Eye Of The Storm

From our front row at Lehman Brothers, we assure you iTesting the Fiscal Limitt was not the case that no one saw the Global Financial Crisis coming. With that in mind, the Treasury market’s struggle to absorb supply in the belly of the curve (2s, 5s and 7s), was a warning sign that the US is approaching its fiscal limit. As we’ve noted, the final $1.9 trillion pandemic fiscal stimulus and the August Treasury borrowing plan announcement triggered the only two periods we can recall, in our 39 years in the business, that Treasury rates moved sharply higher as a consequence of increased supply. Bloomberg headlines about long maturity USTs at their highest yields since 2007 came fast and furious on Thursday, and they were accompanied by a couple of notable investors forecasting 5+% yields. Term premium turned positive for the benchmark 10-year, at 10bp it is up 43bp in a week, 63bp in a month and 104bp in 3 months. Still, even with the impulsive adjustment, 10bp is a paltry premium for the interest rate risk of a security that lost the three largest buyers (the Fed, banks and foreigners), or even for the credit risk of a government with an unsustainable fiscal outlook.

As ominous as conditions appeared on Thursday, a negative GDP revision to services consumption and a cool core personal consumption deflator the following morning, broke the market risk-off fever, at least for now. The response to the data underscores the role of the Fed’s unexpectedly hawkish summary of economic projections in the Treasury and equity market tumult. The post-FOMC speeches left little doubt that the necessary condition for ending the rate hike cycle in the near term is slower growth, rather than disinflation. Of course, another round of bank stress, a nontrivial risk, would end the hiking cycle as well. Next week is scheduled to bring a round of data that could convince the Fed to end the hikes, but unfortunately a casualty of the looming government shutdown is next week’s August Job Openings and Labor Turnover Survey and the most important monthly report, the September Employment report.

While most public policy consultants expect a relatively short shutdown, the data void is likely to increase market expectations for a November hike even as market participants focus on a wide range of non-government data that points to a significant deceleration in consumer spending. We haven’t spent too much time on the implications of a government shutdown, largely because the two most notable ‘full’ shutdowns in late ‘95/early ‘96 and October ‘13 were associated with brief 4% S&P 500 pullbacks and no discernible economic impact. The political implications are both counterintuitive and significant. In both of the shutdown cases, as well as when the Democratic Congress, with an assist from Fed Chair Greenspan, forced George Bush to break his ‘read my lips, no new taxes’ pledge in ‘91, the party that was on the side of fiscal austerity was victorious in the next election. No doubt the GOP will take a transitory hit in public polling (see the Bloomberg headline below), but the public is firmly on the side of politicians supporting reduced debt and deficits. To be sure, markets are signaling the US is approaching its fiscal limit, however, the only acknowledgement from the Fed is Chair Powell suggesting in his press conference that increased supply may have played a role in higher longer maturity rates. Congress is fighting over the 30% of outlays that are discretionary, a battle that will barely move the needle on the long-term debt outlook. In other words, as we discuss at length in this week’s note, the markets are signaling a coming crisis that policymakers are some distance from recognizing, let alone addressing.

(BN) Republicans Will Lose Spin War Over Shutdown: Jonathan Bernstein

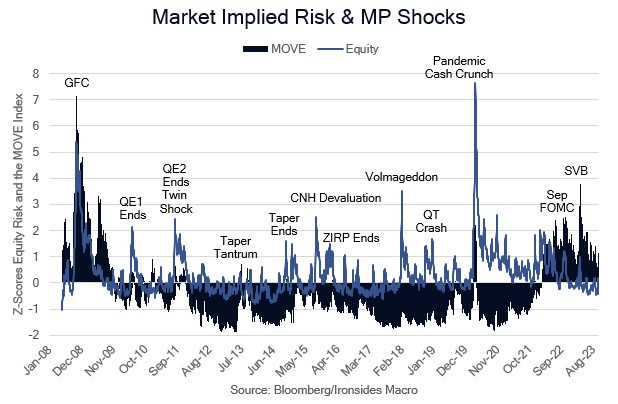

Meanwhile, our discussions this week focused on whether favorable seasonality and an end to the earnings recession will be sufficient to overcome the bear steepening in Treasuries, a deteriorating growth outlook, and excessively tight monetary policy forward guidance. The S&P 500 got close to our near term 4200 target and bounced, and underscoring the impact of bear steepening of the Treasury curve was the fact that the worst performing sector over the last 5 sessions was the most rate sensitive in the S&P 500, namely utilities. Although investor surveys showed negative sentiment, our “it’s what they pay, not what they say” approach to positioning is far from levels that imply investors are leaning short/defensive. The volatility (VIX), volatility of volatility (VVIX) indices, the term structure of VIX futures, and implied correlation are all close to their longer-term median levels. The skew index and correlation of upside calls relative to downside puts (melt-up/down risk) are at levels indicating shorts are building, consequently, it does not appear market positioning is vulnerable to more than brief short covering rallies. In Treasuries, the MOVE Index has bounced off the 100 level we expect to be the lower limit of its range, agency MBS has widened further, credit spreads are beginning to widen a bit, but remain exceptionally tight relative to mortgages and Treasuries. The yen is grinding towards the 150 level, the Ministry of Finance had another round of verbal intervention this week. Our contacts believe the relentless rally in crude oil may stall, but fundamental trends remain favorable. On balance, we suspect we are in the eye of the storm. The most obvious catalyst for a reversal of trend in equities and Treasuries is weaker labor market data that ends the rate hike cycle and weakens the FOMC’s resolve to keep the yield curve inverted through 1H24. Unfortunately, Congress is on a path to deny us of next week’s crucial data.

Figure 1: This is an aggregate of several measures of equity volatility, there are no signs of defensive positioning.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.