A credit report contains a wealth of information on your current outstanding debt, as well as on your employment, bill payment, and loan history. The report also shows your personal information, including places of residence. Credit reports also indicate if you have filed for bankruptcy and might show if you have been arrested or sued.

Your credit report and score contribute to the information lenders use to decide if you can obtain loans and debt-related products such as credit cards. Landlords also use them to screen tenants, and some employers consult them when they make hiring decisions.

You’ll be in better financial shape once you know how to interpret and correct the information that appears on your credit report. Once you know how lenders use credit scores, you’ll be way ahead of the game. The Fair Credit Reporting Act gives you an opportunity to see your score and become a more active player in your own finances as you seek out debt consolidation, a line of credit, tackle credit card debt and more.

Why It’s Important to Understand What’s Behind the Number

Good credit is an important aspect of your financial well-being. A periodic review of your credit report allows you to examine your credit score and find possible errors.

Regularly reviewing your credit file could alert you to potential identity theft. Every 12 months, you can order a free credit report which contains your free credit score from the three major credit agencies: Experian, TransUnion, and Equifax.

Lenders generally look at your Fair Isaac Corporation (FICO) score. Founded in 1956, FICO was the first company to offer a credit-risk model with a numerical score. This model continues to be used by the major credit companies to determine your creditworthiness.

The FICO score ranges from 300 to 850, although lenders use several different scores for different financial products. Lenders often use different credit scoring formulas, as well as information from different credit reporting sources.

For example, your home loan score might differ from your credit card score, while your online purchases could produce a different score from the previous two. Because lenders look at different reports, you may qualify for lower interest rates depending on what scores the lender considers, so it would be wise to shop around when looking for a loan.

Furthermore, you want to only apply for credit that you need, since your recent credit activity indicates to a lender what your credit needs might be. If you apply for a lot of credit within a short time span, a lender might interpret that to reflect a deteriorating economic situation, which may also adversely affect your credit score.

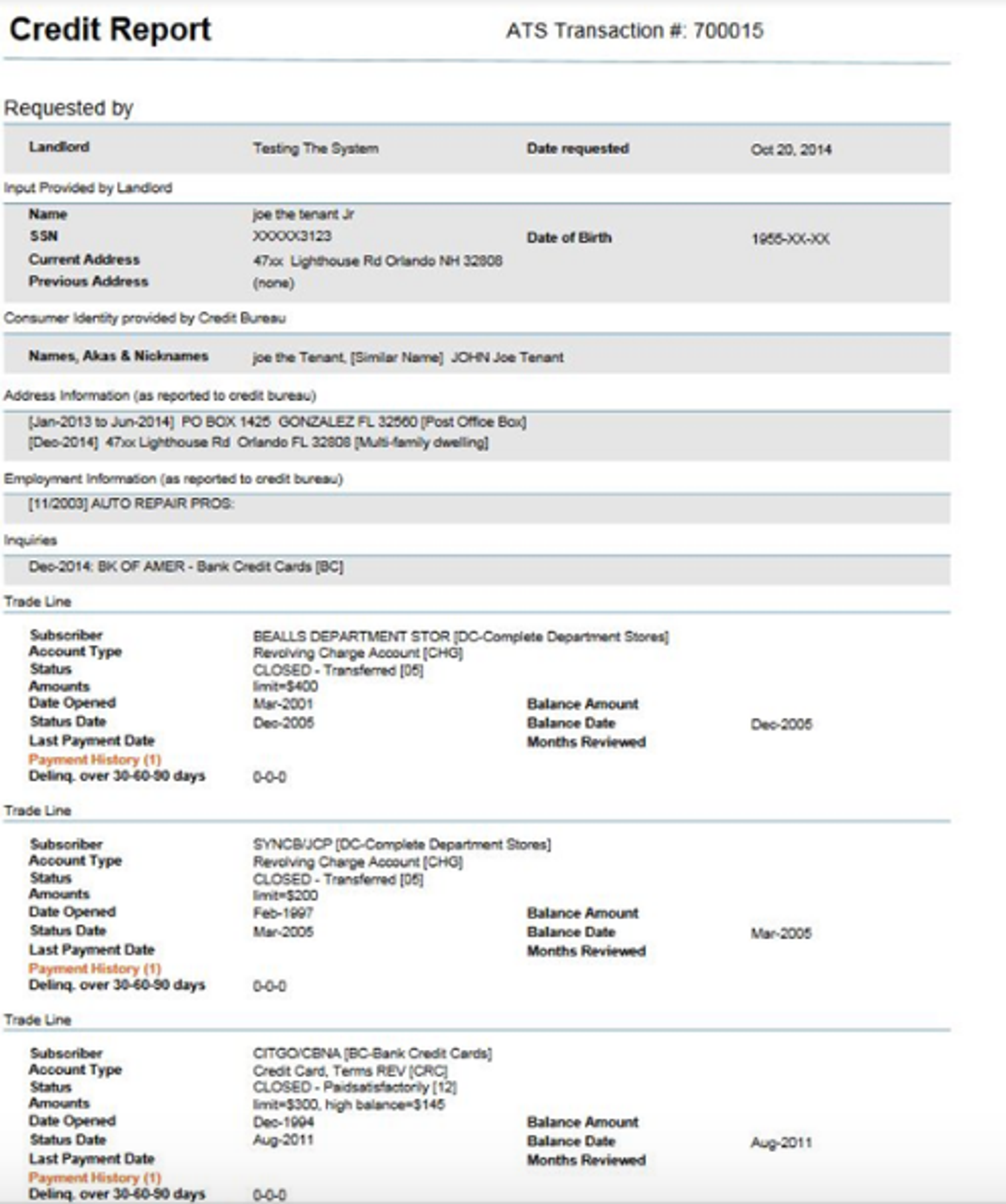

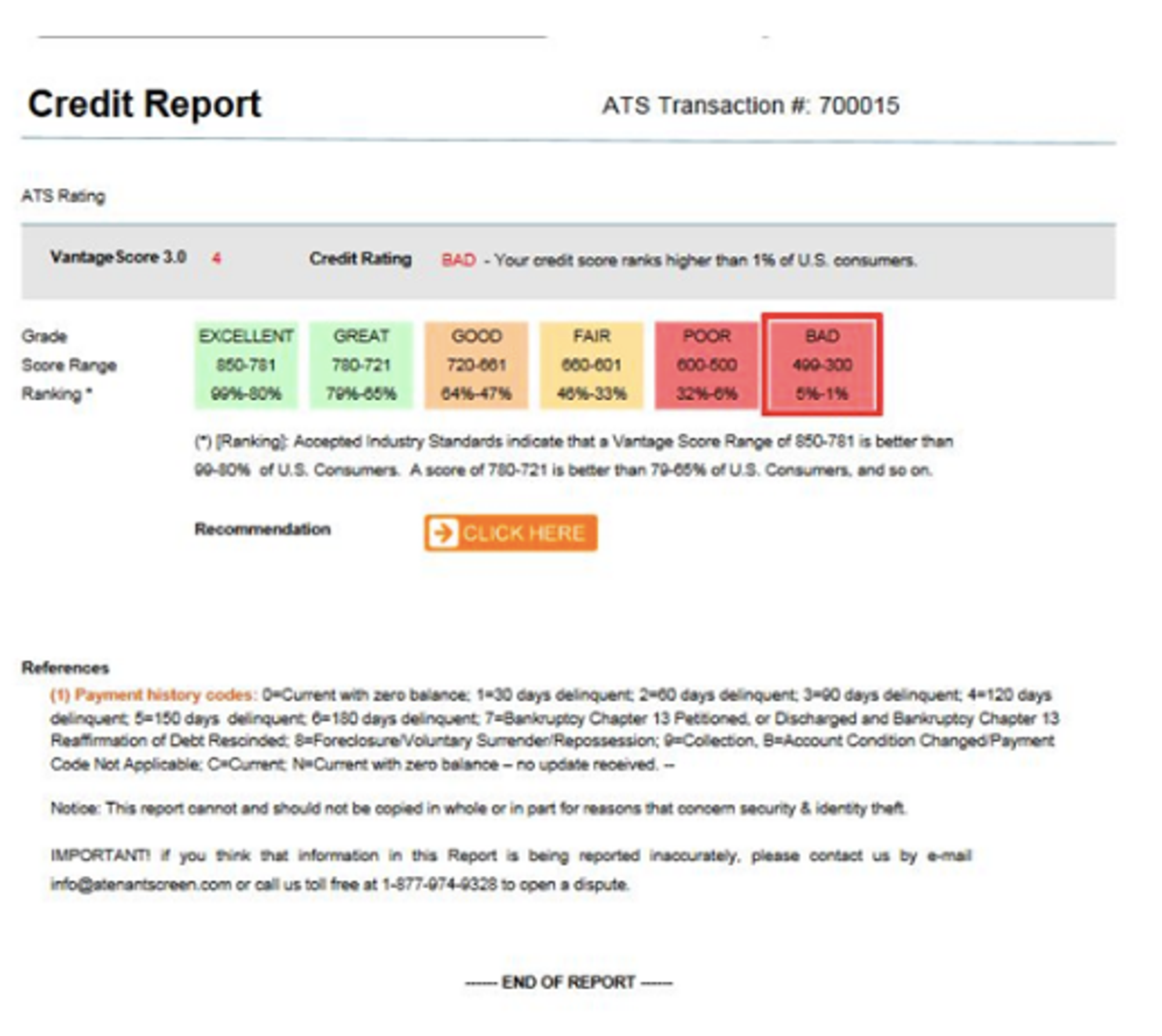

An example of a credit report requested by a tenant screening service from Experian can be seen below:

This particular report shows two revolving charge accounts and one credit card account, each with low limits, and that the individual only borrowed small amounts.

The result of the report is a credit score of 300 – 499, which indicates bad credit despite no delinquencies. Most lenders and landlords would avoid a person like this since he does not have much of a credit history.

What Affects Your Credit Score?

When the credit bureau reviews your report, they are judging your credit risk based on the information that they find. Remember, a credit rating agency is just using math to grade you. There is no emotion behind your credit history, that student loan you’re behind on, if identity theft occurred, etc. Your credit rating changes based on this pre-determined formula, and that is why many mortgage loan providers use formulas to help raise your credit using their own data.

In short, the bureau learns your:

- History of loan or credit accounts

- Accounts that are in arrears

- Accounts that are charged off

- Accounts on which you co-signed

- Payment history

- Accounts that are 7 years old or less (if you find older accounts, ask to have them removed)

- The duration of your debts

- Any liens filed against you

Using credit monitoring services can help you see your consumer credit information, check for errors, etc. This is why your free annual credit report is a good investment of time. Plus, you can check routinely to see what your activities are doing to alter your score.

What You Need to Understand on Your Credit Report

Your credit report consists of a number of components, and your free credit check helps you see:

Component 1: Your Personal Information

Personal items that appear on your credit report usually include your:

- Legal name(s) and aliases

- Address(es)

- Phone number(s)

- Birthdate

- Social Security number: Credit agencies often obscure this number in reports unrelated to employment or taxation where you would have disclosed it.

Component 2: Your Employment History

Information about your employer history may be included in your credit report. If you find inaccuracies, you can file a dispute to change the information on the report.

Employment data that appears on a credit report can often be used to verify your identity.

Component 3: Credit Inquiries

This section highlights the legitimate businesses, such as banks, credit agencies or landlords, that have made inquiries into your credit status.

When you apply for credit by making a bank loan or credit card application, for example, the potential lender conducts what is known as a hard inquiry. Credit checks not made by prospective lenders are called soft inquiries.

Component 4: Credit-Related Accounts

Your outstanding credit accounts or trade lines usually make up the bulk of your credit report. In general, the more accounts you have in good standing, the higher your credit score will be. As long as your accounts remain in good standing and all payments were made in a timely manner, your credit score should be higher.

Credit scores are based on your behavior over time, so the longer you display good credit behavior with a lender, the more your score will improve. If you have multiple accounts, it’s important to make timely payments on all of them. Outstanding balances should also remain small in relation to your accounts’ credit limits.

Furthermore, closing and opening different accounts may affect your overall credit score. For example, if you consolidate all of your credit card accounts into one account, this could adversely impact your credit score, especially if you end up using a large percentage of your total credit card limit. Also, the frequent opening and closing of accounts, as well as the transfer of significant account balances, can damage your credit score.

When reviewing your information, you can both enhance your financial literacy, understand your credit rating better and catch fraud as early as possible.

How to Improve Your Credit Scores

Improving your credit score is just as important as reading the report. Yes, you need to handle inaccuracies (an issue covered below), but the credit rating agency is generally looking for:

- Good payment history (pay on time)

- Keeping accounts open and in good standing

- Little to no charge-offs (work out a deal with creditors instead of letting the account go stale)

- The ability to grow your credit—larger and larger accounts in good standing

Of course, this list is not exhaustive, but these are things that are under your control. Keep in mind that:

- Any deposit account you hold must be in the positive

- You want to avoid repossession or foreclosure at all costs

- Opening new credit cards or accounts could adversely impact your score initially

- Opening several new accounts at once could also impact your score

- Large loans often put a damper on your credit until you show that you have a good payment history

- Lenders will review your entire account and judge your risk based on everything they see

What does this mean? If you’re trying to get pre-approved for a mortgage and you have just bought a car, the lender may believe you are not in a good position to be approved. In short, you want to be careful about how and when you open credit or loan accounts.

What To Do About Inaccuracies

Mistakes and inaccuracies in your credit report can adversely affect your credit history and current credit score. Your personal information (name, address or phone number) could contain mistakes.

Accounts, loans or credit cards might not belong to you or could have been created through identity theft. Erroneous reports of delinquent or late payments could also appear.

Closed accounts could also be listed incorrectly as open, or an unpaid debt could be listed more than once. Once you have found an inaccuracy, you can contact both the creditor that provided the information and the credit reporting company to have your credit record corrected.

If you decide to do this, explain to them what you think is wrong and your reasons. Make sure to include copies of any documentation that supports your side of the issue. Most credit reports come with a section on how to dispute mistakes.

Why Are There Different Credit Scores?

There are 3 major credit bureaus:

- TransUnion

- Equifax

- Experian

Because each company has its own algorithm and formula to create your credit score, they will also be a bit different. This also means that improving your credit score on each platform could occur slightly differently.

Final Thoughts

You might need a high credit score to facilitate future loans and obtain more credit. Raising your credit score involves paying your bills on time, every time, which can be done by setting up automatic payments with your bank.

If you have any missed payments, make sure you pay them as soon as possible and continue to keep up. Most negative items stay on your credit report for seven years, although bankruptcies remain on your report for 10 years.

Credit scoring models also tend to look at how close you are to your credit limit, and a red flag goes up if you exceed or get too close to your credit limit. An almost-maxed out account can also hurt your credit rating, so make an effort to keep your debt balances low in proportion to your overall credit limit.

With respect to your FICO number, lenders in the United States tend to turn down people with a credit score below 599. Those with poor and bad credit (300-599) are unlikely to get approved for a significant loan.

Frequently Asked Questions

What’s a good credit score range?

A good credit score range typically falls between 670 and 850. However, it’s important to note that different lenders may have their own criteria for what they consider to be a good credit score. Generally, a higher credit score within this range indicates a lower risk to lenders and can result in better loan terms and interest rates.

What shows up on a credit report?

A credit report typically includes your personal identifying information, such as your name, address, and social security number. It also includes details about your credit history, such as your open and closed accounts, payment history, credit limits, and balances. Additionally, it may include information about any public records, such as bankruptcies or tax liens, as well as credit inquiries made by lenders when you apply for credit.

Do bank accounts appear on credit reports?

What does R mean on a credit report?

What are the types of collections on credit report?

The types of collections that can appear on a credit report include medical collections, utility collections, credit card collections, student loan collections, and personal loan collections. These collections typically occur when an individual fails to make payments on their debts and the creditor or lender sells the debt to a collection agency. It is important to address and resolve these collections as they can have a negative impact on an individual’s credit score and ability to obtain credit in the future.

About Jay and Julie Hawk

About Julie:

Julie Hawk earned her honors undergraduate degree from the University of Michigan before pursuing post-graduate scientific research at Cambridge University. She then started work in the private sector as a business systems analyst for a major investment bank, where she qualified as a Series 7 Registered Representative and received comprehensive training in various financial products. Further honing her skills, she attended the prestigious O’Connell and Piper options training course in Chicago, mastering professional option risk management techniques.

Julie then transitioned into the role of a professional Interbank forex trader, currency derivative risk manager and technical analyst, ascending to the position of vice president over a 12-year career in the financial markets. Julie’s illustrious banking career spanned working for major international banks in New York City, London, and San Francisco, where she served as an Interbank dealer, technical analyst, derivative specialist and risk manager. Her responsibilities included educating, devising customized foreign exchange hedging and risk-taking strategies, and overseeing large-scale transactions for esteemed banking clients, including corporations, fund managers and high-net-worth individuals. As part of her responsibilities, Julie managed substantial portfolios of forex options, spot, and futures positions as a currency options risk manager, earning recognition for executing innovative and highly profitable forex derivative transactions. Julie also spearheaded educational conferences on currency derivatives.

During her banking career, Julie attained world-class expertise in technical analysis, including Elliott Wave Theory, and pioneered research into automated trading and trading signal systems. An active member of the San Francisco Writers’ Guild, Julie also authored trade strategies, educational material, market commentary, newsletters, reports, articles, and press releases. She became a sought-after market expert who was frequently interviewed by financial magazines and news wires such as REUTERS.

Following her retirement from the banking sector, she dedicated 15 years to online forex trading, mentoring and freelance writing for TheFXperts, which she co-founded with her husband Jay. Julie is the co-author of “Forex Trading: A Beginner’s Guide” and “Technical Analysis for Financial Markets Traders,” in addition to five other books on financial markets trading and personal finance. She now focuses on writing articles on financial markets for platforms like Benzinga, although she continues to trade forex online and mentor fellow traders as part of TheFXperts’ financial team.

About Jay:

Jay Hawk grew up in Chicago and Mexico City where he became bilingual in English and Spanish. After taking formal training as a classical guitarist at prestigious music conservatories in Europe, Jay then embarked on a remarkable journey into the financial markets, cultivating his notable expertise through hands-on experience that began on the Midwest Stock Exchange.

His financial career progressed as he started actively participating in various exchange floor trading activities in the Chicago futures and options pits, where he worked his way up the ladder, serving as a clerk, trader, broker, investor and fund manager. Jay then ran a retail stock brokerage desk and managed funds for large institutional investors, leveraging his discretionary trading skills to yield profitable results for clients.

This ultimately led to Jay holding exchange seats and operating as a market maker on options exchanges in Chicago and San Francisco, initially on the Chicago Board Options Exchange. Jay also played a significant role in the Chicago Mercantile Exchange’s evolution, where he contributed to launching and actively trading the first listed currency futures options. After transitioning to the West Coast, Jay then held a seat and ventured into trading stock options and their underlying stocks on the Pacific Options Exchange.

Jay’s comprehensive understanding of fundamental economic and corporate analysis continues to inform his trading and investment activities and has led to his subsequent success as an expert financial writer. Together with his wife Julie, he co-authored “Stock Trading: A Beginner’s Guide”, “Commodity Trading: A Beginner’s Guide” and “Fundamental Analysis for Financial Markets Traders,” among their published books focusing on financial markets trading, market analysis, and personal finance.

As an integral member of TheFXperts’ team, Jay now excels in trading forex online for his personal account, mentoring aspiring traders and writing for financial platforms like Benzinga where he specializes in covering topics related to the stock and commodity markets, as well as investing, trading and reviewing online brokers.