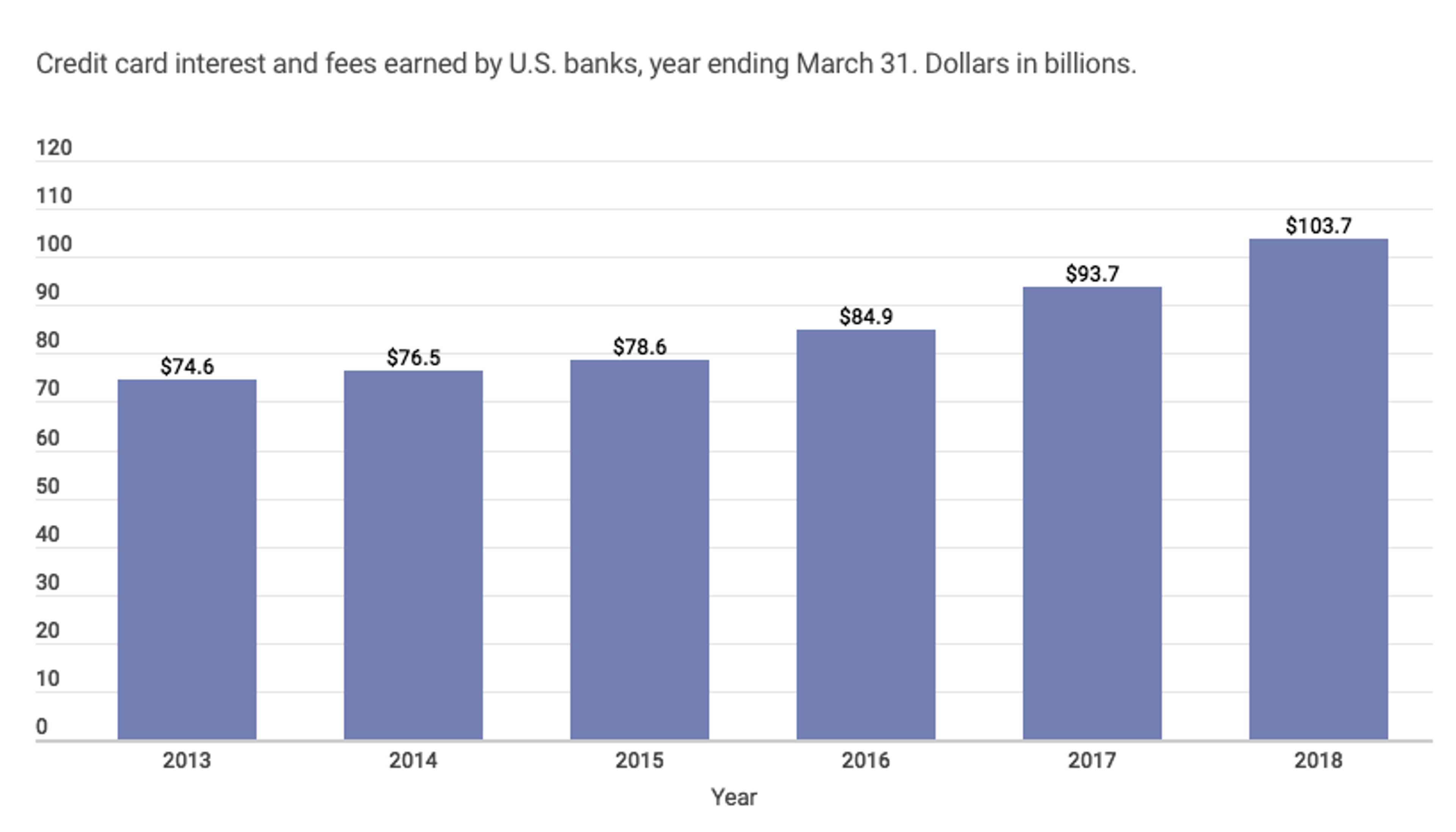

If you struggle with credit card debt, you’re not alone. In 2018, Americans paid banks over $104 billion in credit card interest and fees, a number that continues to grow. And 44% of credit card balances are not paid in full at the end of the month, and the average American with at least 1 credit card has debt to the tune of over $6,300.

Ready to tackle your debt with a plan of action? You can manage and avoid the never-ending cycle of minimum payments. Use our guide to learn how you can pay off your credit card debt.

Overview: What is Credit Card Debt?

Credit card debt is a type of unsecured liability accessed by an issued credit card. Creditors extend a line of credit to you, the borrower, based on your unique income situation and credit history. Then, you as the credit card holder can use the credit throughout the month.

When used responsibly, credit card debt isn’t necessarily a bad thing. It's one of the first ways for new high school or college graduates to begin building credit. It's common to sign up for a low-benefits credit card with a low line of interest and pay the balance off in full every month.

Credit cards also often offer rewards such as cash back or free airline miles. And they also generally carry much lower interest rates than personal loans, so if you want to make a large purchase but can’t afford to pay it off until your next pay period, a credit card can allow you to get what you need without accumulating interest — as long as you are able to make the payment-in-full before the next period.

Unfortunately, many Americans get into trouble with credit bureaus because they spend more than they can afford using a credit card. Credit card debt highly influences your credit score because it is the most common type of credit usage requested and utilized.

This means that even a few missed payments can severely lower your score, making it more difficult to secure home, auto and personal loans in the future.

If you currently have outstanding credit card debts, paying them down should be your 1st financial goal. Eliminating your credit card debt will help improve your credit score (which makes it easier to secure a low-interest loan for other goals) and also help you save money by avoiding excessive interest charges.

How to Pay Down Your Credit Card Debt

Follow these 5 steps.

Step 1: Figure Out Exactly What You Owe

You can’t begin to pay down your debts if you aren’t sure where you owe money. While this may sound like a simple task, most consumers have more than 1 credit card, and it’s easy to lose track of what you owe on each account and the interest rates associated with each debt.

Understand, organize and outline all of your debts to help you decide where you should begin paying 1st and how you can avoid accumulating excess interest charges. Sit down with all of your cards, open all of your account statements and create a comprehensive “master list” of all of your outstanding debts.

Related content: Best Ways to Consolidate Credit Card Debt

Step 2: Target One Debt at a Time

The best way to pay off credit card debt is by using what’s called the “snowball method” of debt reduction. The snowball method dictates that you pay down your smallest debt 1st while also making minimum payments on your larger debts to avoid accruing interest. Identify your smallest debt, write out how much you owe and how much the minimum payments are on all of your other accounts.

Put all of your available extra funds toward paying down your smallest debt while also making the minimum payments on your other accounts. After you have paid off your smallest debt, keep the “snowball” rolling by directing all of your funds towards the 2nd smallest debt, then the 3rd and so on.

Set up direct withdrawals for your credit card accounts that allow automatic payments. Automatic payments will deduct minimum payments from your checking or savings account without requiring you to remember to schedule payments on or before the day they’re due.

This will help you avoid excessive interest charges and additional delinquency on your credit report. If you’re interested in learning more about how to set up direct deposit, check out our guide to learn more about the basics of linking bank and credit card accounts. Contact your credit provider to authorize direct debits for your minimum balances.

Step 3: Rethink Your Budget

It’s easy to say that the solution to paying down credit card debt is to pay more than the minimum amount required, but where can you find money to put your plan into action?

Rethinking your budget and assigning a job to every dollar in your account can help you keep track of where your money goes and locate places where you can cut back and save. Many consumers like to use a budgeting app like Mint to help automatically categorize spending.

While Mint is a popular budgeting app, there are also a number of alternatives to Mint designed specifically for millennials, couples, older savers, college students and any other niche segment of the population.

Choose your favorite budgeting app, sign up for an account, and learn where you can save to put more money toward your debt.

Step 4: Consider Debt Consolidation or Professional Assistance

Credit card debt consolidation is a process that can be useful if you have multiple high balances. Consolidation is a loan process that takes all of your debts from various sources and “rolls” them all into a single monthly payment.

Before you consider a consolidation loan, reexamine your spending and try to reach out to your individual creditors. They may be willing to lower your payments or forgive a percentage of your interest charges if you are able to make a lump sum payment instead.

If you do decide that a debt consolidation loan is right for you, know that the low introductory rate used to lure consumers is typically a “teaser rate” which may increase after a certain period of time. Have a plan in place to ensure that you do not overspend and incur additional debts on your accounts after your debt has been consolidated. To learn more about the pros and cons of debt consolidation loans, check out the video below:

If you are in way over your head, all hope is not lost – financial planning professionals may be able to communicate with your creditors on your behalf to negotiate a lower payment or interest rate. If your debt has been turned over to a 3rd party collection agency or you have been sued for your debt, it’s time to bring in the help of a finance and credit professional in your community.

If a loan isn’t something you want, you can try a platform like Accredited Debt Relief. Use this platform to get a customized plan and a savings account that you will pay into to help pay off your debts. On the backend, Accredited Debt Relief negotiates debts on your behalf and helps you get out of debt as fast as possible.

- No Credit History

Step 5: Budget With the Extra Card

Now that you have a plan to address your credit card debt, you might feel something is missing from your financial transactions. Credit cards often provide you with rewards, but you don’t want to accrue massive credit card debts once again simply to cash in a few rewards.

When you switch to the Extra Debit Card, you connect your bank account, use your new card and accrue rewards like normal. No, this is not a credit card—it’s a unique and consumer-friendly debit card. Extra Card pays for transactions and then settles them using your bank account.

This card is especially helpful in that it:

- Allows you to track your spending

- Offers robust rewards

- Reports to the credit bureau once a month and helps rebuild your credit

Extra Card charges a reasonable annual membership fee, doesn’t require a credit check and never asks for an initial deposit. Instead of repaying your credit card debt and waiting for a better score, earn a few rewards at the same time.

Ditch Your Debt

Paying down credit card debt can be a long, arduous and stressful process. It requires discipline, cutting back and sacrifice. However, paying down your debt (and increasing your credit score in the process) will do more than just give you peace of mind and a break from incessant phone calls about your debt.

A higher credit score can help open more opportunities for yourself and your family – from finally securing the mortgage you need to continuing your education with a student loan and more. Take the steps necessary to ditch your debt and build a firm foundation for your credit.

To learn more about how you can strengthen your finances, check out our guides on the best savings accounts, how to consolidate debt and if you should pay off your mortgage or invest.

About Sarah Horvath

Sarah is an expert in the insurance, investing for retirement and cryptocurrency space.