The More Problems In Sovereign Debt Issue

We’re looking at massive worldwide sovereign debt problems. The Bank of Japan decided to stop defending the 1% rate ceiling on its 10-year bond to stop further weakness in the yen. Not to be outdone, the US Treasury announces plans for trillions of dollars of new bond auctions. At some point, governments are going to have to live with the fact that they can’t improve their citizens’ standard of living by just printing new currency. That day is not today.

This week, we’ll address the following topics:

-

The Federal Reserve continues its pause and reiterates “higher for longer”.

-

Upcoming Treasury auctions are about to flood the government bond market.

-

The Bank of Japan throws in the towel for the third time in the last year.

-

Manufacturing PMI shows greater than expected contraction.

-

The new jobs report disappoints. Market responds positively.

Ready for a new week of terrifying government fiscal policies? Let’s dive in:

-

The Fed Continues to “Pause”:

The Federal Reserve completed its two-day meeting and decided to keep the fed funds rate unchanged. In his press conference, Fed Chairman Powell did deliver one hawkish message. He made it clear that if inflation remains high and economic activity remains higher than expected, the Fed could raise rates again. Powell further said that they were not even considering lowering rates right now.

Powell paused and the markets celebrated.

DKI Takeaway: It’s clear that we’re at or close to the terminal rate meaning the end of rate hikes in this cycle. While the market celebrated this by rising on subsequent days, we’re a little more skeptical. Powell again noted that higher long-term bond yields are continuing to do some of the Fed’s work for them. DKI thinks the bond market is now watching Congressional overspending and massive announced bond issuances from the Treasury Department. The Fed is “paused”, but long-term rates are less tied to Fed policy and may continue to rise.

-

US Debt Issuance is and will be Massive:

The US government announced it will add $1.6 trillion in new debt over the next two quarters. This comes after borrowing another $1 trillion last quarter. If we add in some additional borrowing last June after the debt ceiling deal was completed, the US is looking at almost $3 trillion in additional debt in the ten months from June 1, 2023 to March 31, 2024.

This line is going to have to start sloping up again soon.

DKI Takeaway: As people complain that the Federal Reserve has hiked rates “too quickly” and is “breaking things”, Congressional overspending is undoing the Fed’s work. While the Fed is trying to slow the economy to get inflation under control, Congress now has effective control over the money printer and is doing all they can to stimulate the economy and get cash in the hands of favored constituencies. Given that we’re entering an election year, this won’t stop. Higher for longer now means interest rates, overspending, and inflation.

-

Bank of Japan Throws in the Towel - Again:

For more than a year, DKI has been warning of the slow-moving fiscal disaster in Japan. The Japanese government has taken on massive debt and has kept the yield on their 10-year government bonds at below-market levels. This has caused the yen to plummet; a big problem in an island nation with few natural resources. This week, the Bank of Japan has decided to effectively raise long-term rates for the third time in the past year. They’ll now let the 10-year trade above a 1% yield.

You can see where the BoJ allowed higher yields in the past year. They’ll stop defending 1% now.

Imagine inflation here in the US if the dollar fell by more than 30% against other major currencies.

DKI Takeaway: Unfortunately, the BoJ is stuck. Keep rates artificially low, and the yen falls leading to inflation. Raise rates and that leads to budget deficits that have to be paid by printing more yen. That reduces the value of the yen leading to inflation. This is scary given that Japan is the world’s third largest economy. It’s even more scary given that the US Congress and the Treasury Department are viewing this is as a model to be emulated. For more detail on the topic, check out “Japan is in Trouble – US Treasury Department Trying to Catch up to Them”.

-

ISM Manufacturing PMI Comes in Below Expectations:

The October ISM Manufacturing PMI came in at 46.7 which was well-below the 49.0 expected. Below 50 indicates contraction. Part of the decline was related to strikes at the auto companies which appear headed for resolution (with higher car prices on the way). It also looks like part of the drop is related to a decrease in demand. That’s interesting given Congress’ stimulus spending.

Below 50 and in contraction for the past year.

DKI Takeaway: This one is a win for the Federal Reserve. They’ve been trying to slow economic activity. While inflation remains much higher than the 2% target, weaker manufacturing activity will help reduce price pressures assuming it’s related to lower demand. If it’s a reduction in production while the consumer continues to spend, we’ll again have more money chasing fewer goods which leads to higher prices.

-

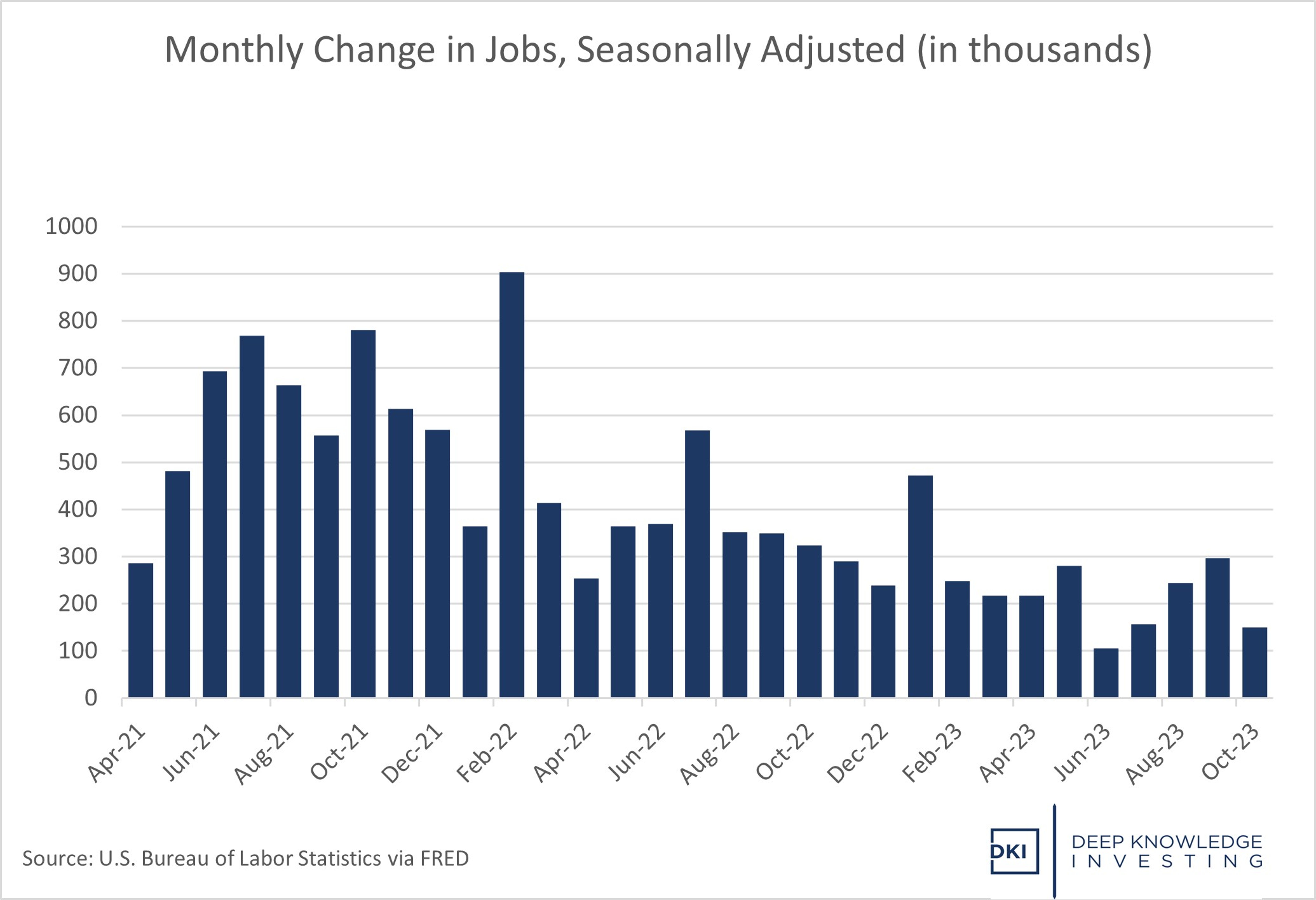

New Jobs Report is Just the Right Amount of “Bad”:

The new nonfarm payroll report shows employment was up by 150k in October. That’s below last month’s 297k and below expectations for 180k new jobs. Part of the decrease was due to strikes at several auto plants which are expected to come to an end soon. The unemployment rate was expected to remain flat at 3.8%, but ticked up to 3.9%.

October was below expectations, but still positive.

DKI Takeaway: For the past two years, we’ve seen a “good news is bad news” dynamic where positive economic news makes the stock market fall due to expectations of more Federal Reserve rate hikes. The relative weakness in this month’s employment report combined with Chairman Powell’s public pause on more rate hikes was encouraging for the market. One caution is that more people are starting to notice that government statistics are now prone to massive restatement in subsequent months. It will be interesting to see which direction today’s 150k jobs gets revised and by how much.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.