Zinger Key Points

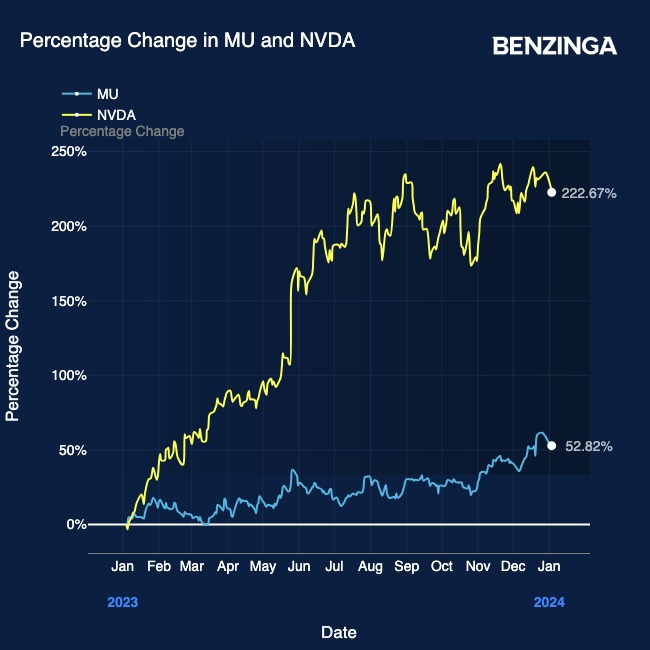

- Despite Micron's stock surging nearly 70% in 2023 amid a revenue decline of about 40%, underlying challenges persist.

- The near term profitability metrics for Micron remain clouded, rival Samsung's impending entry looms large in the HBM memory space.

- Don’t miss this list of 3 high-yield stocks—including one delivering over 10%—built for income in today’s chaotic market.

Micron Technology Inc MU is a stalwart in computer memory and storage solutions. Currently, the company is at a critical juncture as it navigates through an evolving semiconductor market. While the company touts progress in AI-driven memory chips and its bid for a substantial share of the HBM memory market, formidable rival Samsung‘s impending entry looms large, setting a cautious tone for Micron’s future.

Despite strides in production ramp-ups highlighted in Micron’s recent fiscal first quarter (FQ1’24) earnings conference, management’s tempered approach reflects a keen awareness of past overspending pitfalls. The burgeoning AI chips revolution that spurred NVIDIA Corp NVDA to new heights (up 232% over the past year), has also buoyed Micron’s recovery to a good extent. Micron’s stock is up 63% over a one-year period.

Also Read: Chip Stocks At ‘Premium Valuations’: Why Bank Of America Is Bullish On Semiconductors In 2024

Despite Micron’s stock surging nearly 70% in 2023 amid a revenue decline of about 40%, underlying challenges persist. Micron’s trajectory hinges on executing recovery plans while adeptly navigating Samsung’s aggressive foray. The stock’s exuberance in recent years without revenue growth hints at market expectations that might not align with industry realities.

Also Read: Why Micron Technology Shares Are Falling

The near-to-medium-term profitability metrics for Micron remain clouded. While the current supply/demand balance favors memory players, Samsung’s anticipated robust participation poses a potential game-changer.

Samsung’s aggressive aspirations and advanced packaging challenges, introduces uncertainties. Particularly in the HBM memory chips segment, where Micron aims to challenge the dominance of SK Hynix. Reports speculating on Samsung potentially outstripping SK Hynix’s HBM production by the second half of 2024 highlight the intense competitive landscape that Micron faces.

Market forecasts anticipate a remarkable recovery for Micron through FY25, with estimated adjusted EBITDA demonstrating substantial year-over-year growth. Yet, this optimism is juxtaposed with concerns of whether the market has adequately factored in Samsung’s potentially aggressive strides.

Micron’s current EV/EBITDA (FWD) multiple of just 13.4 (against sector median of 15.05) suggests that the markets may not be fully accounting for Micron’s forthcoming recovery amid intensifying competition. Micron currently stands at the crossroads, facing a challenging path to recovery in the highly competitive semiconductor industry.

Photo: Shutterstock

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.