How To Hedge A $500k Mutual Fund Portfolio

A reader recently emailed me, asking how he could hedge a "typical $500k mutual fund portfolio". I'm going to walk through a step-by-step example of doing that in this post.

Step One: Choose A Proxy Exchange-Traded Fund

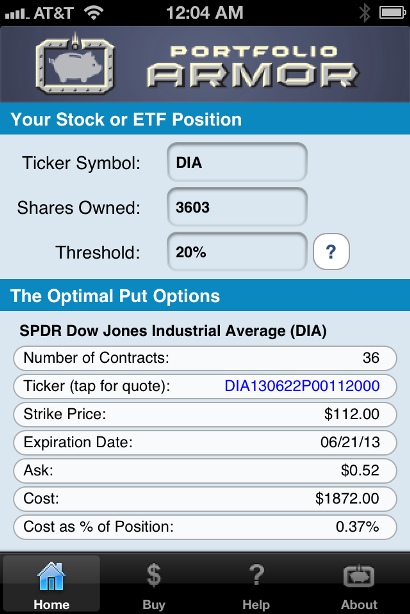

Although mutual funds can't be hedged directly, you can still hedge a portfolio of mutual funds against market risk by buying optimal puts* on a suitable exchange-traded fund, or ETF. The first consideration is that the ETF will need to have options traded on it, but most of the most widely-traded ETFs do. The second consideration is that the ETF be invested in same asset class as your portfolio. Let's assume your portfolio consists of mutual funds that are invested in blue chip U.S. stocks. An ETF you could use as a proxy would be the SPDR Dow Jones Industrial Average (DIA), which, as its name suggests, tracks the Dow Jones Industrial Average. You could then enter its ticker symbol, DIA, in "Ticker Symbol" field in the Portfolio Armor iOS app, as in the screen capture below.

Step 2: Pick A Number Of Shares

In order to hedge a $500k equity portfolio against market risk, you would want to hedge an equivalent dollar amount of your proxy ETF. Since DIA traded at $138.76 on Wednesday, you would simply divide your portfolio dollar amount, $500,000, by $139.76, and enter the quotient, 3603, in the "Shares Owned" field, as in the screen capture below.

Step 3: Pick a Threshold

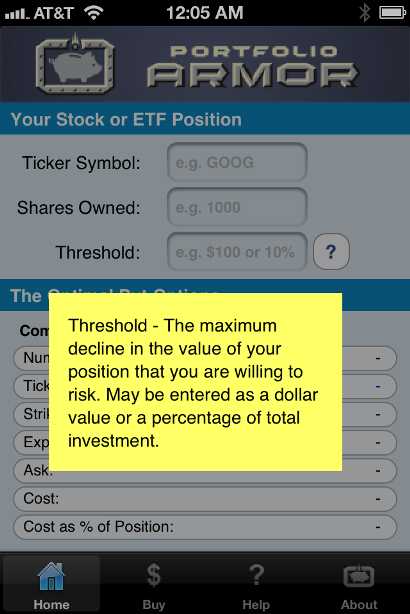

Threshold, in this context, means the maximum decline in the value of your position that you are willing to risk. If you weren't sure of that, you could click on the question mark to the right of the Threshold field above, and you'd see this explanation in the screen capture below.

What is the maximum decline you are willing to risk? Generally, the larger the decline, the less expensive the hedge, and vice-versa. In some cases, a threshold that's too small can be so expensive to hedge that the cost of doing so is greater than the loss you are trying to hedge. I generally use 20% decline thresholds when hedging equities, an idea borrowed from a comment made by fund manager John Hussman in 2008:

An intolerable loss, in my view, is one that requires a heroic recovery simply to break even … a short-term loss of 20%, particularly after the market has become severely depressed, should not be at all intolerable to long-term investors because such losses are generally reversed in the first few months of an advance (or even a powerful bear market rally).

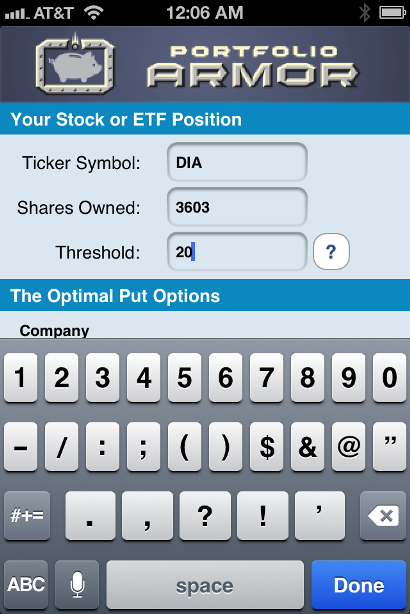

Essentially, 20% is a large enough threshold that it reduces the cost of hedging but not so large that it precludes a recovery. So we'll enter 20, in the Threshold field below, and tap "done", as in the screen capture below.

Step 4: Find the Optimal Puts

A few moments after tapping "Done", we'd be presented with the optimal puts. The screen capture below shows the optimal puts, as of Wednesday's close to hedge against a greater-than-20% drop in DIA.

As you can see at the bottom of the screen capture above, the cost of this protection was only 0.37% of the investor's position value.

How This Hedge Would Protect Your Mutual Fund Portfolio

Remember, the reason we picked DIA in this case is because our hypothetical investor's mutual funds were invested in blue chip US stocks. If these mutual funds drop in value due to a market decline, most likely, the Dow Jones Industrial Average will have dropped as well. And if the Dow has dropped, the ETF tracking it, DIA, will have dropped as well. If the Dow drops more than 20% -- if it drops 20.5%, 30%, 40%, or even more -- the put options above will rise in price by at least enough so that the total value of a $500k position in DIA + the puts will have only dropped by 20%, in a worst-case scenario.

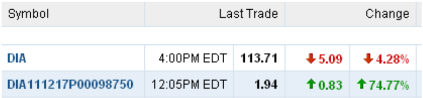

Put option prices can move in a nonlinear fashion, which enables a small dollar amount of them to hedge a much larger dollar value position in an underlying security. Here is an example of that nonlinearity in action: in June of 2011, I bought the optimal puts to hedge against a greater-than-20% decline in DIA over the next several months for my portfolio. Those optimal puts happened to be the $98.75 strike, December expiration puts (represented by the symbol DIA111217P00098750 in the screen capture below). On one day early that August, the Dow and DIA dropped 4.28%. On that day those optimal puts on DIA were up 74.77%.

Hedging Using A Smaller Threshold

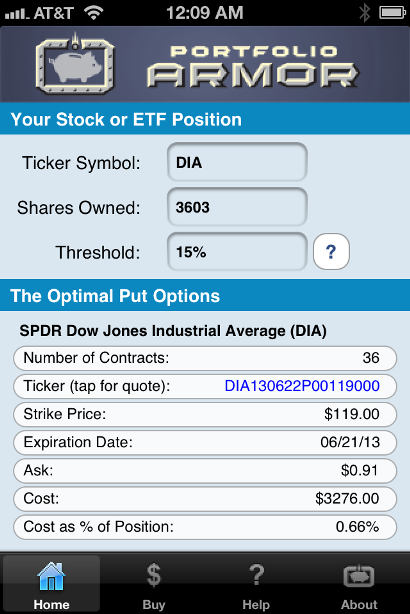

If you want to hedge using a different decline threshold, you can do so. All else equal, it will be less expensive to hedge against a larger decline, and more expensive to hedge against a smaller decline, but the cost of hedging against market risk is low enough right now that you might consider using a smaller threshold. Below is a screen capture of the optimal puts to hedge against a greater-than-15% decline in DIA, as of Wednesday's close.

Hedging A Portfolio Of Stock And Bond Mutual Funds

The example above is simplified in that we've assumed our hypothetical investor's portfolio is entirely invested in equity mutual funds. But what if he had some bond mutual funds? In that case, we could use a similar process to hedge his portfolio against market risk, except instead of using just one proxy ETF, we'd use one per each asset class. So, for example, if 60% of the investor's assets were in blue chip US stocks, and 40% in investment grade corporate bonds, we might scan for optimal puts for a $300k position in DIA and then scan for optimal puts for a $200k position in the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD).

*Optimal puts are the ones that will give you the level of protection you want at the lowest possible cost. Portfolio Armor uses an algorithm developed by a finance Ph.D to sort through and analyze all of the available puts for your stocks and ETFs, scanning for the optimal ones.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.