(Tuesday market close) The last time the S&P 500 index (SPX) exchanged greetings with 4,000, it was climbing the stairs. Today, it met 4,000 again, this time on the way back down. Major indexes collapsed to one-month lows Tuesday amid broad-based selling that hinged on rising Treasury yields and worries about consumer health.

The market was already skittish entering the week thanks to rising rates and growing concerns about inflation. Weak outlooks this morning from retail giants Home Depot HD and Walmart WMT appeared to seal the deal. The SPX closed below 4,000 for the first time since January 20, and volatility skyrocketed.

The selloff was broad, encompassing most sectors. Losing stocks far outnumbered winning ones. While it wasn’t a rush out the door, selling appeared steady most of the day and there was little evidence of people stepping in to buy. Volatility reached the highest point in more than a month, and Treasury yields rallied to their highest levels since early November.

It appears the market is doing a bit of repricing—building in expectations that rates could be higher for longer. Today’s rally in both 2-year and 10-year Treasury yields might have been a major factor keeping buyers away.

Another factor could be a shaky U.S. consumer outlook, highlighted by the small-cap Russell 2000 index’s (RUT) weak performance. The RUT is made up of companies with far more domestic than international exposure, so U.S. consumer weakness would likely be reflected there most heavily. Sure enough, the RUT fell more sharply than other indexes today.

The yield story and the consumer story aren’t necessarily detached. Weak outlooks from WMT and HD tie into the Federal Reserve’s willingness to hike rates, and when you see this kind of caution from WMT, it looks very likely that higher borrowing costs could hurt U.S. consumers.

Though consumer-connected sectors did the worst Tuesday, almost every S&P sector finished in the red. Consumer discretionary shares were among the worst performers, which shouldn’t be a surprise considering the HD and WMT outlooks. Financials, info tech, industrials and other sectors frequently associated with hopes for economic growth all slumped.

More defensive parts of the market like staples and healthcare fared better but didn’t rally. Energy appeared to get a boost from crude oil hanging in at near unchanged prices.

As an investor, there’s no need to panic. If you were looking to add to your portfolio, potentially consider that, but waiting to see how things shake out isn’t a bad idea, either. Minutes tomorrow afternoon from the latest Federal Reserve meeting, along with the government’s second estimate of U.S. Q4 Gross Domestic Product (GDP) Thursday are possible touchpoints later this week.

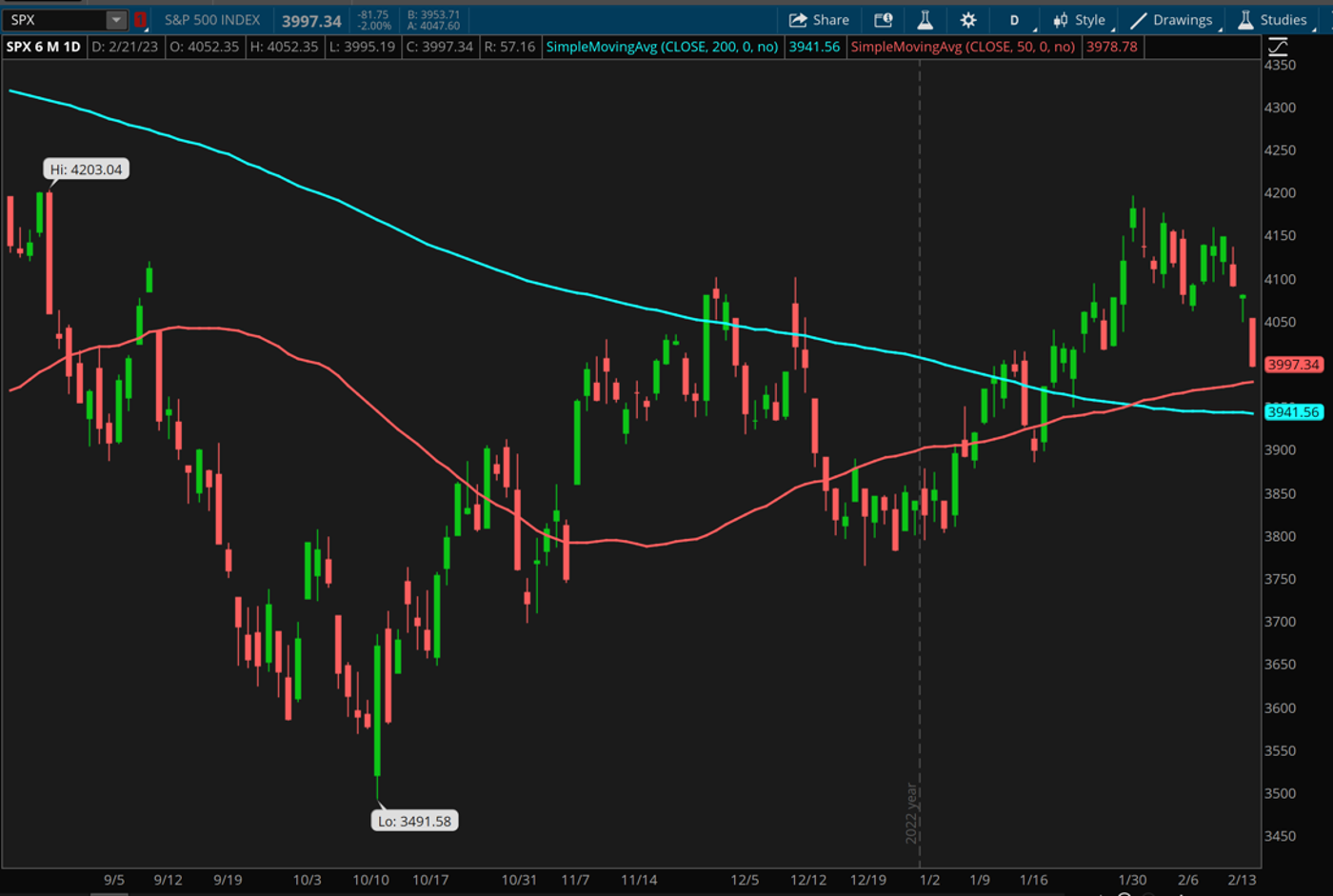

If you’re wondering about technical support, the SPX dropped below the key psychological 4,000 level and now could face a test of the 50-day moving average near 3,978. Below that is the 200-day moving average around 3,940. The SPX has been trading above the 200-day—usually a sign of positive technical conditions—since mid-January.

Market minutes

Here’s how the major indexes performed Tuesday:

- The Dow Jones Industrial Average ($DJI) dropped nearly 700 points, or 2.06%, to 33,129. That wiped out its gains for 2023.

- The Nasdaq Composite ($COMP) fell 2.5% to 11,492.

- The RUT dropped nearly 3% to 1,889.

- The SPX fell 81 points, or 2% to 3,997.

- The Cboe Volatility Index® (VIX) rose 7.7% to 22.87, the highest it’s closed since January 3.

CHART OF THE DAY: SUPPORT GROUP. The S&P 500 index (SPX—candlesticks) closed on the wrong side of 4,000 today for the first time in a month, with possible technical support now seen at the 50-day moving and 200-day moving averages (red and blue lines). Data source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Calendar

Feb. 22: MBA Weekly Applications Survey and expected earnings from TJX Companies (TJX), Nvidia (NVDA), and Baidu (BIDU)

Feb. 23: Q4 GDP second estimate and expected earnings from Alibaba (BABA) and PG&E (PCG)

Feb. 24: January PCE Prices, January Personal Income and Personal Spending, January New Home Sales, and final February University of Michigan Consumer Sentiment Index

Feb. 27: January Durable goods orders, January Pending Home Sales

Feb. 28: February Chicago PMI, February Consumer Confidence, and expected earnings from Target (TGT), Ross Stores (ROST), and HP (HPQ)

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.