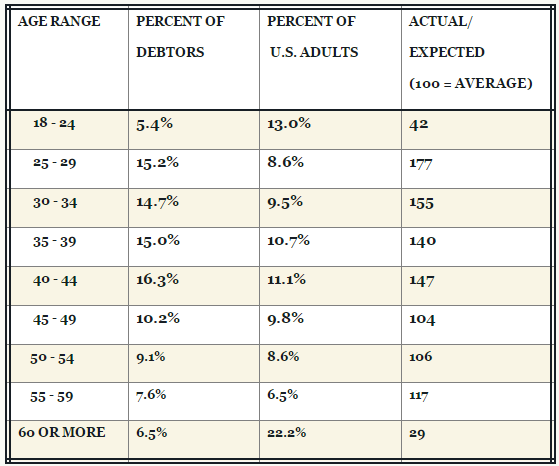

According to the United States Department of Justice, "[T]he ages of 25–44 are the peak years for filing bankruptcy. People between the ages of 45 and 59 file at about the rate that would be expected by their proportion in the population at large." In other words, those who file bankruptcy are more likely to belong to the Millennial or Gen X generation demographics, with the highest percent of debtors belonging to the 40–44 age bracket.

agerange.png (25.04 KB)Source: U.S. Department of JusticeIn speaking with Professor Emeritus and Former Business Dean at New York University at Buffalo, author of "What to do When I get Stupid" and Financial Economist Lewis Mandell, PhD, Benzinga asked if it's possible to rebuild credit after bankruptcy. Mandell shared, "Yes. In fact, since a person cannot generally declare personal bankruptcy again for seven years, those who have just gone through personal bankruptcy are generally regarded as better credit risks than others, with similar finances, who have not declared bankruptcy within seven years."

The Key To Financial Freedom Post-Bankruptcy Is Maintenance

Mandell commented, "You can maintain a good credit rating by limited your use of actual and contingent credit. Actual credit consists of money borrowed and this should be as small a portion of your income as possible. Contingent credit consists of unused lines of credit and credit cards and other such things.

"Since a person with a lot of contingent credit can quickly increase the ratio of outstanding debt to income, that person is deemed to be more risky borrowers and by credit rating agencies," Mandell explained.

It's A Slow Process

"Rebuilding credit after bankruptcy is a slow process," Marco Pantoja, Interim-Director of the Office for Financial Success at the University of Missouri, told Benzinga.

"It may take several years to see a credit score well above the sub-prime area. With time, the negatives on the report dwindle in significance, and any positive history being developed is adding more credibility to the borrower," Pantoja clarified.

Take Time To Self-Reflect

Rebuilding credit post-bankruptcy is not a mindless exercise; it involves constant dedication and financial awareness. While the basic financial principals should always apply (save what you can; don't spend more than you make; treat credit as a method of paying for what you can already afford, not a means to pay for what you want and can't afford; etc.), properly rebuilding credit requires some serious self-reflection.

- 1. Understand Why You Ended Up In Bankruptcy. Pantoja elaborated, "To start, a person needs to be aware of what types of personal behavior or habits helped contribute to the need for bankruptcy. This awareness will help promote the development of positive financial habits and reduce the likeliness of relapsing."

- 2. Go Back To The Basics. "Some fundamental practices of personal finance would be the ideal habits to develop first; tracking expenses, budgeting and saving. With these relatively simple techniques, a person can maintain awareness of their financial situation, harness more control over their spending and reduce their reliance on debt," Pantoja said.

- 3. Start Savvy Spending Habits. Once the basics have been conquered, Pantoja recommended going beyond the beginner habits and embracing techniques that will bring your financial practices from passing to top-notch performing. "Combine these [techniques] with auto-bill pay tools, while avoiding over-spending on credit cards, and you have a surefire recipe for maintaining great credit."

Above all, it is essential to remember how many resources are available to those in financial distress. There is no need to go through the mental hardships of debt alone. If you are facing financial difficulties and are considering bankruptcy, reach out to those around you. Acknowledge the situation and act today. Financial recovery is possible and there is help available.

Image Credit: Public Domain© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

{kind=link}