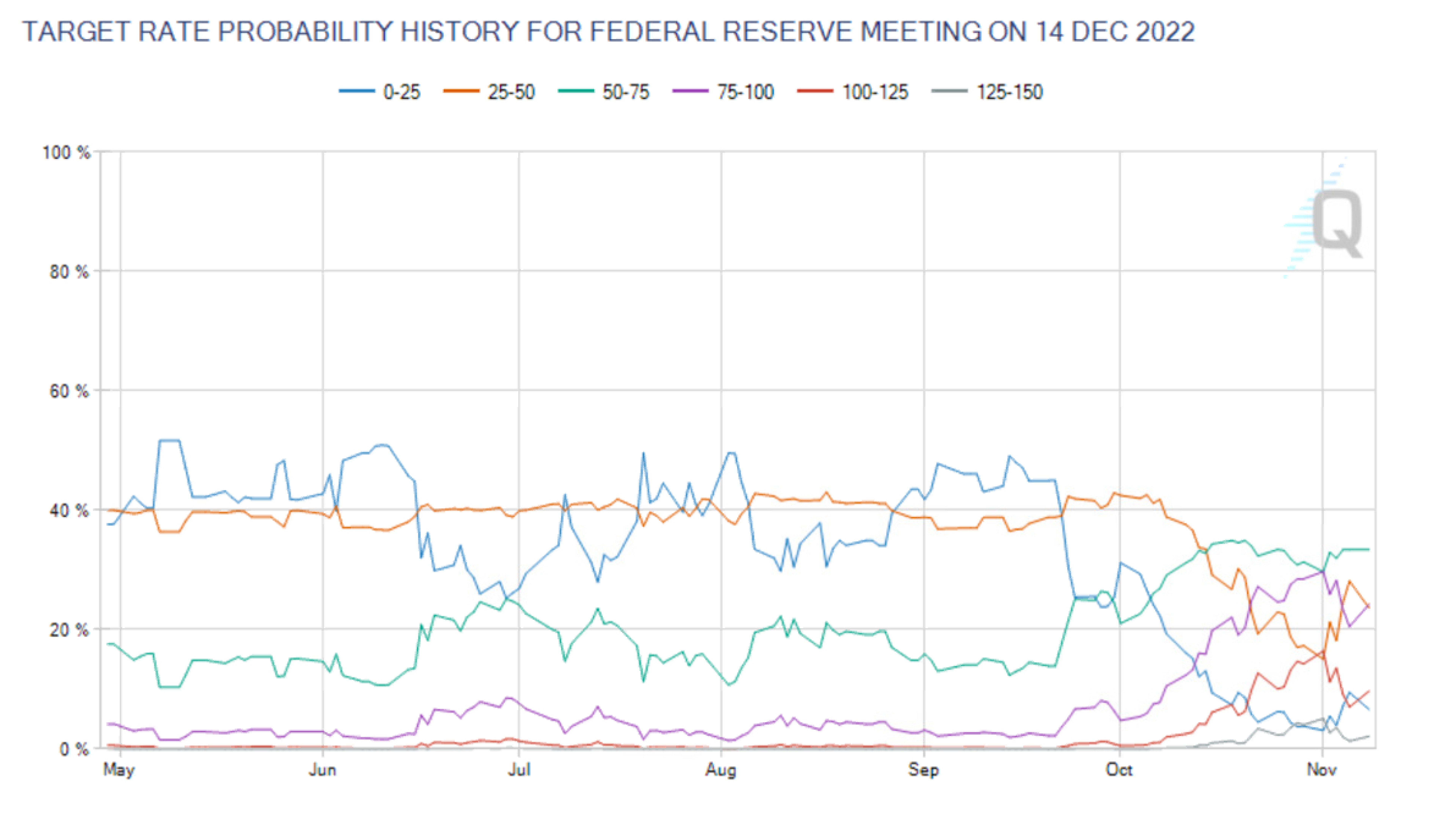

FOMC Rate Hike Expectations Have Shifted Higher

Since the beginning of October, the CME FedWatch Tool has indicated an increased probability of a second hike by the end of 2022. The purple line in Exhibit 1 shows how expectation of a second hike has leapt higher. Concurrently the market has priced a very low probably of no hikes (blue) and the probability of one hike (orange) has fallen off the table from 40% to less than 20%.

CME FedWatch Tool Historic Probabilities of Various Hikes. Source: CME Group

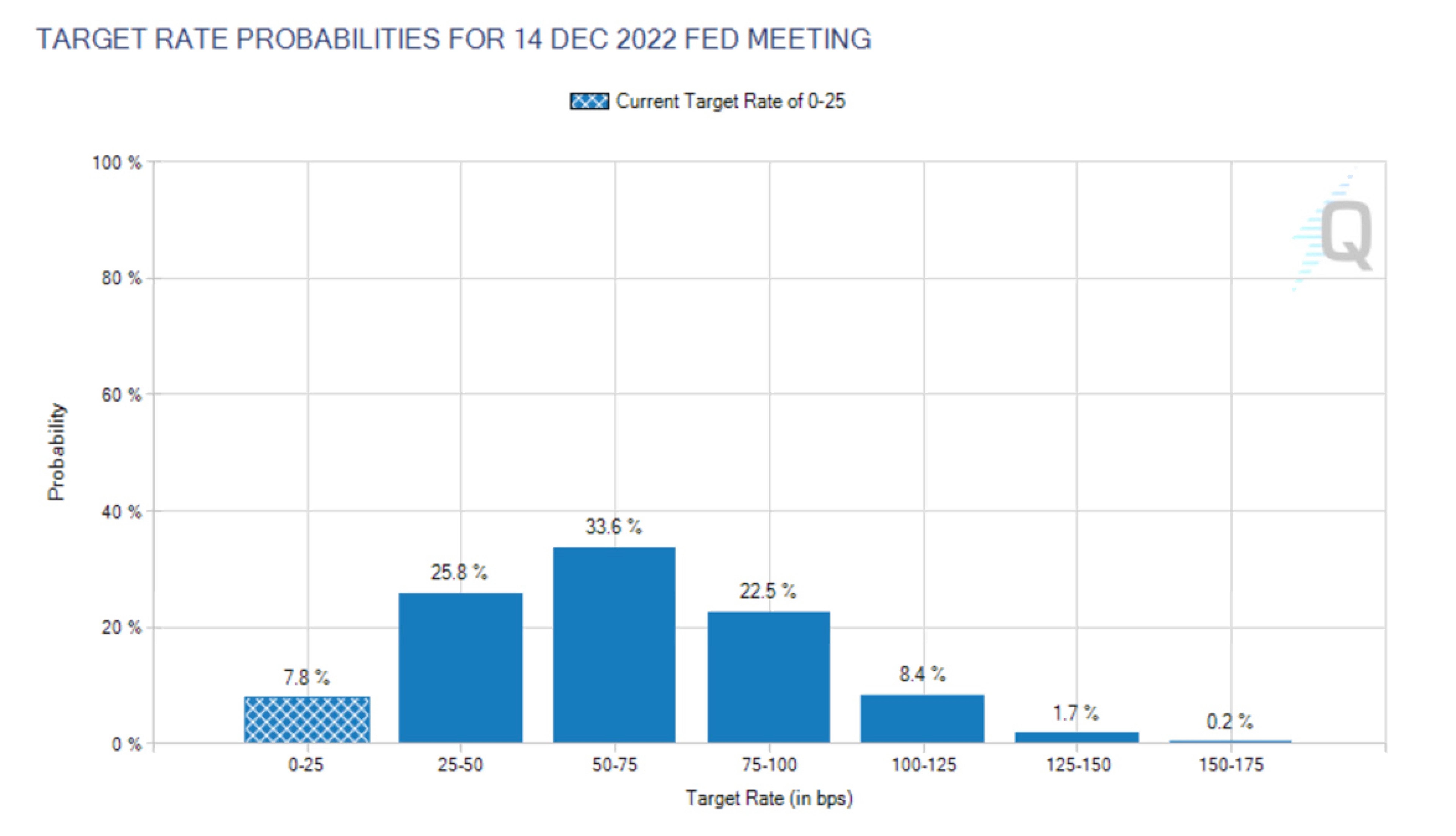

The distribution profile of December 22 rates is shown in Exhibit 2 and it looks somewhat like a normal distribution with the highest probability of a target rate of 50-75 basis points. Importantly, the distribution is somewhat skewed to the higher side with the market pricing a rate regime of 100-125 basis points at nearly 18%.

CME FedWatch Tool for December 2022. Source: CME Group

Eurodollar Options on Futures Volumes Have Jumped

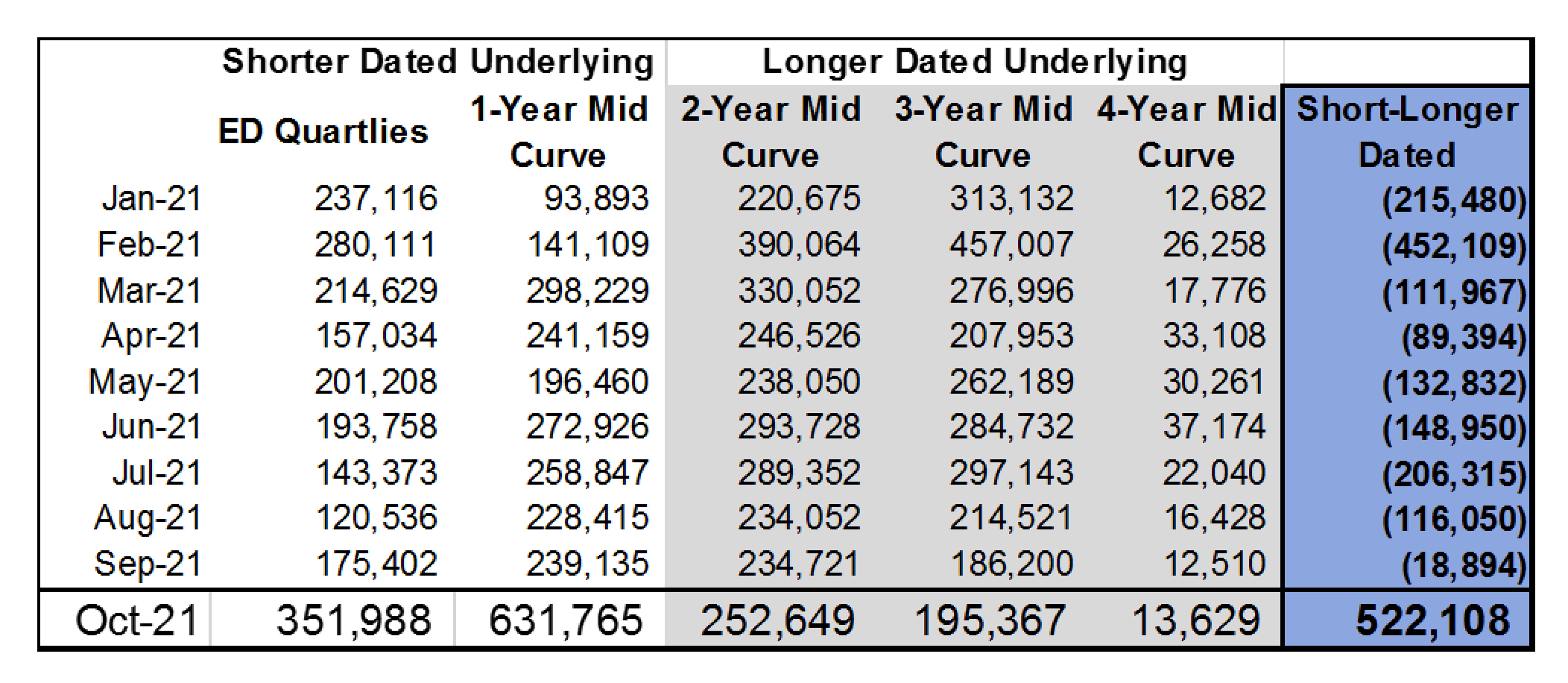

Beginning with the zero-interest rate policy in 2008 and continuing through the following decade, volumes in Eurodollar Quarterly and Mid-Curve options have been solid indicators on when the market expects rate hikes to occur. When the market does not expect rate hikes for two or three years, one can see larger volume in the 2-, 3- and 4-year Mid-Curves. Alternatively, as Fed expectations move into the near term, a shift with volume concentrated in the shorter-dated quarterlies along with the 1-year Mid-Curve options can be seen.

As recently as October, markets responded to these changes in Fed expectations with average daily volume (ADV) significantly moving into both Quarterlies and 1-Year Mid-Curve options. Through the first three quarters, the market was focused on positioning the underlying 2023, 2024 and 2025 futures contracts illustrated by the negative numbers in Chart 1. Based on historical trends, this indicates that the market saw more potential for curve movement in the longer dated part of the curve beginning with 2023.

Selected Eurodollar Options on Futures ADV. Source: CME Group

This changed significantly in October. Short-end volumes outperformed the long end by over 500,000 contracts ADV. This shows the market is much more focused on rate risk in the next 6-18 months. As for volatility in the 1-year Mid-Curve, highs have been reached at 54.6 bps. This is the volatility of a 90-day option and in the December 22-March 23 time frame.

The jump in volatility has permeated other rate markets as well. CME Group Volatility Indexes (CVOL) for the 2-Year Treasury future also show a significant breakout on 30-day implied volatility.

Image: CME Group 2YR CVOL Index (TVUY)

While option volumes and interest rate volatility have been increasing, so has the attention that the regulators are giving non-linear (option) products based on LIBOR.

Regulatory Decree Encouraging Move from LIBOR to SOFR

Slightly over three months ago, the Commodity Futures Trading Commission (CFTC) Market Risk Advisory Committee (MRAC) in a release “adopted a market best practice known as SOFR First.” In the words of the MRAC, “SOFR First represents a prioritization of trading in SOFR rather than USD LIBOR for particular market segments and products, which is designed to help market participants decrease reliance on USD LIBOR in light of supervisory guidance that such activity should cease as soon as practicable and in any event by December 31, 2021.”

The timeline is clear and is in four phases:

- Phase 1 – Linear Swaps (Complete)

- Phase 2 – Cross Currency Swaps (Complete)

- Phase 3 – Non-Linear Derivatives (November 8, 2021)

- Phase 4 – Exchange Traded Derivatives

Since the completion of Phase 1, volumes on SOFR futures have skyrocketed.

Source: CME Group

With November 8 passed, dealers are now focused on moving from LIBOR-based swaptions to SOFR-based swaptions. Indeed, with the March 2021 inclusion of SOFR-based fallbacks in the Eurodollar futures rulebook, contracts with an underlying greater than June 2023 are effectively SOFR-linked contracts.

In early 2020, CME Group launched 3-Month SOFR options duplicating the entire Eurodollar and Mid-Curve options complex. The trends in linear products suggest that the coming SOFR First guidance, along with Fed guidance on the use of LIBOR, could encourage additional uptake in SOFR-based swaptions and options on SOFR futures.

The Times, They are a Changing

The market has quickly changed its forecasts for the path of future interest rates. Eurodollar options have responded in kind. The CFTC’s SOFR First initiative is rapidly moving non-linear risk taking to SOFR-based products. CME Group Watch Tools can show the changes in market expectations, but market participants will do well to heed upcoming phases of SOFR First and prepare now for non-linear SOFR products.

The preceding post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga. Although the piece is not and should not be construed as editorial content, the sponsored content team works to ensure that any and all information contained within is true and accurate to the best of their knowledge and research. The content was purely for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.